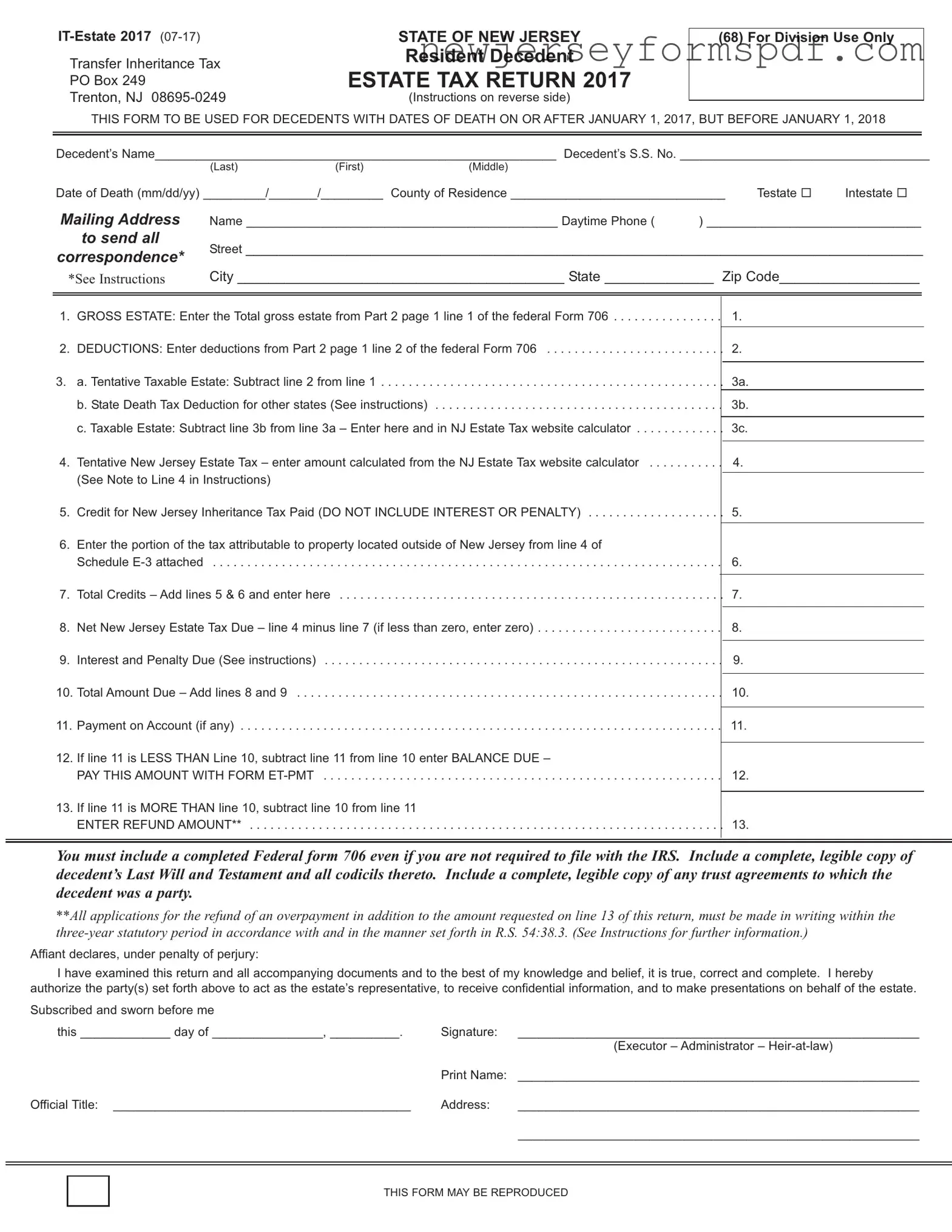

Fill Out a Valid New Jersey Estate Tax Return Template

Diving into the world of estate management in New Jersey, it's essential to understand the nuances of the New Jersey Estate Tax Return form, formally known as IT-Estate 2017. This form serves as a critical tool for settling the financial obligations of a resident decedent's estate to the State of New Jersey. With the state imposing taxes on estates that exceed a certain value threshold, it's imperative for executors and estate administrators to carefully navigate through this document. Completing this form accurately requires an in-depth analysis of the decedent's assets, deductions, and applicable tax credits. The form mandates the inclusion of a completed Federal form 706 for correlating federal estate tax considerations, regardless of whether filing with the IRS is necessary. Additionally, it calls for a clear copy of the decedent's Last Will and Testament along with any trust agreements and stipulates strict guidelines for applying for refunds of overpayments. It not only outlines the taxable estate calculations but also integrates provisions for estate tax waivers, payment procedures, and the potential impacts of lien requirements on property transfers. Ensuring compliance with these detailed instructions is crucial to smoothly processing estate tax returns, securing necessary waivers, and efficiently addressing any refund requests, thereby avoiding processing delays and potential legal complications.

