Fill Out a Valid Cri 200 Nj Template

In the governance of charitable activities within New Jersey, the Short-Form Registration/Verification Statement Form CRI-200 emerges as a pivotal document, underscoring the intricate relationship between regulatory protocols and philanthropic endeavors. Crafted by the New Jersey Office of the Attorney General, Division of Consumer Affairs, this form serves as a gateway for charitable organizations to navigate the state's regulatory landscape, ensuring that their operations align with established legal and ethical standards. Charitable entities, particularly those amassing gross contributions of $25,000 or less annually, find themselves compelled to engage with this form, either as part of their initial registration or during their renewal phase. This obligation extends even to organizations whose contributions do not exceed $10,000 annually, provided they refrain from hiring external solicitation services. The modest registration fee, set at $30, underscores the state's commitment to maintain an accessible regulatory environment. Moreover, the CRI-200 Form delineates the circumstances under which charities might be exempt from registration, sheds light on organizational structural changes, and mandates the disclosure of crucial financial and operational details. This nuanced blend of financial reporting, operational transparency, and regulatory compliance encapsulates the essence of the form, reflecting the broader objectives of the New Jersey Division of Consumer Affairs to foster a trustworthy charitable sector.

Sample - Cri 200 Nj Form

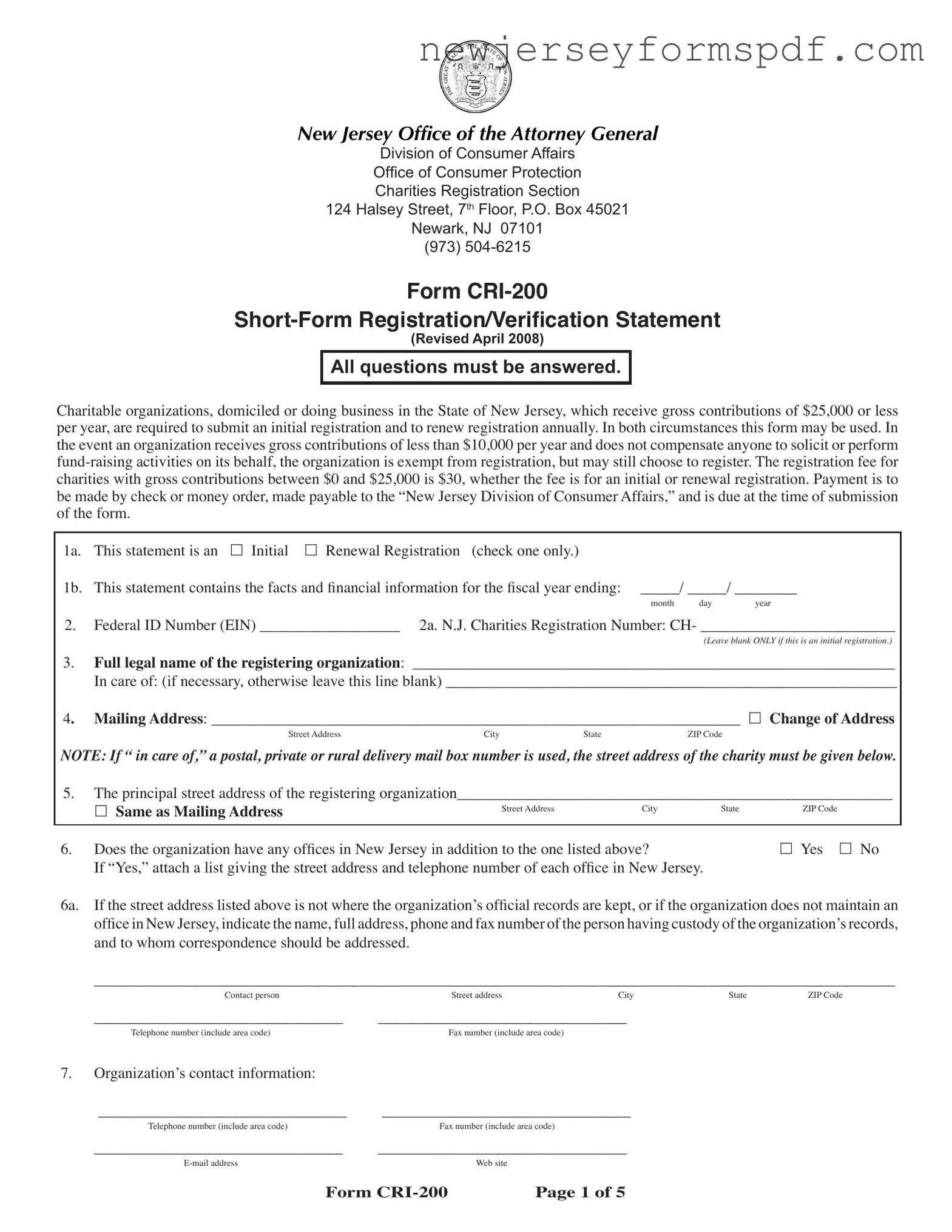

New Jersey Office of the Attorney General

Division of Consumer Affairs

Ofice of Consumer Protection

Charities Registration Section

124 Halsey Street, 7th Floor, P.O. Box 45021

Newark, NJ 07101

(973)

Form

(Revised April 2008)

All questions must be answered.

Charitable organizations, domiciled or doing business in the State of New Jersey, which receive gross contributions of $25,000 or less per year, are required to submit an initial registration and to renew registration annually. In both circumstances this form may be used. In the event an organization receives gross contributions of less than $10,000 per year and does not compensate anyone to solicit or perform

1a. |

This statement is an £ Initial £ Renewal Registration (check one only.) |

|

|

1b. |

This statement contains the facts and inancial information for the iscal year ending: _____/ _____/ ________ |

||

|

month |

day |

year |

2. |

Federal ID Number (EIN) __________________ 2a. N.J. Charities Registration Number: CH- _________________________ |

||

(Leave blank ONLY if this is an initial registration.)

3.Full legal name of the registering organization: ______________________________________________________________

In care of: (if necessary, otherwise leave this line blank) __________________________________________________________

4. Mailing Address: ____________________________________________________________________ £ Change of Address

Street Address |

City |

State |

ZIP Code |

NOTE: If “ in care of,” a postal, private or rural delivery mail box number is used, the street address of the charity must be given below.

5.The principal street address of the registering organization________________________________________________________

|

