Fill Out a Valid New Jersey Ppt 6 B Template

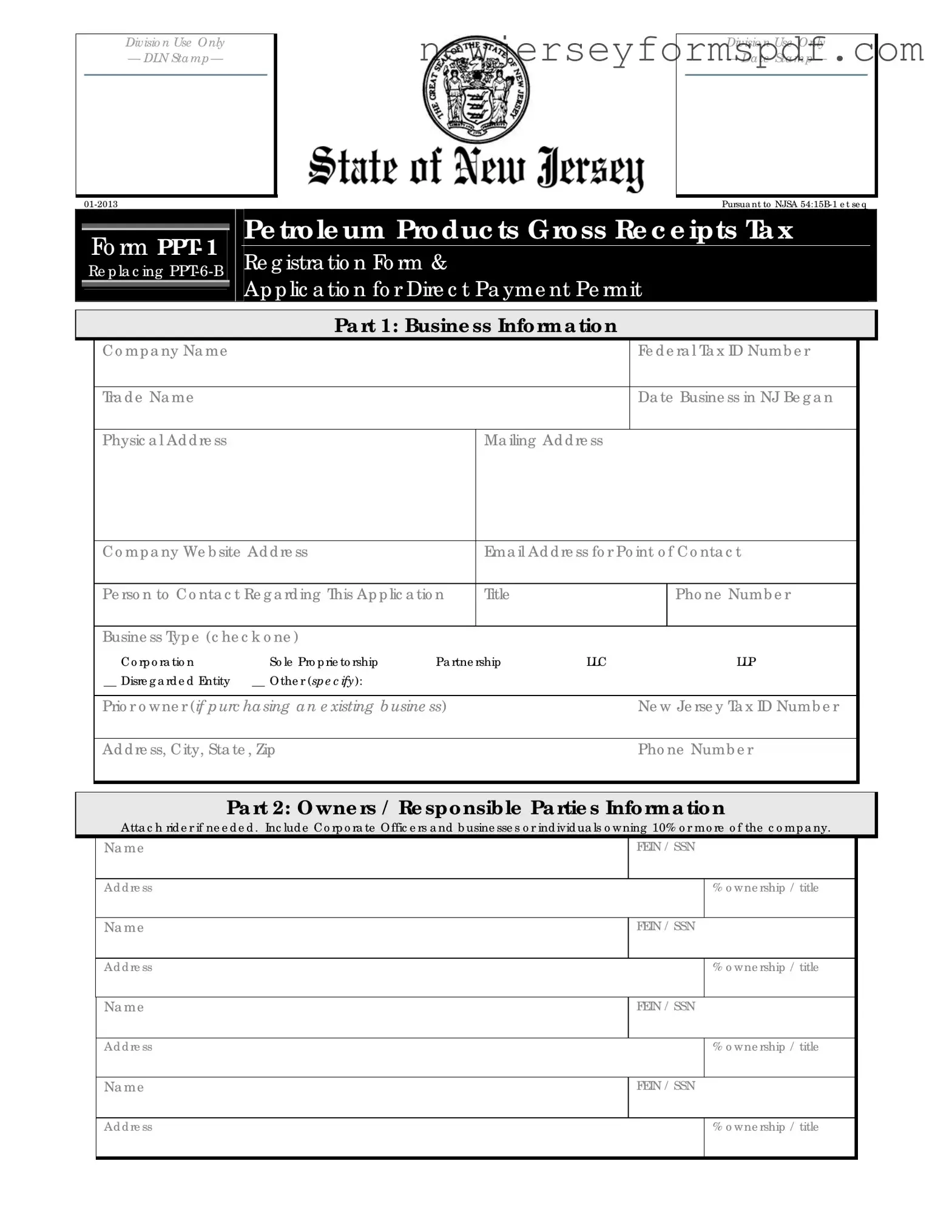

In New Jersey, businesses dealing with petroleum products face a unique set of tax obligations under the NJSA 54:15B-1 et seq, which is why the PPT-6-B form, or the Application for Direct Payment Permit, plays a crucial role. This form allows businesses to purchase petroleum products without being charged the tax upfront; instead, they pay the tax directly to the state for any sale or use of a petroleum product. Designed to streamline the tax reporting and payment process, particularly for entities with a significant proportion of exempt customers or those likely to encounter multiple taxation on the same product, the PPT-6-B is issued by the Division of Taxation. However, the division exercises caution, ensuring that issuing a Direct Payment Permit doesn't burden the ultimate consumers with higher taxes or grant the permit when the applicant has alternative means to mitigate adverse tax consequences. With sections covering business information, ownership and responsible parties, business activities, and a specific application for the permit itself, the form demands detailed disclosures to ensure compliance and integrity. Affirmation of the correctness and completeness of the information provided is required to avoid application denial or permit revocation. Importantly, the New Jersey Division of Taxation provides clear guidelines for application, emphasizing that there are no fees involved, but a commitment to accuracy and transparency is imperative for successful registration and permit acquisition.

Sample - New Jersey Ppt 6 B Form

Divisio n Use O nly

— DLN Sta mp —

Divisio n Use O nly

— Da te Sta mp —

|

|

|

|

|

|

|

Pe tro le um Pro duc ts G ro ss Re c e ipts Ta x |