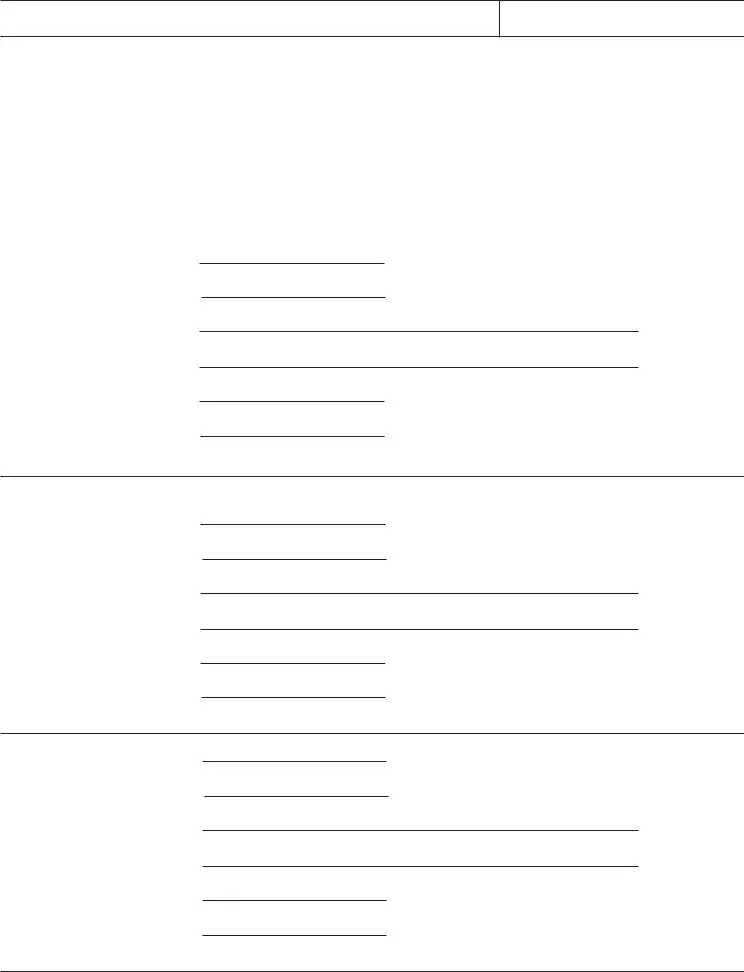

Sample - New Jersey Estate Tax Return Form

STATE OF NEW JERSEY |

|

TrasferIheritaceTax |

Resident Decedent |

|

|

PO x |

ESTATE TAX RETURN 2017 |

TretN |

structisreverseside |

TISORTO USORTSWITTOTONORT |

UYTORUY |

(68) For Division Use Only

ecedet’sNa_______________________________________ |

___________________ecedet’sSSN______________ |

______________________ |

||||||

|

ast |

irst |

dde |

|

|

|

|

|

atefeathddyy_________________________u |

|

tyfResidece__________________ |

_____________ |

Testate |

Itestate |

|||

MailingAddress |

Na_____________________________________________ |

aytiPhe |

_______________________________ |

|

||||

to send all |

Street _______________________________________________________________________________________ |

|||||||

correspondence* |

||||||||

*SeeInstructions |

ity __________________________________________Stat e______________Zide__________________ |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

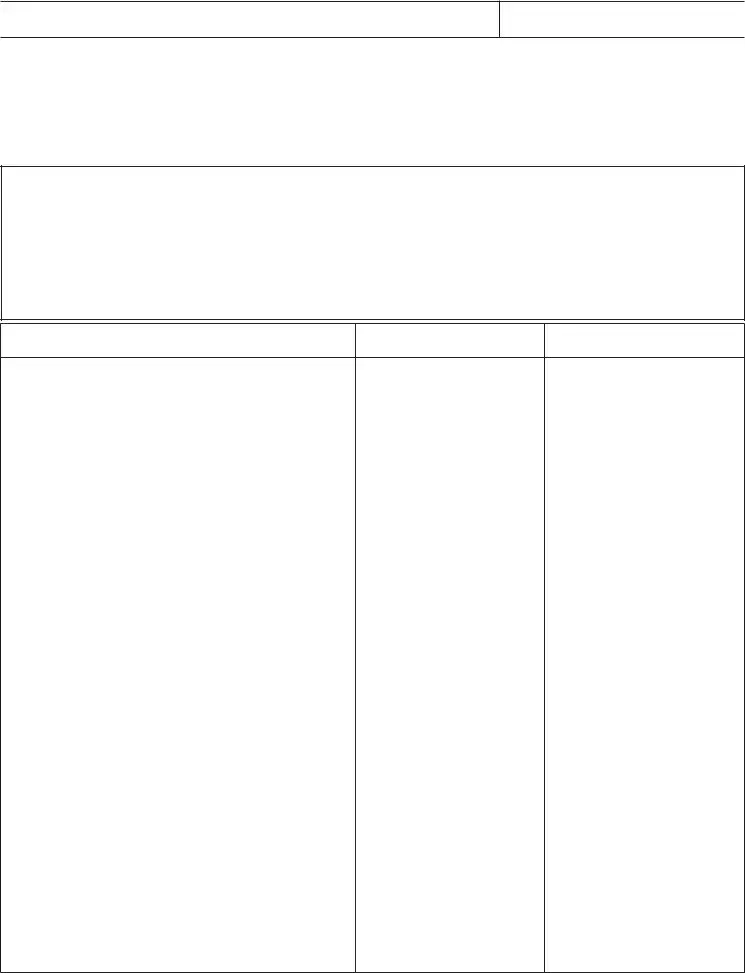

ROSSTtertheTtagrssestatefrPartagei |

efthefederar |

|

UTIONSterdeductisfrPartageieft |

hefederar |

|

aTetativeTaxabeateSubtractiefrie |

a |

|

bStateeathTaxeductifrtherstateseistructi |

s |

b |

cTaxabeateSubtractiebfriea– terherea |

diNateTaxwebsitecacuatr |

|

TetativeNewrseyateTax– eterautcacuatedfrt |

heNateTaxwebsitecacuatr |

|

eNtetieiIstructis |

|

|

reditfrNewrseyIheritaceTaxPaidONOTINUIN |

TORPTY |

|

terthertifthetaxattributabetrertyca |

tedutsidefNewrseyfrief |

|

Schedueattached |

|

|

Ttaredits– diesadeterhere |

|

|

NetNewrseyateTaxue– ieusiefesst |

hazereterzer |

|

IterestadPeatyueeistructis |

|

|

Ttautue– diesad |

|

|

Paytutfay |

|

|

IfieisTiesubtractiefri |

eeterU– |

|

PYTISUNTWITOR |

|

|

IfieisRTiesubtractiefri |

e |

|

TRUNUNT |

|

|

c

You must include a completed Federal form 706 even if you are not required to file with the IRS. Include a complete, legible copy of decedent’s LastWill and Testament and all codicils thereto. Include a complete, legible copy of any trust agreements to whichthe decedent was a party.