£ Same as Mailing Address |

Street Address |

City |

State |

ZIP Code |

|

|

|

|

|

|

|

|

|

|

||

6. |

Does the organization have any ofices in New Jersey in addition to the one listed above? |

|

£ Yes £ No |

||

|

If “Yes,” attach a list giving the street address and telephone number of each ofice in New Jersey. |

|

|

||

6a. |

If the street address listed above is not where the organization’s oficial records are kept, or if the organization does not maintain an |

||||

|

ofice in New Jersey, indicate the name, full address, phone and fax number of the person having custody of the organization’s records, |

||||

and to whom correspondence should be addressed.

_______________________________________________________________________________________________________

Contact person |

Street address |

City |

State |

ZIP Code |

________________________________ |

________________________________ |

|

|

|

Telephone number (include area code) |

Fax number (include area code) |

|

|

|

7. Organization’s contact information: |

|

|

|

|

________________________________ |

________________________________ |

|

|

|

Telephone number (include area code) |

Fax number (include area code) |

|

|

|

________________________________ |

________________________________ |

|

|

|

Web site |

|

|

|

|

Form |

Page 1 of 5 |

8.The organization is eligible to ile a Short Form Registration because:

a)It did not receive gross contributions in excess of $25,000 in the preceding iscal year, AND all of the organization’s functions, including

soliciting contributions. |

£ Yes £ No |

b)It is a fraternal, patriotic, social or alumni organization, historical society or similar organization organized under the provisions

of Title 15 of the New Jersey Revised Statutes or Title 15A of the New Jersey Statutes, AND solicitation of contributions is

conined to the organization’s membership and performed by members of the organization. £ Yes £ No

c) It solicits on behalf of a speciied individual, and all contributions, without any deductions whatsoever, will be turned over to |

|

this beneiciary. |

£ Yes £ No |

d)It is a local post, camp, chapter or similarly designated element or county unit, of a bona ide veterans’ organization which issues charters to the local elements throughout New Jersey or to any veterans’ organization chartered under federal law or a

service foundation of such an organization recognized in the organization’s |

£ Yes £ No |

|

e) It is a private foundation that raised less than $25,000 in public contributions. |

£ Yes £ No |

|

Note to question 8: If after reviewing the answers to questions 8a through 8e, none of the statements can be answered “Yes,” the charity is not eligible to use the

9.Have there been changes in the organization’s name, address, Internal Revenue Service (I.R.S.) status, etc. since the date of your

last reporting? £ Yes £ No

If “Yes,” please provide the details on a separate sheet of paper, and provide copies of the documentary proof of a name change

(example: amendment to incorporation) and/or a copy of the letter of determination from the I.R.S. regarding the

9a. Is the organization a chapter or local unit of a parent organization? £ Yes £ No

If “Yes,” write in the full name, address and phone number (include the area code) of the parent organization. Please do not use

abbreviations.