||||||

|

|

Fo rm PPT- 1 |

|

|

|||||||||

|

|

|

|

|

Re g istra tio n Fo rm & |

|

|

|

|

|

|||

|

|

Re p la c ing |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

Ap p lic a tio n fo r Dire c t Pa yme nt Pe rmit |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

Pa rt 1: Busine ss Info rm a tio n |

|

|

|

|||

|

|

|

C o mp a ny Na me |

|

|

|

|

|

Fe d e ra l Ta x ID Numb e r |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

Tra d e Na me |

|

|

|

|

|

Da te Busine ss in NJ Be g a n |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

Physic a l Ad d re ss |

|

|

|

Ma iling Ad d re ss |

|

|

|

|||

|

|

|

|

|

|

|

|

||||||

|

|

|

C o mp a ny We b site Ad d re ss |

|

Ema il Ad d re ss fo r Po int o f C o nta c t |

|

|||||||

|

|

|

|

|

|

|

|

|

|||||

|

|

|

Pe rso n to C o nta c t Re g a rd ing This Ap p lic a tio n |

Title |

|

|

Pho ne Numb e r |

|

|||||

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

Busine ss Typ e (c he c k o ne ) |

|

|

|

|

|

|

||||

|

|

|

C o rp o ra tio n |

|

So le Pro p rie to rship |

Pa rtne rship |

LLC |

|

LLP |

|

|||

|

|

|

Disre g a rd e d Entity |

|

O the r (sp e c ify): |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||||||

|

|

|

Prio r o wne r (if p urc ha sing a n e xisting b usine ss) |

|

|

Ne w Je rse y Ta x ID Numb e r |

|

||||||

|

|

|

|

|

|

|

|

|

|||||

|

|

|

Ad d re ss, C ity, Sta te , Zip |

|

|

|

Pho ne Numb e r |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Pa rt 2: O wne rs / Re spo nsib le Pa rtie s Info rm a tio n

|

Atta c h rid e r if ne e d e d . |

Inc lud e C o rp o ra te O ffic e rs a nd b usine sse s o r ind ivid ua ls o wning 10% o r mo re o f the c o mp a ny. |