**Allapplicationsfor therefundofan overpayment in additiontothe amountrequested online 13 ofthis return, must be madein writingwithinthe

fiatdecaresudereatyferjury |

|

|

|

|

|

Ihaveexaedthisreturadaaccayigdcutsadt |

|

thebestfwedgeadbeiefitistruecrrecta |

dceteIhereby |

||

authrizetheartysetfrthabvetactastheestate’srere |

setativetreceivecfidetiaifrtiadt |

resetatisbehafftheestate |

|||

Subscribedadswrbefre |

|

|

|

|

|

this_____________dayf_________________________ |

_ |

Sigature |

_________________________________________ |

_________________ |

|

|

|

|

cutr– istratr– eirtaw |

|

|

|

|

PritNa |

___________________________________________ |

_______________ |

|

OfficiaTite _____________________________________ |

______ |

dress |

_________________________________________ |

_________________ |

|

|

|

|

__________________________________________________________ |

||

|

|

|

|

|

|

|

|

|

|

|

|

TISORYROU

Estate Tax Return 2017 Instructions

Thisfristbeusedyfrtheestatefaresidetdece |

dethavigadatefdeathrafteruary |

butbefreuary |

__________________________________________________________________________________________ |

||

TheNateTaxisiadditittheNIheritaceTax |

taxisisedutheestatefeveryresidetdecedetha |

vigadatefdeathrafter |

uarybutbefreuarywhsetaxabee |

stateexceeds$iasdeteredursuattsecti |

ftheederaItera |

ReveuedeUSsieffectuary |

|

|

Filing Requirements |

|

|

rdecedetsdyigrafteruarybutbefre |

uaryaNewrseyestatetaxreturstbefiedif |

thedecedet’sgrssestate |

exceeds$iasdeterediaccrdacewiththervisi |

sftheIteraReveuedeieffectuary |

|

Completing the Return

Mailing Address – Complete the Mailing Address section with the name and address of the person or firm that will be authorized to receive all

communications from the Division of Taxation. NteTheivisiisrequiredtdeaywiththisers |

rfiruesstheestatereresetativehas |

|

|

ascetedr ittfTaxayerReresetative |

|

|

|

Complete Federal Form 706* icudigascheduesadsurtigdcutsThisstbe |

cetedeveifyuweretrequiredtfiewiththe |

|

|

federaIteraReveueServiceRSIfyuarerequiredtf |

ierdidfierwiththeIRSsubtacyfw |

hatwasactuayfied |

NOTE: Be |

sure to answer question 2(c) on Schedule M to avoid processing delays.

*Refers to the (Rev. August 2013) version of Form 706.

Complete lines 1 through 13 of the 2017 New Jersey Estate Tax Return. |

|

|

|

|||

Instructions for Line 3b. State Death Tax Deduction for Other States: tertheautfayestateiheritaceegacyrsuccessi |

|

taxesactuay |

||||

aidtaytherStateNOTicudeNewrseyrthei |

|

|

strictfuiaayrertyicudedithegrssestate |

|

|

iefthisretur |

Note to Line 4: Thewebsiteestatetaxcacuatricrratesacreditf$ |

whichisequatthetaxduethe$iexc |

|

usiautfr |

|||

Itaserfrthecircuarcacuaticreatedbyaica |

|

|

tiftheNewrseyrtifthefederaStateeath |

|

|

Taxeductitthetaxabe |

estateiaccrdacewithSectiftheederaIte |

|

raReveuede |

|

|

|

|

Waiver Request Schedules: Complete Schedules |

uesfthe |

|||||

aretsufficietfrwaiverurses |

Only list those assets which require waivers. See instructions on each schedule for guidance. |

