Fill Out a Valid Nj 1040 Es Template

When dealing with the intricacies of real estate transactions in New Jersey, especially for those who do not reside within the state, the GIT/REP-1 and NJ-1040-ES forms become essential documents. These forms cater to nonresident individuals, estates, or trusts involved in selling property and aim to simplify the taxation process associated with such transactions. The GIT/REP-1 form, serving as a Nonresident Seller’s Tax Declaration, requires sellers to provide detailed information about themselves and the property being sold, including ownership percentage and the total consideration involved in the transaction. It emphasizes the importance of honesty in the declaration, with strict penalties for falsehoods including fines or imprisonment. The NJ-1040-ES portion, on the other hand, is a voucher for declaring estimated taxes due on the gain from the sale, calculated based on New Jersey's highest Gross Income Tax rate of 8.97%. It demands meticulous completion and timely submission at the closing of the sale, stipulating that payment can be made via check or money order but not cash. Crucially, failing to properly fill out and submit these forms can prevent the deed from being recorded, highlighting their importance in the transaction process. In addition, the form navigates through the requirements for representing the seller, with a focus on proper authorization through a Power of Attorney or a direct authorization letter. This comprehensive approach aims to ensure that all parties involved in the real estate transaction are appropriately informed, taxed, and in compliance with New Jersey's laws, showcasing the state’s effort to maintain a transparent and efficient marketplace.