||

|

Na me |

|

FEIN / SSN |

|

|

|

|

|

|

Ad d re ss

% o wne rship / title

Na me

FEIN / SSN

Ad d re ss

% o wne rship / title

Na me

FEIN / SSN

Ad d re ss

% o wne rship / title

Na me

FEIN / SSN

Ad d re ss

% o wne rship / title

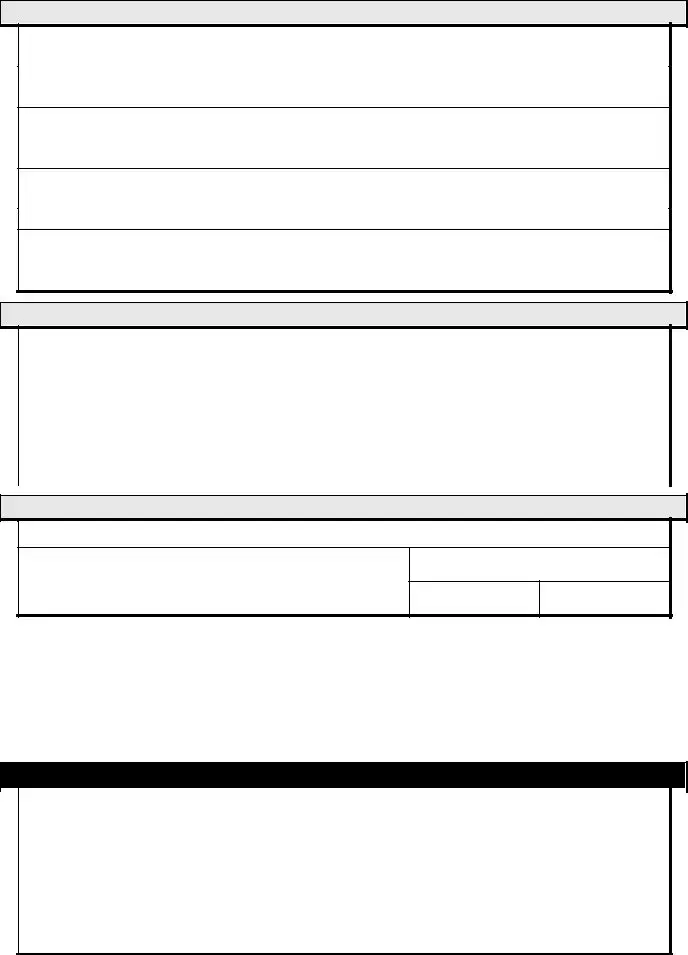

Pa rt 3: Busine ss Ac tivitie s

De sc rib e yo ur b usine ss mo d e l a nd re g ula r a c tivitie s

List yo ur inte nd e d sup p lie rs

List yo ur inte nd e d c usto me rs

List the p ro d uc ts yo u inte nd to se ll

Pa rt 4: Applic a tio n fo r Dire c t Pa ym e nt Pe rm it

Ho ld ing a Dire c t Pa ym e nt Pe rmit e ntitle s the ho ld e r to p urc ha se p e tro le um p ro d uc ts witho ut b e ing c ha rg e d the ta x. The Dire c t Pa yme nt Pe rmit ho ld e r will p a y the ta x d ue d ire c tly to the sta te fo r a ny sa le o r use o f a p e tro le um p ro d uc t.

|

The |

Divisio n o f Ta xa tio n issue s Dire c t p a yme nt Pe rmits to |

e ntitie s who will ha ve a size a b le p ro p o rtio n o f e xe mp t |

|||||||

c usto me rs o r who will fre q ue ntly e nc o unte r situa tio ns in whic h the ta x will b e c o lle c te d mo re tha n o nc e . |

|

|

||||||||

|

The |

Divisio n o f Ta xa tio n ma y no t issue a Dire c t Pa ym e nt Pe rmit if d o ing so will inc re a se the |

ta x b urd e n to |

the |

||||||

ultima te c o nsume r o r if the a p p lic a nt ha s o the r me a ns to a vo id ne g a tive ta x c o nse q ue nc e s. |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This b usine ss re q ue sts a Dire c t Pa ym e nt Pe rm it. |

|

|

|

This b usine ss o nly |

ne e ds |

to re g iste r fo r |

the |

|

|

|

|

|

||||||

|

|

|

|

|

|

Pe tro le um Pro duc ts |

G ro ss |

Re c e ipts Ta x. |

No |

|

|

|

|

|

|

|

|

Dire c t Pa ym e nt Pe rm it is re q ue ste d a t this tim e . |

|||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

Pa rt 5: Affirm a tio n

The sig na to ry a ffirms tha t a ll info rma tio n c o nta ine d in this re g istra tio n a nd a ny a tta c he d d o c ume nts is c o mp le te a nd true . Any inc o mp le te o r inc o rre c t info rma tio n c a n re sult in d e nia l o f this a p p lic a tio n o r re vo c a tio n o f the p e rmit.