|||||

Required Documents |

|

|

|

|

|

|

cyfaycicatifrtheIRSregardigtheateTa |

|

x |

|

|

|

|

ceteegibecyfthedecedet’sastWiad |

|

Testatadacdicistheret |

|

|

|

|

cyfaytrustagreetstwhichthedecedetwasaa |

rtyad |

|

|

|

||

cyfthedecedet’sastfuarfederaictaxretu |

|

rfiedrirtdeath |

|

|

|

|

Interest Rates and Payment Due Date |

|

|

|

|

|

|

IterestaccruesattherateferauayNateT |

|

|

axtaidwithiiethsfthedecedetsdatef |

|

deathIfaextesiftit |

|

fiethefederaestatetaxreturisgratedtheirectr |

|

yreduceiterestterauutitheearierfthee |

|

xiratifthefederaextesir |

||

thedatefthefiigfthefederareturwiththe |

IRS |

|

|

|

|

|

Requestsfraiterestreductistbeaccaiedbyacy |

|

|

ftherequestdettheIteraReveueServicefraexte |

|

sitfiethefedera |

|

estatetaxreturagwithacyfayrequiredarvaa |

|

|

dverificatiastthedatewhichthefederaestate |

|

taxreturwasactuayfied |

|

Paytsarefirstaiedttheiterestifaywhichhas |

|

accruedtthedatefayt |

|

|

|

|

Payments on Account / Refund Requests |

|

|

|

|

|

|

Paytsaccutybedeataytitavidfurtheraccrua |

|

|

fiteresttheautaidIaycasewherethea |

|

|

utaidaccut |

frNewrseyIheritaceratetaxesexceedstheautfta |

|

xdueafterthefiaassessthasbeedetheveraida |

|

utwiberefuded |

||

itheduecursefbusiess |

|

|

|

|

|

|

rtectiverefudcaishudbederITwithi |

|

|

threeyearsfrthedatefaytrtectiverefudcaii |

|

|

sacaifiedtrtect |

ataxayer’srighttatetiarefudbasedacti |

|

getevetfrwhichthestatutefitatisisabutt |

exire |

rtectivecaiisusuaybased |

||

ctigeciessuchasedigitigatiragig |

|

federaestatetaxaudit |

|

|

|

|

Lien |

|

|

|

|

|

|

rresidetdecedetsdyigaftereceertheN |

|

|

ateTaxreisaiearertyfthedecedetasf |

|

|

thedatefdeathutiaid |

Nrertyybetrasferredwithutthewrittecsetft |

|

|

heirectrftheivisifTaxati |

|

|

|

NEW JERSEY INHERITANCE AND ESTATE TAX:

RETURN PROCESSING INSTRUCTIONS

Follow these procedures to avoid delays in processing returns, waivers, and refunds:

DO NOT enclose returns in any kind of BINDER, SEALED FOLDER or

NOTEBOOK.

DO NOT use STAPLES (especially

OIt is OK to use rubber bands or clips to keep the file together.

O

DO NOT enclose DUPLICATE COPIES of returns or duplicates of other documents.

OWhen filing both Inheritance and Estate Tax, include only ONE copy of the will, trusts, income tax return, 706, appraisals, and any other attachments.

A few things to DO:

STAPLE checks to the completed payment voucher, and put voucher on

TOP.

OMake sure checks are signed, and made payable to “New Jersey Inheritance and Estate Tax”

OInclude the Decedent’s name and SS# on the check.

Place the return and schedules on top (if no payment), with the will and other supporting documents beneath.

Check that returns are SIGNED by the legal representative of the estate and NOTARIZED.

OThe representative’s name should be printed clearly beneath the signature

VERIFY the decedent’s social security number and date of death.

Make sure the MAILING ADDRESS on the return is correct – and indicates the person who you want to receive ALL correspondence (letters, bills, waivers, etc).

OThe Division cannot correspond with your attorney or CPA unless they are listed on the front page of the return.

Clearly mark amended returns as “Amended” along the

BOTTOM of the return.

File Inheritance Tax and Estate Tax returns together when

possible.

OKeep the two returns separate within the same envelope or box.

OKeep in mind the two taxes have separate due dates for payment of the tax.

OInclude separate checks and vouchers for each tax.

Thisageitetiayeftba

( |

T |

|

rnsernheritnx |

TT |

|

TTT |

||

x |

||

ttTxynt |

||

renton |

||

|

||

TTTT |

|

oiisionsnly

T

edentsme_______________________________________ |

_____________________________________________ |

|||||

|

(st |

(irst |

|

(ddle |

|

|

edentso_________________________________ |

|

_ |

|

|

|

|

teoeth(mmdd_________________________ou |

|

ntoResiden__________________ |

_______________ |

|||

MailingAddress |

me_____________________________________imeone |

(_____________________ |

||||

tosendall |

treet______________________________________________ |

_______________________________ |

||||

correspondence |

||||||

|

it______________________________________ |

tte____ |

________ |

ipode________ |

||

|

|

|

|

|

|

|

TToTTin)

(ode |

tex(totloeremittedwiththisorm |

____________________________ |

TT

ntsonuntmemdetntimetovoidurtherl orthereundonoverpntmustemdeinwritinwith themnnersetorthinR(texndR

ointerestonthemountsopidlpplitions inthethreersttutorperiodinrdnwithndin (nheritnx

kcckspyltonitncndttTx oxTnton

ncluddcdntsnndsocilscuitynuon cck)