Sample - Nj 1040 Es Form

State of New Jersey

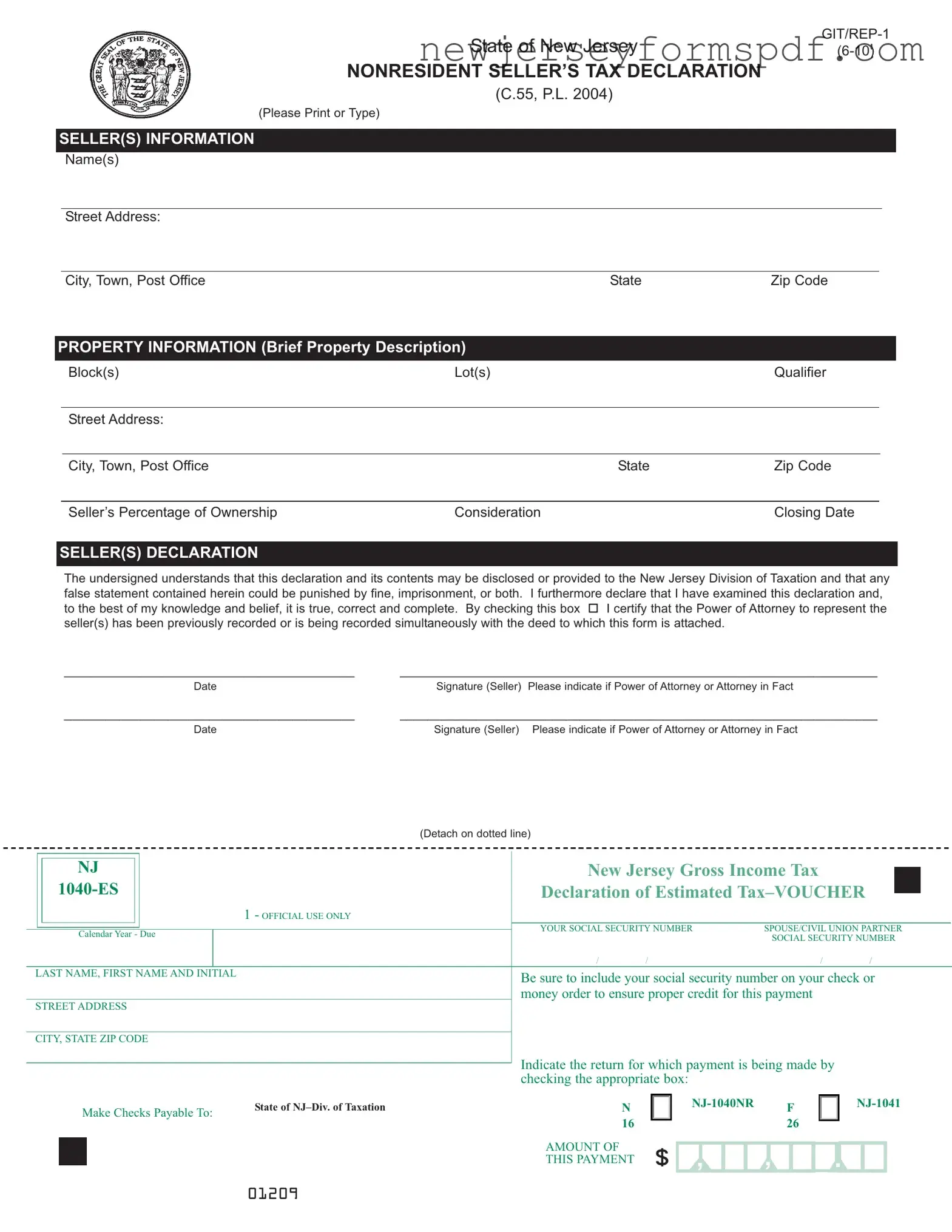

NONRESIDENT SELLER’S TAX DECLARATION

(C.55, P.L. 2004)

(Please Print or Type)

SELLER(S) INFORMATION

Name(s)

Street Address:

City, Town, Post OfficeState Zip Code

PROPERTYINFORMATION (Brief Property Description)

Block(s) |

Lot(s) |

Qualifier |

|

|

|

Street Address: |

|

|

|

|

|

City, Town, Post Office |

State |

Zip Code |

|

|

|

Seller’s Percentage of Ownership |

Consideration |

Closing Date |

SELLER(S) DECLARATION

The undersigned understands that this declaration and its contents may be disclosed or provided to the New Jersey Division of Taxation and that any false statement contained herein could be punished by fine, imprisonment, or both. I furthermore declare that I have examined this declaration and, to the best of my knowledge and belief, it is true, correct and complete. By checking this box I certify that the Power of Attorney to represent the seller(s) has been previously recorded or is being recorded simultaneously with the deed to which this form is attached.

__________________________________________ |

_____________________________________________________________________ |

|

Date |

Signature (Seller) |

Please indicate if Power of Attorney or Attorney in Fact |

__________________________________________ |

_____________________________________________________________________ |

|

Date |

Signature (Seller) |

Please indicate if Power of Attorney or Attorney in Fact |

|

|

|

(Detach on dotted line) |

|

|

|

|

|

|

|

|

|

|

|

|

NJ |

New Jersey Gross IncomeTax |

|

|

|

|

|||

|

Declaration of |

|

||

|

|

|||

|

|

|

|

|

|

1 |

|

|

|

||

|

|

|

|

|

|

|

|

YOUR SOCIALSECURITYNUMBER |

SPOUSE/CIVILUNION PARTNER |

||

|

|

|

|

|

|

||||||

|

|

CalendarYear - Due |

|

|

|

|

|

SOCIALSECURITYNUMBER |

|||

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

/ |

/ |

/ |

/ |

||

LASTNAME, FIRSTNAMEAND INITIAL |

|

|

Besuretoincludeyoursocialsecuritynumberonyourcheckor |

||||||||

|

|

|

|

|

|

|

|

||||

moneyordertoensurepropercreditforthispayment

STREETADDRESS

CITY, STATE ZIPCODE

Indicate the return for which payment is being made by checking the appropriate box:

Make Checks PayableTo: |

State of |

N |

|

|

|

16 |

|

||

|

|

|

|

|

|

|

|

AMOUNTOF |

$ |

|

|

|

||

|

|

|

THIS PAYMENT |

|

F |

|

||

|

26 |

|

|

|

|

|

,

,

,

.

.

01209

Tax Declaration Instructions

This form is only to be completed by nonresident individuals, estates or trusts selling property in New Jersey on or after August 1, 2004.

Name(s): |

Name of seller(s). If more than one owner separate forms must be used except for husband & wife/civil |

|

union couples that file jointly |

Address: |

Seller(s) primary residence or place of business. Do not use the address of the property being sold if a |

|

new residence has been established. |

Property Information: |

Information as listed on deed of property being sold. |

Percentage of Ownership: |

If there is more than one owner list seller's % of ownership. |

Consideration: |

Consideration" means in the case of any deed, the actual amount of money and the monetary value of |

|

any other thing of value constituting the entire compensation paid or to be paid for the transfer of title to |

|

the lands, tenements or other realty, including the remaining amount of any prior mortgage to which the |

|

transfer is subject or which is assumed and agreed to be paid by the grantee and any other lien or |

|

encumbrance not paid, satisfied or removed in connection with the transfer of title. If there is more than |

|

one owner, indicate seller's portion of total consideration received. If the total consideration for the |

|

property is $1,000 or less complete the Seller’s Residency Certification/Exemption form |

|

|

Signature: |

Seller(s) must sign and date the declaration. If the seller's representative is signing the declaration |

|

either (1) a Power of Attorney executed by the seller(s) to the representative must be previously |

|

recorded or recorded simultaneously with the deed to which this form is attached, or (2) a letter signed |

|

by the seller(s) granting authority to the representative to sign this form must be attached.. |