Sig na ture o f o wne r o r a utho rize d o ffic e r |

Printe d Na m e |

Title

Da te

Se nd this c o mp le te d re g istra tio n/ a p p lic a tio n to :

Exc ise Ta x Bra nc h

Divisio n o f Ta xa tio n

PO Bo x 189

Tre nto n, NJ 08695- 0189

Ema il it to :

fue l.ta x@ tre a s.sta te .nj.us

THERE IS N O FEE FO R THIS A PPLIC A TIO N .

Sho uld yo u ha ve a ny q ue stio ns re g a rd ing this re g istra tio n/ a p p lic a tio n, p le a se c a ll the Exc ise Ta x Bra nc h a t (609)

Divisio n Use O nly – De te rm ina tio n

|

|

|

The a p p lic a nt is re g iste re d fo r the PPG RTa s o f |

Inve stig a tio n sta rt d a te : |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

The a p p lic a nt re c e ive d a DPP e ffe c tive o n |

Inve stig a tio n e nd d a te : |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

The a p p lic a tio n fo r DPP wa s d e nie d . |

Inve stig a te d b y: |

|

|

|

|

|

||

|

|

|

|

|

|

Inve stig a to r’ s sta te me nts:

Document Specifications

| Fact Name | Description |

| Form Purpose | The New Jersey PPT-6-B form is used to apply for a Direct Payment Permit for purchasing petroleum products without being charged the tax upfront. |

| Governing Law | This form is pursuant to NJSA 54:15B-1 et seq., relating to the Petroleum Products Gross Receipts Tax. |

| Form Sections | It includes sections for business information, owner/responsible parties information, business activities, application for direct payment permit, and affirmation. |

| Business Information Required | Applicants need to provide company name, tax ID, physical and mailing address, contact details, business type, and information about the ownership. |

| Owner/Responsible Parties Information | Details of corporate officers and individuals or businesses owning 10% or more of the company must be included. |

| Business Activities | Applicants must describe their business model, list intended suppliers and customers, and detail the products intended to be sold. |

| Direct Payment Permit Benefits | Holding a Direct Payment Permit allows the holder to purchase petroleum products without the immediate tax charge, with the tax due paid directly to the state later. |

| Permit Issuance Criteria | The Division of Taxation may issue a Direct Payment Permit if it benefits entities with a sizable portion of exempt customers or frequent tax collection duplications, without increasing the tax burden on the ultimate consumer. |

| Affirmation | The signatory affirms all information provided is complete and true, acknowledging that incorrect information can result in application denial or permit revocation. |

| Application Submission | The completed registration/application can be sent to the Excise Tax Branch of the Division of Taxation via mail or email. There is no fee for this application. |

| Contact Information | If applicants have questions, they can contact the Excise Tax Branch at a provided phone number. |

Detailed Steps for Using New Jersey Ppt 6 B

Filling out the New Jersey PPT-6-B form is crucial for entities looking to obtain a Direct Payment Permit for petroleum products. This document enables businesses to navigate the financial aspect of their operations more efficiently by allowing them to purchase petroleum products without being immediately charged the tax, which they will later pay directly to the state. The aim is to avoid any undue tax burden on the consumers and to simplify tax collection for businesses that qualify for this permit. To ensure that your application is processed smoothly, follow these step-by-step instructions carefully.

- Begin by entering the Business Information required in Part 1:

- Enter your Company Name.

- Fill in your Federal Tax ID Number.

- List the Trade Name, if applicable.

- Specify the Date Business in NJ Began.

- Provide the Physical Address and a separate Mailing Address if it's different.

- Include your Company Website Address and Email Address for the Point of Contact.

- Detail the Person to Contact Regarding This Application, including their title and phone number.

- Check the box that best describes your Business Type.

- If purchasing an existing business, include the Prior owner's New Jersey Tax ID Number, address, city, state, zip, and phone number.

- Proceed to Part 2: Owners/Responsible Parties Information.

- Attach a rider if more space is needed for information.

- Include names, FEIN/SSNs, addresses, and percentage of ownership/title for corporate officers and individuals or businesses owning 10% or more of the company.