_______________________________________________________________________________________________________

10.Purpose for which the organization was created (write in or attach a statement to this registration): _______________________

______________________________________________________________________________________________________

10a. |

Does the organization solicit or intend to solicit contributions from the general public in the State of New Jersey (including through |

||

|

the sale of merchandise)? |

£ Yes £ No |

|

|

If “Yes,” explain the purpose for which solicited funds are being raised (write in or attach a statement to this registration): |

||

|

_______________________________________________________________________________________________________ |

||

10b. |

Does the organization solicit funds under any other name(s)? £ Yes £ No |

||

|

If “Yes,” please attach to this registration a list of all other names used: _________________________________________ |

||

11. |

Does the organization register or solicit in other states? |

£ Yes £ No |

|

|

If “Yes,” please indicate other states here or, if necessary, attach to this registration a list of those states. __________________ |

||

11a. |

Has the organization ever been enjoined in any jurisdiction from soliciting contributions or has it been found to have engaged in |

||

|

unlawful practices in the solicitation of contributions or the administration of charitable assets? £ Yes £ No |

||

|

If “Yes,” list the jurisdiction and attach copies all of the relevant documents. _________________________________________ |

||

11b. Has the organization’s charity registration been denied, suspended or revoked by any jurisdiction or state? £ Yes £ No

11c. Has the organization voluntarily entered into an assurance of voluntary compliance agreement or any similar order or legal agreement with any jurisdiction, state or federal agency or oficer? £ Yes £ No

Form |

Page 2 of 5 |

12.If the answer to 11a, 11b or 11c is “Yes,” please attach to this registration a statement that provides the details of the action, together with the reason(s) for that denial, suspension, revocation, injunction, compliance agreement etc., including the state or jurisdiction involved, the dates and full copies of all related documents.

Indicate the attachment of documents to this Registration/Veriication Statement by checking this box: £

13.Is the organization currently I.R.S.

If “Yes,” under which section of the code?___________________________________________

14.Has the organization’s

If “Yes,” please attach to this registration a statement providing an explanation, including all of the facts, dates, and all letters and notices received from the I.R.S.

15.Has the organization used an independent paid

If “Yes,” for what purpose(s) are funds being raised? ____________________________________________________________

15a. If the answer to question 15 is “Yes,” write in or provide a separate listing of the name(s) of all independent paid

16.Provide on a separate sheet of paper the name, title, street address, telephone number and salary of each oficer, director and trustee, and the ive

Indicate the attachment of documents to this Registration/Veriication Statement by checking this box: £

16a. Has any person listed in the response to question 16 been adjudged liable in any administrative or civil action, or been convicted

in a criminal action involving theft, fraud or deceptive business practices? £ Yes £ No

If the response is “Yes,” please provide all of the details on a separate sheet and also attach to this registration a copy of the order, judgment or other document(s) indicating inal disposition of the matter.

Please note: For the purpose of question 16a, a plea of guilty, non vult, nolo contendere or any similar disposition of the alleged activity shall be deemed a conviction. A judgment of liability in an administrative or civil action would include a inding

or admission that the individual engaged in an unlawful practice relating to the solicitation of contributions or the administration of charitable assets.

We understand that this registration is being issued at the discretion of the Division of Consumer Affairs and agree that employees of the Division may inspect the records in the possession of this organization in order to ascertain compliance with the statute and all pertinent regulations. We also understand that we may be required to provide additional information if requested.

We hereby certify that the above information and the attached inancial schedule(s) and statement(s) are true. We are aware that if any of the above statements are willfully false, we are subject to punishment.

Signature____________________________ Name______________________________ Title ______________ Date ____________

Signature____________________________ Name______________________________ Title ______________ Date ____________

This form must be signed by two (2) authorized oficers of the organization, including the chief inancial oficer.

Form |

Page 3 of 5 |

Note: If the inancial value of a line item = 0, place a zero in the space provided.

Please report all igures as GROSS, not NET.