The

Payment in the form of check or money order should be made payable to the State of New Jersey - Division of Taxation. Cash is not acceptable. Tax payment is determined by multiplying the gain on the sale of the property by the highest Gross Income Tax rate of 8.97%. Gain is to be determined without taking into consideration any distributions during the taxable year to beneficiaries by estates or trusts. In no case can the payment be less than 2% of the consideration received.

All information requested on this form must be completed. Failure to complete the form in its entirety will result in the deed not being recorded.

This form and associated payment must be completed at the time of closing and given to the buyer or the buyer's attorney.

The buyer or buyer's attorney must submit the original Sellers Declaration of Tax to the county clerk at the time of recording the deed. Failure to submit the Sellers Declaration of Tax or the Seller's Residency Certification or a Tax Prepayment Receipt will result in the deed not being recorded.

The county clerk will attach the top portion of the form to the deed when recorded. The bottom portion,

Additional information regarding the Gross Income Tax estimated payment requirements on the sale of real estate can be found on the Division of Taxation’s web page at www.state.nj.us/treasury/taxation.

Document Specifications

| Fact Name | Description |

|---|---|

| Applicable Law | Governing law for NJ 1040 ES is Chapter 55, Public Law 2004 |

| Form Purpose | Used by nonresident individuals, estates or trusts selling property in New Jersey |

| Required Information | Includes seller(s) information, property description, seller's percentage of ownership, consideration, and closing date |

| Significance of Signature | Seller's signature confirms the declaration is true, correct, and complete. Power of Attorney must be recorded if not the seller signing |

| Payment Calculation | Tax payment is 2% of the consideration or the gain on the sale multiplied by 8.97%, whichever is higher |

| Submission Process | The NJ-1040-ES form and payment must be given to the buyer or the buyer's attorney at the time of closing for submission |

Detailed Steps for Using Nj 1040 Es

Filling out the NJ 1040 ES form is a required step for nonresident individuals, estates, or trusts selling property in New Jersey and involves declaring estimated gross income tax on the sale. The process, while seemingly straightforward, requires attention to detail to ensure all information provided is accurate and complete. Failure to do so could prevent the deed from being recorded. Follow the steps below carefully to complete this form correctly.

- Start by listing the Name(s) of the seller(s) involved in the transaction. If there is more than one owner, and they are not a married/civil union couple filing jointly, separate forms should be used.

- Provide the Address of the seller(s), which should be their primary residence or place of business. Do not list the address of the property being sold, unless no new residence has been established.

- Under Property Information, enter the details as listed on the deed of the property being sold, including Block(s), Lot(s), Qualifier, and the Street Address.

- Input the Seller’s Percentage of Ownership if there is more than one owner, making sure to list each seller's percentage.

- Record the total Consideration received for the property. This represents the total compensation paid for the title transfer, including money, the monetary value of other things of value, and any remaining mortgage amounts assumed by the grantee. If multiple owners are involved, indicate each seller's share of the consideration received.

- The Date and Signature(s) of the seller(s) are mandatory at the bottom of the form. If someone other than the seller is signing, ensure a Power of Attorney has been previously recorded or is being recorded simultaneously with the deed. Alternatively, attach a letter signed by the seller(s) granting authority to sign.

- Complete the NJ-1040-ES portion at the bottom of the form by providing the social security number or federal tax identification number of the seller(s), the amount of tax payment determined by applying the Gross Income Tax rate or 2% of the consideration received, whichever is applicable.

- Make a payment in the form of a check or money order payable to State of New Jersey - Division of Taxation. Cash payments are not accepted. Include the seller's social security number on the check or money order to ensure proper credit.

- Submit the completed form and associated payment to the buyer or the buyer's attorney at the time of closing. It is their responsibility to submit the original Sellers Declaration of Tax to the county clerk when recording the deed.

The county clerk attaches the top portion of this form to the recorded deed and forwards the NJ-1040-ES along with the payment to the State of New Jersey, Revenue Processing Center. By following these steps accurately, sellers can ensure the smooth processing of their property sale and comply with New Jersey tax laws.