- Move to Part 3: Business Activities.

- Describe your business model and regular activities.

- List your intended suppliers and customers.

- Identify the products you intend to sell.

- In Part 4: Application for Direct Payment Permit, choose the appropriate option for your business:

- If applying for a Direct Payment Permit, check the corresponding box.

- If you only need to register for the Petroleum Products Gross Receipts Tax without requesting a Direct Payment Permit at this time, check the relevant box.

- Complete Part 5: Affirmation.

- The owner or authorized officer must sign and print their name, title, and date, affirming the completeness and truthfulness of the information provided.

- Finally, send the completed registration/application form to the Excise Tax Branch Division of Taxation either by mail to PO Box 189, Trenton, NJ 08695-0189 or by email to fuel.tax@treas.state.nj.us. Remember, there is no fee for this application.

After your application is submitted, it will be processed and reviewed by the Division of Taxation. Keep an eye on your contact information for any communication from the Excise Tax Branch regarding the status of your application. Whether you're aiming for a smooth transition into New Jersey's business environment or looking to streamline your tax responsibilities, following these instructions carefully will set you on the right path.

Learn More on New Jersey Ppt 6 B

What is the New Jersey PPT 6 B form?

The New Jersey PPT 6 B form is an application required for businesses seeking a Direct Payment Permit for purchasing petroleum products without being immediately charged the Petroleum Products Gross Receipts Tax. By holding this permit, the tax due is paid directly to the state by the permit holder rather than at the point of sale. This application becomes pertinent for entities that have a sizeable proportion of exempt customers or frequently deal in transactions where the tax would be collected more than once, leading to unnecessary complications or financial burdens.

Who needs to fill out the New Jersey PPT 6 B form?

Businesses that intend to purchase petroleum products in New Jersey without being charged the tax at the time of purchase need to fill out this form. These are typically companies that either sell to a significant number of exempt customers or could end up paying the tax multiple times through their chain of transactions. This includes, but is not limited to, large distributors, certain retailers, and other entities engaged in the petroleum products industry within New Jersey.

What information is required on the PPT 6 B form?

- Part 1: Business Information - Includes the company name, Federal Tax ID Number, trade name, the date business operations started in New Jersey, physical and mailing addresses, company website, and the email address and phone number for the contact person.

- Part 2: Owners/Responsible Parties Information - Details about corporate officers and anyone owning 10% or more of the company must be provided.

- Part 3: Business Activities - A description of the business model, regular activities, intended suppliers and customers, and a list of the products intending to be sold.

- Part 4: Application for Direct Payment Permit - This section is where the business states its request for the Direct Payment Permit, highlighting its eligibility and need.

- Part 5: Affirmation - The applicant must affirm that all information provided in the application and any attached documents is complete and true.

Is there a fee for applying for a Direct Payment Permit in New Jersey?

No, there is no fee associated with the application for a Direct Payment Permit in New Jersey. The state encourages eligible businesses to apply if they meet the criteria, aiding in simplifying the tax collection process both for the entities and the state.

Where should the completed PPT 6 B form be sent?

Once completed, the PPT 6 B form can be sent to the Excise Tax Branch of the Division of Taxation. Businesses have the option to mail the form to PO Box 189, Trenton, NJ 08695-0189. Alternatively, the form can be emailed to fuel.tax@treas.state.nj.us. Applicants should also note the contact number (609) 633-9057 for any questions related to the registration/application process.

Common mistakes

When filling out the New Jersey PPT-6-B form for a Direct Payment Permit, individuals often encounter various pitfalls that can lead to significant delays, rejections, or future compliance issues. Recognizing and avoiding these mistakes is crucial for a smooth application process. Here is an expanded list of common errors:

Not providing complete Business Information, including the physical and mailing address, company website, and the email address for the point of contact. This comprehensive detail is essential for the Division of Taxation's records and future communications.

Failure to accurately list Owners/Responsible Parties with a 10% or greater ownership. Applicants sometimes omit essential details such as FEIN/SSN, address, and their percentage of ownership/title, which are critical for identifying all responsible parties.