Full legal name and street address of the organization

Full legal name:__________________________________________________________________________________________

Fiscal

month day year

Mailing address:

_______________________________________________________________________________________________________

Mailing AddressP.O. Box Number or SuiteCityStateZIP code

Street address of the registering organization: __________________________________________________________________

Street AddressCityStateZIP Code

New Jersey Charities Registration number: CH _______________ |

Telephone number: _________________________ |

|

(include area code) |

A. Revenue

Line A1. |

Contributions & Donations: Includes but is not limited to individual and corporate contributions, donations, legacies, |

|

|

bequests and gross receipts from fundraising: |

|

|

A1a. Direct Public Support ………………………………… |

__________________ |

|

A1b. Indirect Public Support (including donations from other charities) |

__________________ |

|

A1c. Gross Contributions (add lines 1a and 1b) |

__________________ |

Line A2. |

Government Grants .......................................… |

__________________ |

Line A3. |

Other Income |

|

|

A3a. Membership dues and assessments …………………… |

__________________ |

|

A3b. Interest and dividends |

__________________ |

|

A3c. Program service revenue ……………………………… |

__________________ |

|

A3d. Gain from sale of assets |

__________________ |

|

A3e. Other income (please specify on a separate statement): |

__________________ |

|

A3f. Donations from founder(s) of private foundation |

__________________ |

|

A3g. Total other income |

__________________ |

Line A4. |

Total Gross Revenue (add lines A1c, A2 and A3g)… |

__________________ |

B. Expenses

Line B1. |

Program ………………………………… |

__________________ |

Line B2. |

Management, ofice and general expenses……………… |

__________________ |

Line B3. |

__________________ |

|

Line B4. |

Payments to state/national afiliates (if applicable)………………… |

__________________ |

Line B5. |

Total Expenses (add lines B1, B2, B3 and B4)……… |

__________________ |

C. Excess or Deicit

Line C1. Excess or deicit for the |

__________________ |

Please Note: The amount of Gross Contributions ( line A1c on this form) determines the registration fee which must be paid and the

form which should be used. July 2006 revisions to the Charities Registration Act now require all charities to pay a registration fee, including charities whose Gross Contributions are less than $10,000. Further information for charity registrants may be found on our

Web site: http://www.njconsumeraffairs.gov/ocp/charities.htm

Form |

Page 4 of 5 |

Registrants who are qualiied to ile the

must submit the following:

(1)A completed signed

(2)A check or money order in the amount of $30, even if gross contributions did not exceed $10,000. Annual renewal registrations are due within six months of the iscal

(3)Except when submitting an initial registration, the organization’s charities registration number should be written on all checks, forms, attachments, documents etc. being submitted.

(4)If the charity was required by the Internal Revenue Service to ile an

(5)Photocopies of any orders, judgments, agreements or other documents which show the inal disposition of any civil or criminal actions brought against the organization or its board members, marked with the related question number and the charities registration number.

(6)Only initial registrants are required to submit photocopies of the organization’s bylaws, certiicate of incorporation and I.R.S. determination letter. However, copies of these documents must be resubmitted each time they are amended.

(7)Mail the completed registration, enclosures and any attachments to the:

New Jersey Division of Consumer Affairs

Charities Registration & Investigation Section

P.O. Box 45021

Newark, NJ 07101

Should you have questions regarding charities registration in New Jersey, please visit our Web site at http://www.njconsumeraffairs.gov/ocp/charities.htm where registration information, instructions, forms and a fee schedule may be viewed and/or downloaded. After reading through all of the information on our Web site, if you have further questions, please contact the Charities Registration Section at our hotline number

Form |

Page 5 of 5 |

Document Specifications

| Fact Name | Description |

|---|---|

| Eligible Organizations | Charitable organizations domiciled or conducting business in New Jersey, receiving gross contributions of $25,000 or less per year, are required to use Form CRI-200 for initial and annual renewal registrations. |

| Exemption Criteria | Organizations receiving less than $10,000 per year and not compensating anyone for fundraising activities are exempt from registration, although they may voluntarily register. |

| Registration Fee | The registration fee for using Form CRI-200 is $30, applicable to both initial registration and renewals. |

| Payment Method | Fees must be paid by check or money order, made payable to the “New Jersey Division of Consumer Affairs”. |

| Form Submission Address | Completed forms, along with the appropriate fee, should be mailed to the New Jersey Division of Consumer Affairs, Charities Registration & Investigation Section, P.O. Box 45021, Newark, NJ 07101. |

| Governing Laws | The registration process is governed by the New Jersey Charitable Registration and Investigation Act, requiring certain charitable organizations to register and report annually. |

Detailed Steps for Using Cri 200 Nj

Completing the CRI-200 form is a required step for charitable organizations in New Jersey that receive gross contributions of $25,000 or less per year. This process involves both initial registration and annual renewal. Correctly filling out and submitting this form ensures compliance with the state's regulations on charitable activities. Below is a step-by-step guide designed to assist in accurately completing the form.