remittinmorethnoneelisteeindividullelow

olle(teronineove

Thisageitetiayeftba

T’SN

T’SSOISURITYNU

|

SCHEDULE |

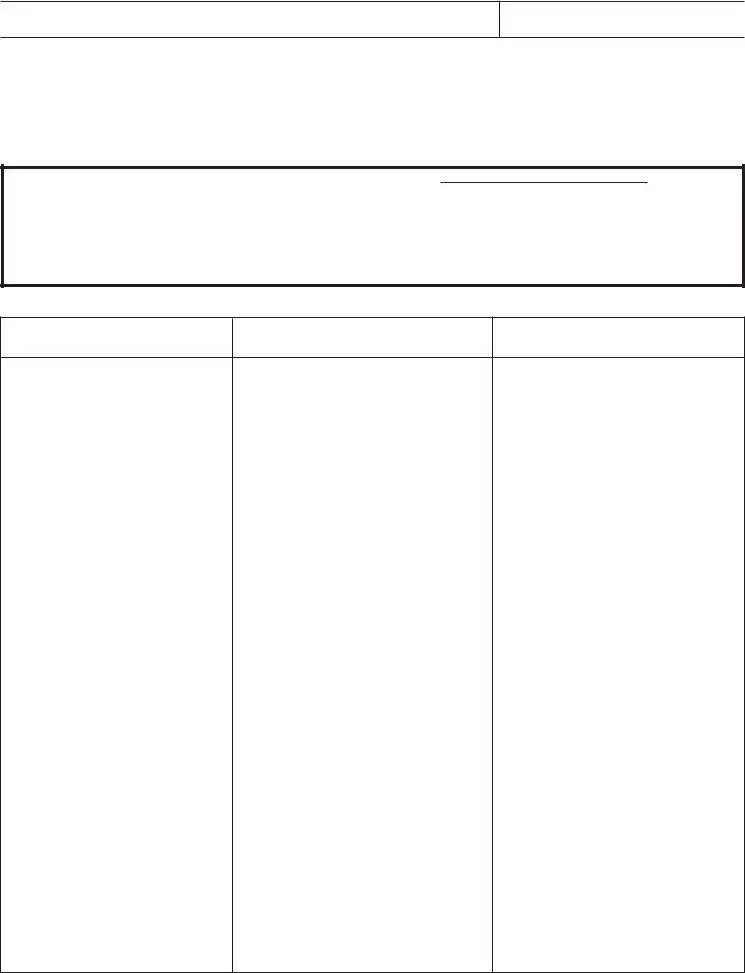

reditfrrtiftaxattributabetrertycated |

utsideNewrsey |

|

||

|

|

|

|

|

||

|

Igeeraitagibeersarertyiscsideredtbe |

catediNewrseyregardessfwhereityactuaybecat |

ed |

|||

|

|

|

|

|

||

|

rssvauefrertycatedutsideNewrseyicuded |

iefthefirstagef |

|

|

||

|

thisretur |

|

|

|

|

|

|

|

Prerty |

|

aue |

|

|

|

|

|

|

|

||

|

___________________________________________________________ |

_______________________ |

|

|

||

|

___________________________________________________________ |

_______________________ |

|

|

||

|

___________________________________________________________ |

_______________________ |

|

|

||

|

___________________________________________________________ |

_______________________ |

|

|

||

|

___________________________________________________________ |

_______________________ |

|

|

||

|

___________________________________________________________ |

_______________________ |

|

|

||

|

Usesearatesheetifecessary |

|

|

|

|

|

|

Newrseygrssestatewherevercatedutistedie |

|

fthefirstagefthisretur |

|

|

|

|

TetativeNewrseyateTaxutistedief |

thefirstagefthisretur |

|

|

||

|

|

|

||||

|

wabecreditivideiebyieadtiyby |

ieterhereadiefthefirst |

|

|

||

|

|

|

||||

|

agefthisretur |

|

|

|

|

|

|

|

|

|

|

|

|

T’SN

T’SSOISURITYNU

SCHEDULE

WAIVER REQUEST SCHEDULE

NEW JERSEY REAL PROPERTY

Note: All items on this schedule must be reported on the Form 706

istaNSRPROPTYiwhichthedecedetheda |

|

iterest |

|

|

|

Rertfractiashares |

only iftherertywashedasteats |

|

|

|

|

trertrertyhedasteatsyhetiretyifsuseci |

viuiarterissurvivig |

|

|||

Taxwaiverswitbeissuedfrassetstistedthissche |

due |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

ecedet’sShare

uty

StreetadNuer

iciaity

t

c

TiteOwerfRecrd

ecedet’sShare

uty

StreetadNuer

iciaity

t

c

TiteOwerfRecrd

ecedet’sShare

uty

StreetadNuer

iciaity

t

c

TiteOwerfRecrd

fadditiasaceisrequiredattachridersfthesasize frybererduced

T’SN

T’SSOISURITYNU

SCHEDULE

WAIVER REQUEST SCHEDULE

NEW JERSEY BANK ACCOUNTS/CREDIT UNIONS/BROKERAGE ACCOUNTS

Note: All items on this schedule must be reported on the Form 706

istaassetshedi |

New Jersey bagistitutiswhichdecedet’saisisted |

|

|

||||

hisyicudechecgaccutssavigsaccutseyrts’s |

|

adIR’s |

|

||||

Icudetheafeachbaristitutiadaccut |

uertieaccutsi |

||||||

ebaybegruedtgetherbuteachaccutstbe |

istedsearatey |

||||||

Stateaas |

|

|

registeredeachaccut |

|

|

||

isty |

|

|

the full datefdeathbaacefeachaccutthisschedue |

|

|

||

Taxwaiverswitbeissuedfrassetstistedthissche |

due |

||||||

Brokerage Accounts must list total valueof account, rather than individual assets.

(A)

New Jersey Accounts

(B)

Registered Name(s)

(C)

Full Date of Death Value

fadditiasaceisrequiredattachridersfthesasize frybererduced

T’SN

T’SSOISURITYNU

SCHEDULE

WAIVER REQUEST SCHEDULE

NEW JERSEY STOCK ONLY

Note: All items on this schedule must be reported on the Form 706

istONYstcicrrateditheStatefNewrseywhi chdecedet’saisisted

Rerttheuerfshareswedfeachstc

isttheafthecayadaas |

|

registeredeachstc |

|

Taxwaiverswitbeissuedfrassetstistedthissche |

due |

||

Stocks held in a Brokerage Account should notbe listed on this schedule – include them in Account Total on Schedule

(A)

Number of Shares

(B)

Name of Stock

(C)

Registered Names

fadditiasaceisrequiredattachridersfthesasize frybererduced

Document Specifications

| Fact Name | Description |

|---|---|

| Form Title | New Jersey Estate Tax Return Form IT-Estate 2017 |

| Governing Law | R.S. 54:38.3 guides the refund process for overpayments. |

| Eligibility Date for Decedents | Applies to resident decedents who passed away after a specified date and before January 1, 2018. |

| Related Documents | Must include Federal form 706, Last Will and Testament, any trust agreements, and Schedule M question 2(c) to avoid delays. |

| Waiver Request Schedules | Complete Schedules E-4 to E-7 to request necessary waivers for New Jersey assets. |

| Special Handling Notes | Do not use binders or staples. It's recommended to use rubber bands or clips for organization. |

| Filing and Payment Guidance | Instructions for mailing addresses, payment checks, and ensuring documents like the will are included and properly ordered. |

| Interest and Payment Deadline | Interest accrues from the date of death until payment. Payments are first applied to any accrued interest. |

Detailed Steps for Using New Jersey Estate Tax Return

Dealing with the loss of a loved one brings a multitude of responsibilities, among which is navigating the nuances of estate tax filings. If you find yourself in the position of handling a loved one’s estate in New Jersey, you’ll need to familiarize yourself with filling out the New Jersey Estate Tax Return form. This step-by-step guide will walk you through the essential steps of completing the form correctly, ensuring that all necessary details are accurately reported and helping to streamline the process for you.