Incorrectly describing Business Activities, including the business model and regular activities. A detailed and accurate description helps the Division understand the business's operation and its eligibility for a Direct Payment Permit.

Not specifying Intended Suppliers and Customers and the products the business intends to sell. This information is crucial for assessing the application's merit and the applicant's need for the permit.

Selecting the wrong Application Type in Part 4. Applicants must clearly indicate whether they are applying for the Direct Payment Permit or only registering for the Petroleum Products Gross Receipts Tax, as this affects the application's processing.

Failure to properly complete the Affirmation section by the owner or authorized officer, including ensuring that the signature, printed name, title, and date are correctly filled out. This affirmation verifies that all information provided is complete and true, and any inaccuracies can result in denial or revocation of the permit.

Avoiding these common mistakes requires attention to detail and a thorough understanding of the application requirements. Ensuring all information is complete, accurate, and well-documented facilitates a smoother application process and helps avoid unnecessary delays or complications.

Documents used along the form

When handling the New Jersey PPT-6B form, which is essential for businesses dealing in petroleum products looking to manage their Gross Receipts Tax in a streamlined manner, there are several other forms and documents often needed to ensure compliance and efficiency. These documents play a pivotal role in supporting the application for a Direct Payment Permit and maintaining accurate records for tax purposes. Let’s take a look at a few:

- Business Registration Certificate (BRC): Essential for every business operating within New Jersey, the BRC proves that your business is registered to legally operate in the state. This certificate is often required when filing for any form of state tax.

- Form NJ-REG: This form needs to be completed to register a business for tax and employer purposes in New Jersey. It’s a critical step in ensuring your business is in the database for state taxes, including petroleum products gross receipts tax.

- Certificate of Authority: Required for collecting sales tax or purchasing tax-free items intended for resale, this document is crucial for businesses that sell petroleum products which may also be subject to sales tax.

- Annual Report: Filed with the New Jersey Department of Treasury, the Annual Report is essential for keeping your business in good standing. It updates or confirms the vital details about your company’s operational status and ownership.

- Form NJ-927: This form is used to report and pay unemployment, disability, workforce development, and family leave insurance contributions if you have employees in New Jersey. Even though it's not directly related to petroleum tax, it’s important for overall compliance.

- Form C-9600: Required to make a claim for a refund of Gross (Sales) Tax paid in error on purchases made by a business. If your business mistakenly pays tax on a purchase exempted by the Direct Payment Permit, this form would be necessary.

- Letter of Good Standing: While not a form, acquiring a Letter of Good Standing from the Division of Revenue can be beneficial, especially when expanding business operations or applying for loans. It certifies that your business is compliant with filing and tax requirements.

Accompanying your PPT-6B form with the correct supporting documentation can streamline the application process, ensuring your business meets all regulatory requirements for operating in New Jersey’s petroleum products sector. Adequate preparation and understanding of each document’s role and requirement can save time and protect against compliance issues, simplifying tax and legal processes for business owners in the petroleum industry.

Similar forms

The New Jersey PPT-6-B form, used for applying for a Direct Payment Permit for petroleum products, shares similarities with the Streamlined Sales and Use Tax Agreement (SSUTA) Certificate of Exemption. Both forms enable registered businesses to make tax-exempt purchases—PPT-6-B for petroleum products directly from the state, and the SSUTA Certificate for general sales and use tax across multiple states. Each requires the applicant to affirm that the information provided is accurate and complete, and misuse of either can lead to penalties or the revocation of tax-exempt status.

Similar to the New Jersey PPT-6-B form, the Application for Employer Identification Number (Form SS-4) submitted to the Internal Revenue Service also gathers detailed business information, such as the type of business entity, owner details, and business activities. Although serving different purposes—one for state tax exemption and the other for federal identification—the thoroughness in collecting identifiable business data highlights their importance in ensuring regulatory compliance and accountability.

The New Jersey Division of Revenue's Business Registration Application (NJ-REG) also parallels the PPT-6-B form, as both are necessary steps for businesses to legally operate within New Jersey. While NJ-REG is broader, encompassing various tax and employer obligations on a state level, the PPT-6-B form has a narrow focus on petroleum products tax. Each plays a crucial role in aligning businesses with New Jersey's regulatory environment, emphasizing the state's commitment to fair commerce and tax collection.