Learn More on Nj 1040 Es

What is the NJ 1040 ES Form?

The NJ 1040 ES Form, associated with the State of New Jersey, serves as the Declaration of Estimated Tax specifically designed for individuals, estates, or trusts selling property in New Jersey if they are not residents of the state. This form must be completed to accurately declare the estimated taxes due on the sale, ensuring compliance with New Jersey's tax laws.

Who needs to complete the NJ 1040 ES Form?

This form is a requirement for nonresident individuals, estates, or trusts that are selling property located within New Jersey. The need to complete this form arises from transactions occurring on or after August 1, 2004. Each seller, when not filing jointly as a husband and wife or civil union couple, should use separate forms to declare their portion of tax due.

What information is necessary to fill out the NJ 1040 ES Form?

- Seller(s) Information: This includes the name(s) of the seller(s), along with their street address, city, state, and zip code, which should reflect their primary residence or place of business, not the property being sold.

- Property Information: Details such as block(s), lot(s), qualifier, and street address of the property being sold are required.

- Percentage of Ownership: Seller's percentage share of the ownership should be listed if there are multiple owners.

- Consideration: The total compensation received for the property, including money and other values, adjusted for any mortgage or encumbrance that remains to be paid by the grantee.

- Signature: All sellers must sign and date the form. If a representative signs the form, proper documentation granting authority must also be provided.

How is the tax payment calculated and made?

The tax payment is calculated by multiplying the gain from the property sale by the highest Gross Income Tax rate of 8.97%. However, the minimum payment cannot be less than 2% of the total consideration received. Payments should be made by check or money order, payable to the State of New Jersey - Division of Taxation. It is critical to include the seller's social security number or federal tax identification number to ensure proper credit for the payment.

What happens if the NJ 1040 ES Form is not completed or the tax is not paid?

Failure to complete the NJ 1040 ES Form in its entirety or to make the necessary tax payment at the time of closing will result in the deed not being recorded. The form and payment must be given to the buyer or the buyer's attorney at closing. The county clerk will attach the top portion of the form to the deed upon recording, and the bottom portion, along with the payment, is forwarded to the State of New Jersey, Revenue Processing Center. It is imperative to comply with these requirements to avoid legal complications and ensure that the property transfer is properly documented.

Common mistakes

When completing the NJ 1040 ES form, individuals often encounter pitfalls that can lead to inaccuracies or omissions, potentially causing delays or penalties. Understanding these common mistakes can ensure a smoother process for nonresident sellers in New Jersey.

Failing to correctly identify the property details such as Block(s), Lot(s), and the precise Street Address. This information must directly match the details listed on the property deed. Any discrepancy between the form and the deed details can lead to complications during the sale process.

Incorrectly stating the Seller’s Percentage of Ownership and the Consideration received for the property. It is crucial to accurately calculate and represent one's share of ownership and the total consideration, as these figures directly influence the tax implications of the property sale. This mistake can lead to an incorrect tax payment calculation.

Omitting the Seller(s) Social Security Number or Federal Tax Identification Number. This oversight can result in the inability of the State of New Jersey - Division of Taxation to properly credit the payment to the seller(s), potentially causing unnecessary follow-up and verification.

Not attaching the required Power of Attorney documentation or letter of authority from the seller(s) when the declaration is signed by a representative. This documentation is necessary to verify the representative's authority to act on behalf of the seller(s). Failure to provide this documentation can invalidate the submission.

Furthermore, it is worth highlighting a few best practice tips to avoid these common mistakes:

Thoroughly review all property details against the deed before submission to ensure all information is consistent and accurate.

Understand the definition of Consideration in the context of the NJ 1040 ES form to accurately calculate and report the amount.

Ensure that all necessary documents, including the Power of Attorney if applicable, are completed and attached to the NJ 1040 ES form before submitting it.

Consult with a professional if there is any uncertainty regarding the calculation of taxes or the completion of any part of the form. Even small errors can lead to significant delays or additional costs.

By paying close attention to these details, sellers can avoid the pitfalls that often accompany the completion of the NJ 1040 ES form, ensuring a smoother, more accurate process.

Documents used along the form

When handling property transactions in New Jersey, especially for nonresidents, it's crucial to understand the NJ 1040-ES form and its companions. These documents play a vital role in ensuring compliance with state taxation laws and facilitating smooth property sales. Here's an overview of other essential forms and documents often used alongside the NJ 1040-ES form.