- Begin by accurately filling out the decedent’s name (last, first, middle) and Social Security Number in the designated sections at the top of the form.

- Enter the decedent’s date of death (month, day, year), and the county of residence at the time of death.

- Specify whether the decedent died testate (with a will) or intestate (without a will).

- Fill out the mailing address section with the name, daytime phone number, and full address of the person or firm authorized to receive all communications. This is essential for ensuring proper handling and response to any correspondence from the Division of Taxation.

- Carefully enter the information regarding the decedent’s estate in sections a through e, following the provided instructions for calculating the taxable estate and tentative tax.

- For section 3b, make sure to enter the amount of any estate, inheritance, legacy, or succession taxes paid to other states, excluding New Jersey. This is critical for accurately computing the state death tax deduction.

- Review the calculations on the form to determine the Net New Jersey Estate Tax due, interest, and penalty if applicable, and the total amount due.

- Include a completed Federal form 706, even if not required by the IRS. This includes all schedules and supporting documents filed or would have been filed with the IRS.

- Attach a complete, legible copy of the decedent’s Last Will and Testament and any codicils thereto. If the decedent was party to any trust agreements, include complete copies of these documents as well.

- Ensure that any requests for a refund of an overpayment are made in writing within the statutory three-year period as outlined in R.S. 54:38.3.

- Sign the form and have it notarized. The representative's printed name, official title, address, and date should be clearly indicated. This authentication step is crucial for the validity of the return.

- Adhere to the return processing instructions to avoid any delays. This includes avoiding the use of binders, sealed folders, or extra-long staples. Make sure any payments are stapled to the completed payment voucher and placed on top, with checks made payable to “New Jersey Inheritance and Estate Tax” including the decedent’s name and SS#. Confirm that the mailing address is correct and designates the appropriate recipient for all correspondence.

- Finally, file the completed return. If also filing an Inheritance Tax return, include this in the same envelope or box but keep the two returns separate. Remember to include separate checks and vouchers for each tax.

Following these steps will help ensure the New Jersey Estate Tax Return form is filled out accurately and completely, aiding in the smooth handling of the decedent's estate. Remember to double-check all entries and attachments before submission to avoid common filing errors and potential delays.

Learn More on New Jersey Estate Tax Return

FAQs about the New Jersey Estate Tax Return Form (IT-Estate 2017)

Who needs to file the New Jersey Estate Tax Return (IT-Estate 2017)?

The New Jersey Estate Tax Return is required for the estates of individuals who were residents of New Jersey at the time of death, and whose date of death falls within a specific window and their gross estate exceeds a certain value. Specifically, if an individual passed away after December 31, 2016, but before January 1, 2018, and their gross estate, plus adjusted taxable gifts and specific exemptions, exceeds the threshold of $2,000,000, then the estate is required to file. It is important to include a complete Federal Form 706, even if not mandated by the IRS, alongside any will, trust documents, and a notarized signature from the estate's representative.

What documents are required when filing the IT-Estate 2017?

When filing IT-Estate 2017, you are required to submit a variety of documents to ensure a complete and accurate representation of the decedent's estate. These include:

- A complete, legible copy of the decedent's Last Will and Testament, including all codicils.

- Any trust agreements to which the decedent was a party.

- The Federal Form 706 for the estate, even if you are not required to file it with the IRS.

- The completed estate tax return forms and any applicable schedules.

Ensuring all the necessary documents are submitted can prevent delays in processing the estate tax return.

How can I avoid delays in having the New Jersey Estate Tax Return processed?

To prevent delays in processing the New Jersey Estate Tax Return, follow these key guidelines:

- Avoid enclosing returns in binders, sealed folders, or notebooks. Use rubber bands or clips instead.

- Do not use staples, especially extra-long ones, on the return. If needed, two-hole ATCO fasteners along the top of the return are acceptable.

- Do not include duplicate copies of the return or any attached documents. When filing both Inheritance and Estate Tax returns, ensure only one copy of each requisite document is included.

- Staple checks to the completed payment voucher, placing the voucher on top, and ensure the decedent's name and SSN are on the check.

- Verify all personal information, such as the decedent's social security number and date of death, is accurate.

Adhering to these guidelines will streamline the process, making it smoother and quicker.

What happens if an overpayment is made on the New Jersey Estate Tax?

In instances of overpayment on the New Jersey Estate Tax, the estate or the representative can request a refund. However, to be considered for a refund, the request must be made in writing within three years of payment, in accordance with New Jersey tax laws. It's important to detail the reason for the overpayment and the exact amount you believe should be refunded. The Division of Taxation will review the request and, if approved, will process the refund in the due course of business.

Common mistakes

Failing to include a complete, legible copy of the decedent's Last Will and Testament and any codicils thereto. This oversight can delay the processing of the estate tax return and affect the distribution of the estate.

Omitting a complete, legible copy of any trust agreements to which the decedent was a party. Trusts can significantly impact the estate's tax burden, and neglecting to submit these documents can lead to inaccuracies.