- Choose between Initial and Renewal Registration by checking the appropriate box at the top of the form.

- Fill in the fiscal year-end date for which this registration applies in the format mm/dd/yyyy.

- Provide the organization's Federal ID Number (EIN).

- Enter the New Jersey Charities Registration Number, if renewing. Leave blank if this is an initial registration.

- State the full legal name of the organization.

- If applicable, specify the name the registration is in care of, or leave blank.

- Provide the organization’s mailing address, including street address, city, state, and ZIP code.

- Indicate if there is a change of address by checking the appropriate box.

- Supply the principal street address of the organization if different from the mailing address.

- Answer whether the organization has any offices in New Jersey aside from the one listed. If “Yes,” attach a list with details.

- For organizations not keeping official records at the listed office or without a New Jersey office, provide the contact person’s name, address, and contact information.

- Record the organization’s primary contact information, including telephone number, fax number, email address, and website.

- Determine eligibility for using the Short Form CRI-200 by reviewing the criteria listed and checking “Yes” or “No” accordingly.

- Note any changes in the organization's name, address, IRS status, etc., since the last reporting. Attach additional sheets if necessary.

- State the purpose for which the organization was created. Attach a separate statement if needed.

- Detail whether the organization solicits contributions from the general public in New Jersey, and for what purpose.

- Indicate if the organization solicits under any other names. Attach a list of all such names if applicable.

- Answer if the organization registers or solicits in other states and provide details or an attached list as required.

- Reveal any legal or administrative actions against the organization related to its charitable activities. Attach documents as necessary.

- Confirm the organization's IRS tax-exempt status and provide the applicable section of the code.

- Detail any interactions with independent paid fundraisers, fundraising counsel, or commercial co-venturers.

- On a separate sheet, list the names, titles, and compensation of key organization members and staff, marking the corresponding box to indicate attachment.

- Sign and date the form by two authorized officers of the organization, including the chief financial officer.

Once completed, the form along with the attachments and a check or money order for the registration fee made payable to the “New Jersey Division of Consumer Affairs” should be mailed to the address provided. It is crucial to adhere to submission deadlines to avoid late fees. Organizations are encouraged to keep a copy of the completed form and all attachments for their records.

Learn More on Cri 200 Nj

What is the Form CRI-200?

Form CRI-200 is a Short-Form Registration/Verification Statement required for charitable organizations that are domiciled in or conduct business in New Jersey and receive gross contributions of $25,000 or less per year. It is used for both initial registration and annual renewal of the charity's registration with the New Jersey Office of the Attorney General, Division of Consumer Affairs, Office of Consumer Protection Charities Registration Section.

Who needs to file Form CRI-200?

Charitable organizations in New Jersey that receive gross contributions of $25,000 or less annually. However, if the organization's contributions are less than $10,000 per year and it does not compensate anyone for soliciting or conducting fundraising activities, it is exempt from registration but may still opt to register.

What is the registration fee for Form CRI-200?

The registration fee is $30 for charities with gross contributions between $0 to $25,000. This fee applies to both initial registrations and renewals. The check or money order for the fee should be made payable to the "New Jersey Division of Consumer Affairs."

What information is required on Form CRI-200?

- Designation if the form is for an initial or renewal registration.

- Federal ID Number (EIN) and NJ Charities Registration Number (if not an initial registration).

- Full legal name, mailing, and principal street addresses of the organization.

- Details about additional offices in New Jersey, if any.

- Contact information for the organization and the person holding the organization's records.

- Information regarding eligibility for filing the Short-Form based on the organization's gross contributions and the nature of its activities.

- Details of any changes in the organization’s name, address, IRS status, etc.

- Purpose for which the organization was created and information about fundraising activities.

Can Form CRI-200 be used by all charities in New Jersey?

No, Form CRI-200 can only be used by charities that meet specific criteria such as receiving gross contributions of $25,000 or less and conducting all their functions, including fundraising, through volunteers, members, officers, or persons who are not compensated. Charities that do not meet these conditions must use the Long-Form Initial Registration Statement CRI-150-I or the Long-Form Renewal Statement CRI-300R.

When is Form CRI-200 due?

The completed Form CRI-200 must be submitted within six months of the end of the fiscal year for which registration is sought. If filed after the due date, a $25 late fee is also due.

Where should Form CRI-200 be mailed?

Mail the completed form, along with the necessary fee and any other required documents, to: New Jersey Division of Consumer Affairs, Charities Registration & Investigation Section, P.O. Box 45021, Newark, NJ 07101.