- GIT/REP Forms: The GIT/REP series, including GIT/REP-1 (Nonresident Seller’s Tax Declaration), GIT/REP-2 (Nonresident Seller’s Tax Prepayment Receipt), GIT/REP-3 (Seller’s Residency Certification/Exemption), GIT/REP-4 (Waiver of Seller’s Filing Requirement of GIT/REP Forms and Payment), are crucial for nonresident sellers. They address various tax situations and exemptions specific to the nonresident sale of property in New Jersey.

- W-9 Form: Request for Taxpayer Identification Number and Certification, this form is used to request the seller's taxpayer identification number (TIN), which is necessary for reporting to the IRS.

- 1099-S Form: Proceeds from Real Estate Transactions, it's used to report the sale or exchange of real estate to the IRS and the seller, including the gross proceeds from the transaction.

- HUD-1 Settlement Statement: Although replaced by the Closing Disclosure form for most real estate transactions, the HUD-1 is still used for certain types of transactions. It itemizes all charges to seller and buyer in a real estate transaction.

- Closing Disclosure: This form outlines the final terms and costs of the mortgage and is essential for real estate transactions involving a loan. It provides details on loan fees, interest rate, monthly payments, and closing costs.

- Deed of Sale: The document that officially transfers ownership from the seller to the buyer. It must be completed, signed, and, often, notarized.

- Power of Attorney: If the seller is unable to personally attend the closing, a Power of Attorney may be needed to authorize another individual to sign on their behalf.

- Property Tax Statements: Current property tax statements can be required to show the property's tax status and any due or outstanding charges at the time of sale.

- Title Insurance Policy: Offers protection against claims on the property's title that were not found during the initial title search.

- Home Inspection Reports: While not directly related to the tax process, home inspection reports might be needed for final negotiations before closing the sale.

Understanding these documents and their purposes can significantly reduce the complexity and stress of selling property in New Jersey, especially for nonresidents. Correctly filing and managing these documents ensures legal compliance, smooths the transaction process, and provides both the seller and buyer with protection and peace of mind during the sale. Navigating these requirements with care is essential for a successful real estate transaction.

Similar forms

The IRS Form 1040-ES, "Estimated Tax for Individuals," is quite similar to the NJ 1040-ES document as both are designed for taxpayers to pay estimated taxes on income that is not subject to withholding. This includes earnings from self-employment, interest, dividends, alimony, rent, gains from the sale of assets, prizes, and awards. Both forms serve the same purpose but are used for different jurisdictions, with the IRS form being for federal taxes and the NJ 1040-ES specifically for New Jersey state taxes.

The Schedule D (Form 1040), "Capital Gains and Losses," shares similarities with the property sale aspect of the NJ 1040-ES form. While the NJ 1040-ES is utilized for estimating taxes due on the gain from selling a property in New Jersey, Schedule D is used to report the overall gains or losses from asset sales, including real estate, on a federal level. Both require the taxpayer to detail the sale of assets, but the NJ form is focused on a specific transaction's state tax implications.

The W-9, "Request for Taxpayer Identification Number and Certification," relates closely to the NJ 1040-ES as both require taxpayer identification numbers to ensure proper tax reporting and payment processing. The NJ 1040-ES requires this information for effectively crediting the taxpayer's payment, much like how the W-9 is used by entities to accurately report income paid to individuals and businesses to the IRS.

The 1099-S, "Proceeds from Real Estate Transactions," is a federal form that parallels the property sale reporting component of the NJ 1040-ES. Both documents are concerned with real estate transactions, where the 1099-S is used by the seller's agent to report the sale's proceeds to the IRS, and the NJ 1040-ES involves estimating and paying state tax on the gain from such a sale to the New Jersey Department of Taxation.

Form 8962, "Premium Tax Credit (PTC)," while primarily concerned with the Affordable Care Act tax credits, also revolves around accurately estimating and reconciling certain financial aspects with the IRS, akin to the NJ 1040-ES's function of estimating taxes due. Both forms deal with complex calculations to determine the appropriate amounts for tax responsibilities or benefits.

The NJ GIT/REP forms, including the Nonresident Seller’s Tax Declaration, share a direct purpose with the NJ 1040-ES in the context of real estate transactions. Where GIT/REP forms are used to declare income and withhold taxes directly from real estate sales, the NJ 1040-ES serves the broader purpose of estimating and paying taxes on gains from such sales, underscoring their connected roles in real estate taxation in New Jersey.