Not including a completed Federal Form 706, even when not required to file with the IRS. The information from this form is crucial for accurately determining the estate’s tax obligations to New Jersey.

Incorrectly calculating the taxable estate. This mistake can result from misunderstanding which assets are to be included or improperly valued, affecting the estate's tax liability.

Forgetting to claim deductions for estate or inheritance taxes paid to other states, if applicable. This can result in the overpayment of taxes to New Jersey.

Entering incorrect information on Schedule M, especially failing to answer question 2(c), leading to processing delays. Accurate completion is essential for efficient processing.

Failure to apply for waivers for New Jersey assets using Schedules E-4 through E-7. Not requesting necessary waivers can restrict access to these assets for the beneficiaries.

Missing the payment of interest and penalties due, calculated from the date of the decedent’s death. This oversight can increase the estate’s financial burden due to accruing interest.

Incorrect mailing address or recipient for correspondence. This can result in critical communications from the Division of Taxation being sent to the wrong address or individual.

Avoiding these mistakes ensures the estate tax return process goes smoothly, helping beneficiaries to receive their inheritance without unnecessary delays or financial burdens.

Documents used along the form

When preparing to file a New Jersey Estate Tax Return, several additional documents often accompany the submission to ensure compliance and thoroughness. These documents serve as integral components of the estate tax submission process, providing crucial details and substantiation for the information included in the estate tax return. The understanding of these forms and their purpose can greatly assist in navigating the complexities of estate planning and taxation.

- Federal Form 706: This is a United States Estate (and Generation-Skipping Transfer) Tax Return, which is required for the estate of a decedent who was a U.S. citizen or resident at the time of death. It details the decedent's gross estate under the terms of the Internal Revenue Code (IRC).

- Last Will and Testament and All Codicils: The decedent's will, along with any codicils, amendments made to the will before the decedent's death, are crucial. These documents outline the decedent’s final wishes regarding the distribution of their estate and appoint an executor.

- Trust Agreements: These include any agreements related to trusts the decedent was part of. Trust documents provide details about the management and distribution of assets held in trust, which could affect the estate's taxable assets.

- Waiver Request Schedules (Schedules E-4 thru E-7): These schedules are necessary when requesting waivers for certain New Jersey assets within the estate. They help to identify assets that require waivers before they can be transferred to heirs or beneficiaries.

- Documentation for Federal Estate Tax purposes: Any documents that were submitted to the IRS in support of the Federal Estate Tax Return, including appraisals, account statements, and other records, must also be included. These documents support the values and claims made on the estate tax return.

Together, these documents form a comprehensive packet that supports the New Jersey Estate Tax Return, ensuring all aspects of the decedent's estate are accurately presented and accounted for. Properly assembling and submitting these forms not only complies with legal requirements but also facilitates a smoother process for the estate’s executor and beneficiaries, potentially minimizing taxes and maximizing the estate’s value passed on to the heirs. Understanding the importance and function of each can significantly ease the burden of estate settlement.

Similar forms

One document similar to the New Jersey Estate Tax Return form is the Federal Estate Tax Return (IRS Form 706). This form is required for reporting the decedent’s entire gross estate, determining the estate's tax liability to the federal government, and identifying assets for the IRS. It's akin to the New Jersey Estate Tax Return because both demand detailed listings of the decedent's assets and both calculate taxes based on the value of those assets. However, the federal form is broader, covering federal tax liabilities, while the New Jersey form focuses on state-specific tax responsibilities.

Another analogous document is the Last Will and Testament, which outlines the decedent’s final wishes regarding the distribution of their assets and the appointment of an executor to manage their estate. While the Last Will and Testament itself does not calculate taxes, the New Jersey Estate Tax Return requires a complete and legible copy of it (and any codicils) because it directly impacts the estate's asset distribution, which in turn affects tax calculations.

The Trust Agreement document is also comparable. Trust agreements detail how assets placed into trust should be handled both during the decedent's life and after their death. Since the New Jersey Estate Tax Return requires copies of any trust agreements to which the decedent was a party, it underscores the influence these documents have on estate valuation and corresponding tax obligations, similar to the Last Will and Testament.

Applications for Refund of an Overpayment share similarities with the New Jersey Estate Tax Return in that they involve written requests for money to be returned under specific circumstances. For the Estate Tax Return, requests for refunds due to overpayment must be made within a statutory period, highlighting a procedural intersection where careful reporting and timely requests can lead to adjustments in the estate’s financial dealings with state tax authorities.

The IRS Request for Transcript of Tax Return Form (Form 4506-T) can echo the requirements of the New Jersey Estate Tax Return, especially concerning validation processes. Completing the Estate Tax Return may necessitate obtaining federal tax information to ensure consistent reporting across both state and federal levels, reflecting the interconnectedness of different jurisdictions’ tax documentation and the thoroughness required in estate settlement.

A Waiver Request, particularly for real and personal property within New Jersey, resembles the Estate Tax Return in terms of providing necessary documentation for asset transfers. The return may necessitate waivers for certain New Jersey assets to be successfully transferred to heirs or beneficiaries, ensuring that all tax obligations are satisfied before the distribution of the decedent's estate.

Finally, a State Death Tax Deduction Form for Other States reveals a procedural and informational similarity to the New Jersey document, as it pertains to understanding and documenting taxes paid to other states. The New Jersey Estate Tax Return form includes considerations for taxes paid to other jurisdictions, which can affect the estate’s tax liability within New Jersey, illustrating the broad scope of estate taxation beyond a single state's boundaries.