How can I get more information or assistance with Form CRI-200?

For more information or assistance with the Form CRI-200, visit the New Jersey Division of Consumer Affairs’ website at http://www.njconsumeraffairs.gov/ocp/charities.htm or contact the Charities Registration Section at their hotline number (973)-504-6215 during regular business hours.

Common mistakes

When filling out the Form CRI-200 in New Jersey, individuals often make mistakes that can lead to delays or issues with their charitable organization's registration process. Below is a detailed list of common errors to avoid:

- Not checking the correct box at the beginning of the form to indicate whether the submission is for an Initial or Renewal Registration. This simple step can cause confusion about the organization's registration status.

- Leaving the Charities Registration Number blank on a renewal registration. This number is crucial for identifying the organization's previous submissions and records.

- Providing incomplete or incorrect organization legal name or mailing address. The form requires accurate information to ensure proper communication and legal registration.

- Forgetting to note a change of address by not ticking the specified box if the organization's address has changed since its last registration.

- Omitting additional office locations within New Jersey. All locations must be listed to comply with state regulations.

- Failing to provide contact details for the person who has custody of the charity's official records, especially if they are kept at a different address.

- Skipping question 8 concerning eligibility criteria for filing the Short Form CRI-200, which could result in using the incorrect form for the organization's situation.

- Not updating the form when there have been changes in the organization's name, address, or IRS status since the last filing. Accurate and current information is essential for compliance and communication.

- Incorrectly answering or leaving blank the questions concerning the organization's fundraising activities, such as whether it solicits under other names or in other states. This information helps to understand the scope of the organization's fundraising efforts.

- Neglecting to attach required documents, such as a list of officers and salaries or proof of tax-exempt status changes, can hinder the registration process. Each question that requires an attachment is marked, and failing to include these attachments can result in an incomplete application.

Ensuring all information is correct and complete, and attaching all required documents, will facilitate a smoother registration process for charitable organizations in New Jersey.

Documents used along the form

When an organization in New Jersey files the Form CRI-200 for charitable registration, several other documents and forms are commonly used in conjunction to ensure compliance with all state charity laws and regulations. Understanding these documents can help organizations streamline their registration process and remain in good standing.

- IRS Form 990: This form is required by the IRS for tax-exempt organizations to provide annual financial information. It is often needed alongside the CRI-200 to give a complete picture of the organization’s financial status.

- Articles of Incorporation: This document officially creates the organization and is filed with the New Jersey Division of Revenue. It outlines the fundamental management structure and purpose of the nonprofit.

- Bylaws: Bylaws govern the internal operations of an organization, such as procedures for meetings, elections, and duties of directors and officers. They do not require state approval but may need to be submitted with the CRI-200 for initial registration or if there have been amendments.

- IRS Determination Letter: This letter from the IRS confirms the organization's tax-exempt status. It is crucial for proving exemption from federal income tax and often must be submitted with the CRI-200.

- Financial Statements: Audited financial statements might be required for larger charities. These provide a detailed overview of the organization's financial health and are useful for both internal and external purposes.

Conflict of Interest Policy: While not always mandatory, a conflict of interest policy is recommended best practice for nonprofits. This policy helps ensure decisions are made in the organization’s best interest rather than personal gain. - Form CRI-300R: For charities that have gross contributions exceeding $25,000, the Long-Form Renewal Statement CRI-300R is required for annual renewal rather than the CRI-200.

- List of Officers and Directors: This list, including contact information, must be updated regularly and submitted as changes occur. It is crucial for the CRI-200 registration process and general organizational management.

Together, these documents form a comprehensive package that supports the registration and ongoing compliance of charitable organizations in New Jersey. By staying informed and organized, organizations can effectively navigate the regulatory landscape, maintain their good standing, and focus on their mission-driven work.

Similar forms

The Form CRI-200 shares similarities with the IRS Form 990-EZ, primarily in serving non-profit organizations with less complex financial activities. Both forms are designed for smaller entities, with the CRI-200 being for those with gross contributions of $25,000 or less and the 990-EZ targeting small to medium non-profits. Each form requires basic financial data, organizational structure details, and information on fundraising activities, aiming to simplify the reporting process while ensuring compliance and transparency.

Another related document is the IRS Form 1023, which is an application for tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. Much like the CRI-200, Form 1023 is geared towards charitable organizations. However, while the CRI-200 is more focused on annual registration with New Jersey's Division of Consumer Affairs, Form 1023 is concerned with establishing an organization's initial eligibility for exemption from federal income tax.