The Certificate of Authority Application for Sales Tax (Form CA-1) is akin to the PPT-6-B in that it involves registering with the state for specific tax purposes. While the CA-1 form is for businesses to collect sales tax from customers, the PPT-6-B allows for direct tax payment to the state for petroleum products. Both forms facilitate tax compliance within the business's operational framework, ensuring that necessary taxes are accurately collected and remitted.

The Hazardous Waste Generator's ID Number Application shares a commonality with the PPT-6-B, as both require businesses to provide detailed information about their operations for regulatory purposes. The former is for environmental regulation, ensuring safe hazardous waste handling, while the latter deals with tax regulation of petroleum products. Each application underscores the importance of state oversight in protecting both fiscal and environmental health.

The Alcohol and Tobacco Tax and Trade Bureau's (TTB) Alcohol Dealer Registration form is another related document. Like the PPT-6-B, it's specific to a type of product—alcohol instead of petroleum products—and requires detailed information about the business for compliance purposes. Both forms are integral to monitoring and regulating the distribution of controlled products, ensuring that taxes are properly assessed and collected.

Another similar document is the New Jersey Certificate of Authority for a Foreign Corporation. This document, like the PPT-6-B, necessitates thorough business information for entities seeking to operate within state jurisdiction. The primary difference lies in their purpose: the Certificate of Authority allows foreign corporations to legally do business in New Jersey, while the PPT-6-B relates to tax exemption on petroleum products. Both are critical for ensuring businesses meet New Jersey's legal and regulatory standards.

Finally, the Uniform Commercial Code (UCC-1) Financing Statement bears resemblance in its requirement for detailed business information, despite its primary focus being on securing interests in collateral for financing. Both the UCC-1 and the PPT-6-B form require accurate business identification to protect state and individual interests—whether for commercial financing or tax exemption purposes. Detailing business operations and ownership, they help maintain the integrity of financial and regulatory systems.

Dos and Don'ts

When filling out the New Jersey PPT-6-B form, there are certain practices one should follow to ensure accuracy and compliance. Below are lists of what you should and shouldn't do.

Do:

- Ensure all the information provided is complete and accurate, including business information, owners/responsible parties, and business activities.

- Include a rider if additional space is needed for listing corporate officers or owners with 10% or more ownership.

- Clearly describe your business model, regular activities, intended suppliers, intended customers, and the products you intend to sell in Part 3.

- Check the appropriate box in Part 4 to indicate whether this business is applying for a Direct Payment Permit or only needs to register for the Petroleum Products Gross Receipts Tax.

- Have the owner or authorized officer sign the affirmation in Part 5, affirming that all information contained in the registration/application and any attached documents is complete and true.

Don't:

- Leave any sections incomplete. An incomplete application could result in the denial of the application or revocation of the permit.

- Provide false information. This can also lead to denial of the application or revocation of the permit.

- Forget to check whether you're purchasing an existing business. If so, provide the prior owner's information.

- Ignore the instructions on the application for sending the completed registration/application. It can be sent either by mail to the Excise Tax Branch or by email.

- Assume the process ends with the submission of the form. Keep track of your submission and follow up with the Excise Tax Branch if necessary.

Adhering to these guidelines will streamline the process and help avoid any unnecessary delays or issues with your application. For any questions, direct contact with the Excise Tax Branch is recommended.

Misconceptions

When dealing with the New Jersey Petroleum Products Gross Receipts Tax Form PPT-6B, misconceptions can lead to confusion and potential errors in submission. Here is a clarification of common misunderstandings surrounding this form:

Misconception 1: The form is only for businesses directly involved in petroleum distribution. Clarification: While primarily designed for entities in the petroleum industry, the form can also be pertinent to businesses that have a substantial portion of transactions exempt from taxes or face frequent tax duplications.

Misconception 2: Obtaining a Direct Payment Permit will automatically exempt all petroleum product purchases from taxes. Clarification: The permit allows the holder to defer tax payment until the sale or use of the product, at which time they must report and pay the tax directly to the state.