Dos and Don'ts

When preparing to file the New Jersey Estate Tax Return, there are several crucial steps to follow to ensure the process is completed accurately and effectively. Being mindful of these instructions can help avoid common mistakes that may result in processing delays or incorrect assessments of tax liability. Below are guidelines on what should and shouldn't be done:

Do:

Ensure to include a completed Federal Form 706 even if not required by the IRS, including all schedules and supporting documents, to provide comprehensive information about the deceased's estate.

Attach a complete, legible copy of the decedent’s Last Will and Testament along with any codicils and any trust agreements the decedent was a part of, ensuring that the estate's planning documents are fully accounted for in the tax calculation.

Verify the decedent’s Social Security Number and date of death on the return to avoid any confusion or misidentification.

Ensure that the return is signed and notarized by the estate’s legal representative to validate the authenticity of the information provided.

Accurately complete the Mailing Address section with the information of the individual authorized to receive all correspondence from the Division of Taxation, facilitating effective communication.

File any necessary Waiver Request Schedules (E-4 through E-7), only listing assets that require waivers, to properly request the release of New Jersey assets held by the decedent.

Don't:

Bind the return in any form of binder, sealed folder, or notebook which can hinder the processing of the document.

Use staples, especially extra-long ones, as this can cause damage to the documents; it is recommended to use rubber bands or clips instead.

Submit duplicate copies of the return or any attachments unless specifically required as this can cause confusion and delay in processing.

Forget to staple checks to the completed payment voucher and ensure that the voucher is placed on top for visibility; checks should be made payable to “New Jersey Inheritance and Estate Tax” with the decedent’s name and SSN included.

Overlook checking and ensuring the return is accurate and complete before submission, including verifying all schedules and documentation are included.

Fail to clearly mark the return as “Amended” at the bottom if filing an amendment to previously submitted information, to ensure that the amendment is processed correctly.

Following these guidelines carefully will help ensure that the New Jersey Estate Tax Return is filed correctly and efficiently processed, reducing the risk of delays or errors.

Misconceptions

Misconceptions about the New Jersey Estate Tax Return form can lead to confusion for those navigating the process of estate planning or handling the affairs of a loved one who has passed away. Here are seven common misunderstandings:

- The belief that the New Jersey Estate Tax Return form is only required if the decedent had assets in New Jersey. In reality, the form is necessary for all resident decedents whose gross estate exceeds the threshold amount established by New Jersey law, regardless of where the assets are located.

- Many assume they do not need to include a complete copy of the decedent's Last Will and Testament and any codicils thereto, as well as trust agreements. This information is essential for a full understanding of the decedent's estate and must be provided.

- There is a misconception that if an estate is not required to file a federal estate tax return, then a New Jersey Estate Tax Return is not needed. However, a New Jersey Estate Tax Return must be filed based on the specific criteria set by the state, which can differ from federal requirements.

- Another misunderstanding is regarding overpayment. Some believe that overpayments are automatically refunded without action. The truth is, requests for the refund of an overpayment must be made in writing within the three-year statutory period.

- Some people think payments on account or refund requests should only include the amount paid with the return. It is crucial to understand that any payment made prior to the formal assessment should also account for any further accrual of interest until the amount paid fully satisfies the tax due.

- A common mistake is underestimating the importance of accurately completing all required documents and schedules. Each section of the return, including the waiver requests for New Jersey assets, plays a vital role in the accurate assessment of estate taxes.

- Finally, many overlook the detailed instructions provided for the return, leading to delays in processing. For instance, not using staples and enclosing returns in the specified manner are practical tips to prevent processing delays.

Addressing these misconceptions and following the guidelines as outlined can help streamline the process of filing the New Jersey Estate Tax Return, ensuring compliance and the timely resolution of the estate's tax obligations.

Key takeaways

Filling out and using the New Jersey Estate Tax Return form, specifically for those who had a decedent with a date of death on or after January 1, 2017, requires attention to detail and understanding of several key points to ensure compliance and accuracy. Below are six essential takeaways for navigating this form:

- Always include a completed Federal Form 706 alongside the New Jersey Estate Tax Return when the decedent's date of death is on or after January 1, 2017, even if filing with the IRS is not compulsory. This fosters a uniform assessment of the estate across federal and state levels.

- Financial documents, such as the decedent's Last Will and Testament, any codicils, and any relevant trust agreements, must be submitted in a legible format. These documents provide critical information that affects tax calculations and return processing.

- Requests for refunds of any overpayment beyond what is outlined on line 13 of the return must be submitted in writing within a three-year period as dictated by R.S. 54:38.3. This stringent timeline underlines the importance of timely and accurate filing.

- Clarification of assets requiring waivers through Schedules E-4 to E-7 is mandatory. These schedules explicitly ask for information on New Jersey assets for which waivers are sought, underscoring the state's interest in local property and its transfer post-death.

- Interest accrual on unpaid New Jersey Estate Tax begins from the decedent's date of death, emphasizing the need for prompt payment to avoid additional charges. Extensions provided for filing the federal estate tax return may influence the interest calculated, offering some flexibility in certain circumstances.

- Adherence to specific submission instructions, such as avoiding the use of binders or extra-long staples and properly signing and notarizing the return, is crucial. These guidelines aim to streamline the processing of returns, waivers, and refund requests, minimizing delays.

Compliance with these key points helps ensure that the estate's financial affairs are settled correctly and efficiently, reflecting the decedent's wishes and legal requirements. Careful preparation and understanding of the New Jersey Estate Tax Return can significantly ease the administrative burden on the estate's executor or administrator.

Popular PDF Documents

New Jersey Tax Id Number - For changes in remittance addresses or to establish a new vendor, this form serves as your key document.

Nj Tax Forms 2023 - For those wary of e-filing's security or accuracy, the NJ-1040-O form offers a reassuring alternative.