The California Charities Registration Form shares a purpose with the CRI-200, as both are required for charitable solicitation within their respective states. Although each state has its specific thresholds and exemptions, the underlying goal is to provide state officials with sufficient information to regulate charitable activities, protect donors, and ensure that charities are using their funds appropriately. These forms collect details on finances, activities, and governance to aid in oversight and transparency.

The Uniform Registration Statement (URS) facilitates charitable solicitation registration across multiple states, including New Jersey, offering an alternative to the state-specific form like CRI-200 for organizations fundraising in multiple states. However, the CRI-200 is tailored specifically to New Jersey's statutory requirements and fees, whereas the URS tries to harmonize the differing requirements of various states into a single form, potentially simplifying the registration process for charities operating nationally.

Form CRI-300R, the long-form renewal statement for New Jersey, caters to more substantial organizations than the CRI-200. While both forms serve the purpose of annual registration for charities, the CRI-300R is required for those receiving more than $25,000 in gross contributions, demanding more detailed financial information and supporting documents. This differentiation allows the Division of Consumer Affairs to tailor its oversight to the size and scope of the organization.

The New York Charities Bureau's Annual Filing for Charitable Organizations (Form CHAR410) parallels the CRI-200 in its fundamental goal of annual charity registration and disclosure. Both forms request financial data, operational information, and details about fundraising practices. However, New York's requirements and thresholds for filing may differ, reflecting the state's specific regulatory environment and oversight intentions for charitable entities.

The Pennsylvania Bureau of Corporations and Charitable Organizations' Charitable Organization Registration Statement is another document with a similar purpose to the CRI-200, aiming to regulate charities operating within the state. While both forms ensure that organizations comply with financial and operational transparency, Pennsylvania’s form is part of a broader regulatory framework, emphasizing the common goal among states to protect the public and maintain charity integrity.

Form 990-N, also known as the e-Postcard, is an IRS requirement for small exempt organizations typically earning $50,000 or less in gross receipts. Its link to the CRI-200 lies in its intent to streamline the reporting process for small entities. Both forms recognize the administrative burden on smaller charities and offer simplified reporting solutions while ensuring necessary regulatory oversight and public transparency.

The IRS Form 8868 is an application for Extension of Time to File an Exempt Organization Return. It is indirectly related to the CRI-200 through the need for some organizations to delay their filing due to various reasons. The ability to request extensions reflects the understanding that circumstances might prevent timely reporting. Both federal and state levels offer mechanisms to ensure compliance without undue hardship on charitable entities.

Lastly, the Colorado Charities Registration Statement mirrors the CRI-200 in purpose, as both are vital for charity regulation within their respective states. Each form encapsulates the specific legal requirements, operational thresholds, and reporting mandates tailored to the state’s charitable sector, underlying a nationwide effort to ensure that charities act in the public’s interest through transparency and accountability in their fundraising practices.

Dos and Don'ts

When filling out the Form CRI-200 in New Jersey, it's important to approach the process with care and attention to detail. The goal is to ensure that your charitable organization complies with state requirements, avoiding any issues that could arise from missteps. Here is a thoughtful guide on the dos and don'ts:

- Do:

- Ensure that all questions are answered. Leaving questions unanswered can result in the rejection of the form.

- Verify the accuracy of your organization's contact information, including the principal street address and mailing address. Accurate contact information is crucial for effective communication.

- Include the correct registration fee by check or money for the amount of $30, payable to the "New Jersey Division of Consumer Affairs." Correct payment is essential for the processing of your form.

- Attach a list of additional offices in New Jersey, if applicable, including their street addresses and telephone numbers. This information helps maintain transparency about your organization's operations within the state.

- Provide details on any changes in the organization's name, address, IRS status, etc., since the last reporting period, along with the necessary documentary proof. This keeps your records up to date and prevents any discrepancies.

- Check the box that corresponds to the appropriate registration type at the beginning of the form, whether it's an initial registration or a renewal. This ensures your submission is processed correctly.

- Attach all required documents, including a financial statement and any other requested attachments, indicating their inclusion by checking the relevant box. Complete documentation supports the credibility and transparency of your organization.

- Sign the form with two authorized officers of the organization, including the chief financial officer. Proper authorization is a key compliance requirement.

- Don't:

- Forget to list all other names under which the organization solicits funds, if applicable. This omission could lead to legal complications.

- Overlook attaching the IRS-990 form if your charity was required to file one for the fiscal year being reported. This form is critical for verifying your financial information.