Misconception 3: There is a fee associated with the application for the Direct Payment Permit. Clarification: There is no fee required to submit this application, enhancing accessibility for all eligible businesses.

Misconception 4: Any business, regardless of size or sales volume, can apply for and receive a Direct Payment Permit. Clarification: The Division of Taxation may restrict issuance to entities that demonstrate a sizeable proportion of exempt transactions or have high potential for tax duplication issues.

Misconception 5: The form requires detailed financial information about the company. Clarification: While comprehensive business information is required, the main focus is on the business model, activities, and tax registration status rather than detailed financial data.

Misconception 6: Submission of the form guarantees approval of the Direct Payment Permit. Clarification: Approval is contingent upon meeting specific criteria set by the Division of Taxation and the submission of complete and accurate information.

Misconception 7: The form is complicated and requires legal assistance to complete. Clarification: The form is designed to be user-friendly, and most businesses should be able to complete it without the need for legal counsel, though consulting with a professional can provide extra assurance.

Misconception 8: Once obtained, a Direct Payment Permit is permanent. Clarification: Permits may be subject to review, renewal, or revocation based on compliance with state regulations and tax laws.

Misconception 9: The form is only for new businesses or those new to the petroleum industry. Clarification: Existing businesses adjusting to changes in the tax law or their business model may also need to submit this form.

Misconception 10: There's no need to update the Division of Taxation after receiving a Direct Payment Permit. Clarification: Permit holders must regularly report their petroleum product transactions and any changes in business status, ensuring compliance with state tax obligations.

Understanding these key aspects can significantly smooth the process of complying with New Jersey's petroleum product taxation guidelines, allowing businesses to focus on their core operations with one less regulatory burden to worry about.

Key takeaways

When considering the application and usage of the New Jersey PPT-6-B form for Direct Payment Permit for Petroleum Products Gross Receipts Tax, several crucial factors must be understood by businesses in New Jersey.

- Preparation and Documentation: It is essential to provide accurate business information, including the company name, Federal Tax ID Number, and the physical and mailing addresses. The form requires detailed information regarding the business model, regular activities, suppliers, customers, and the products being sold. For owners and responsible parties, a comprehensive list including their names, FEIN/SSN, addresses, and ownership percentages/title must be attached if needed. Inaccuracies can result in the denial of the application or revocation of the permit.

- Eligibility for Direct Payment Permit: Holding a Direct Payment Permit allows the holder to purchase petroleum products without being charged the tax upfront. Instead, the tax is paid directly to the state by the permit holder. This arrangement is typically reserved for entities with a significant proportion of exempt customers or who frequently encounter situations where the tax would otherwise be collected multiple times. The Division of Taxation has the discretion to deny issuing a Direct Payment Permit if it believes that doing so would increase the tax burden on the ultimate consumer or if the applicant has other means to avoid negative tax consequences.

- Application Process: To apply for a Direct Payment Permit, entities must affirm that all information contained in the registration and any attached documents is complete and true. The application, along with any necessary documents, should be sent to the Excise Tax Branch of the Division of Taxation via mail or email. There is no fee for this application, which simplifies the process for potential applicants.

- Post-Application: The Division of Taxation will investigate the applicant to verify the information provided and determine eligibility for the Direct Payment Permit. It is essential to monitor the application's status and comply with any further requests for information or clarification from the Division. Being responsive and cooperative during the investigation can facilitate a smoother process.

Understanding these key takeaways can aid businesses in successfully navigating the complexities of the PPT-6-B application process. It ensures compliance with New Jersey's tax regulations regarding the purchase of petroleum products, ultimately allowing for more efficient and cost-effective business operations.

Popular PDF Documents

New Jersey Inheritance Tax - A beneficial resource for legal professionals, tax consultants, and estate administrators navigating New Jersey's estate tax obligations.

Nj Reg - Businesses acquiring assets or employees from another company in New Jersey must detail the transaction on the NJ-REG form.

Nj 927 - The form is structured to help employers easily navigate through reporting requirements.