- Ignore the need to attach explanations for any "Yes" responses to questions about legal actions against the organization. Transparency in these matters is crucial for maintaining public trust.

- Leave the federal ID number (EIN) or the NJ Charities Registration Number sections blank if this is a renewal registration. These identifiers are crucial for linking your form to your organization's records.

- Miss the deadline for annual renewal registrations, which is within six months of the fiscal year-end. Late submissions incur additional fees and can jeopardize your standing.

- Fail to update your organization's contact information if it has changed since the last submission. Accurate and current information is essential for official communications.

- Submit incomplete forms or documentation. Incompleteness can delay processing and potentially lead to the rejection of your registration.

- Make the check payable to an incorrect entity. Remember, the fee should be made payable to the "New Jersey Division of Consumer Affairs."

Filling out the Form CRI-200 with diligence and attention to these guidelines will help ensure a smoother process for maintaining your charitable organization's compliance in New Jersey.

Misconceptions

Many misconceptions exist about the New Jersey Form CRI-200, which is essential for charitable organizations in the state. Below are nine common misunderstandings clarified:

- Only large charities need to register. In fact, charitable organizations operating or fundraising in New Jersey with gross contributions of $25,000 or less per year must submit a CRI-200 form for initial registration and annual renewal.

- Organizations exempt from registration do not benefit from registering. Even if an organization receives less than $10,000 per year and does not compensate anyone for fundraising, registering can lend credibility and transparency, despite being exempt.

- The registration fee varies based on the charity’s size. The truth is the registration fee for charities with gross contributions between $0 and $25,000 is a flat $30, regardless of the organization's size.

- Only initial registrations require a fee. Both initial and renewal registrations carry a $30 fee, contrary to what some may believe.

- All charities are required to use Form CRI-200. The CRI-200 is specifically for charities that receive gross contributions of $25,000 or less. Others must use the long-form CRI-150-I for initial registration or CRI-300R for renewal.

- Charities do not need to report changes in their organization. If there have been changes in the organization’s name, address, IRS status, etc., since the last report, these need to be detailed on a separate sheet along with the form.

- Submission of IRS-990 forms is optional. If the charity is required by the IRS to file any version of the IRS-990 form for the fiscal year being reported, it must be submitted alongside the CRI-200 form.

- Organizations filing the CRI-200 form can delay submitting their financial statements. The completed and signed CRI-200 form, including financial statements and schedules, must be submitted within six months of the fiscal year-end.

- Form adjustments or amendments can be made informally. Any changes to the organization, including bylaws, incorporation certificates, and IRS determination letters, must be formally resubmitted with the registration if they are amended.

Understanding these points is vital for charitable organizations to ensure compliance with New Jersey’s Division of Consumer Affairs and maintain good standing in their charitable endeavors.

Key takeaways

Here are eight key takeaways for navigating the completion and usage of the New Jersey Form CRI-200 for charitable organizations:

- Eligibility Criteria: Charitable organizations operating or domiciled in New Jersey with gross contributions of $25,000 or less per year are required to either initiate or renew their registration using Form CRI-200.

- Exemption Possibility: Organizations receiving less than $10,000 per year and not compensating individuals for fundraising activities can opt out of registration, though registration remains available to them.

- Registration specifics, such as if it's an initial or renewal registration, must be clearly indicated on the form.

- The registration fee for eligible charities is set at $30, payable to the “New Jersey Division of Consumer Affairs” at the time of form submission.

- Organizations exempt from registration based on their operating model, the nature of their solicitation, or affiliated status can identify this through specific checkboxes on the form.

- In cases of address or operational changes, detailed explanations and relevant documents should be provided as attachments.

- The form requires identification of solicitation activities beyond New Jersey borders, legal injunctions against soliciting, or any previous denial, suspension, or revocation of registration in any jurisdiction.

- For complete submission, the form mandates inclusion of the financial statement, checks for the applicable fee, IRS documents if required, and any additional information prompted by answers within the form. Subsequently, all submissions should be directed to the Charities Registration & Investigation Section in Newark, NJ.

Form CRI-200 not only facilitates a transparent registration or renewal process for charities but also ensures compliance with New Jersey state requirements, maintaining public trust in the charitable sector.

Popular PDF Documents

Proof of Service Nj - Includes an affirmation section for nominators to certify the accuracy and truthfulness of the information provided.

Abandoned Property Nj - Claimants must affirm their legal authority to claim the property by signing the form and checking a legal disclaimer.

Njcaa Ejection - The form distinguishes between violent and non-violent ejections, providing insight into the nature of the infractions.