Form W-2, "Wage and Tax Statement," though primarily for employment income, has an indirect similarity with the NJ 1040-ES in the aspect of providing critical information for tax calculation and payment. While W-2 forms report wages and taxes withheld to employees and the IRS, the NJ 1040-ES represents a self-assessed estimation of tax due, demonstrating the spectrum of tax reporting mechanisms.

The Form 8283, "Noncash Charitable Contributions," parallels the NJ 1040-ES in that both involve declarations related to value and tax implications—8283 for the donated property value and NJ 1040-ES for estimations of tax due on income not subjected to withholding. Each requires detailed documentation for different purposes within the tax filing process.

The Schedule E (Form 1040), "Supplemental Income and Loss," is akin to the NJ 1040-ES as it pertains to reporting income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs on a federal level. The NJ 1040-ES addresses a subset of these incidents (gain from real estate sales) for state tax estimates, showing how different forms capture various income types across jurisdictions.

Finally, the Form 4868, "Application for Automatic Extension of Time To File U.S. Individual Income Tax Return," while serving a different function—extending the deadline to file a tax return—still embodies the anticipation of future tax liabilities. Similar to how the NJ 1040-ES involves estimating taxes due before the actual filing, Form 4868 requires an estimate of the tax liability to ensure proper extension request processing.

Dos and Don'ts

When filling out the NJ 1040 ES form, it's important to follow the correct procedures and avoid common mistakes to ensure the form is accepted and processed efficiently. Here are some dos and don'ts to help guide you through the process:

Do:- Print or type the information clearly to avoid any misinterpretation of your entries.

- Include the seller(s) name(s), ensuring if there are multiple owners, each gets represented accurately.

- Provide the correct address, not the address of the property being sold unless it is still the primary residence or place of business.

- Accurately list the property information as it appears on the deed.

- Correctly calculate and list the seller(s) percentage of ownership if there is more than one owner.

- Declare the total consideration received for the property, making sure to list the seller's portion if ownership is shared.

- Sign and date the declaration, ensuring that if a representative is signing, a Power of Attorney has been recorded or is being recorded simultaneously with the deed.

- Include your social security number or federal tax identification number on the form.

- Make your check or money order payable to the State of New Jersey - Division of Taxation; cash is not acceptable.

- Submit the completed form and associated payment at the time of closing to the buyer or the buyer's attorney.

- Leave any sections of the form blank; incomplete forms may result in the deed not being recorded.

- Use the property's address as the seller's address if a new primary residence or place of business has been established.

- Forget to list the percentage of ownership if the property is owned jointly by more than one person.

- Miscalculate the total consideration received for the property or the seller’s portion of it.

- Sign the declaration without a previously recorded Power of Attorney if a representative is completing the form on the seller’s behalf.

- Forget to include your social security number or federal tax identification number, leading to processing delays.

- Attempt to make the payment in cash, as it is not an acceptable form of payment for this process.

- Omit any required documentation, such as the power of attorney, if applicable.

- Miss the deadline for submission at the time of closing, which can complicate the sale process.

- Fail to check the Division of Taxation’s web page for any updates or additional requirements related to the sale of real estate.

Misconceptions

Understanding the intricacies of tax forms can be daunting, and the NJ 1040 ES form is no exception. Common misconceptions often lead to confusion or errors. Let’s address and clarify seven of the most frequent misunderstandings about this form.

Only for Residents: Many believe the NJ 1040 ES form is strictly for New Jersey residents. However, this form is also crucial for nonresident individuals, estates, or trusts selling property in New Jersey. It caters to all sellers, regardless of their residency status, provided the property in question is located within the state.

Use of Property Address: A common error is using the address of the property being sold as the seller’s address. The form requires the seller’s primary residence or place of business address. This specification ensures that correspondence related to the tax form reaches the seller and not the property that has been sold.

Single Ownership Assumption: It's often assumed that if a property is owned by more than one person, they must file a single NJ 1040 ES form collectively. However, separate forms should be used for each owner, except for married couples or civil union partners filing jointly. This distinction is crucial for accurately recording each individual’s share of ownership and responsibility.

Payment Methods: There's a misconception that tax payments can only be made through checks. The form explicitly allows for payment via money orders as well. Importantly, cash payments are not acceptable, ensuring a documented trail of payment for both the seller and the New Jersey Division of Taxation.

Setting the Sale Price as Consideration: Misunderstanding surrounds the term “consideration” on the form. Consideration is not merely the sale price; it encompasses the entire compensation, including the amount of any prior mortgage assumed by the grantee and any other liens. Understanding this helps in accurately declaring the transaction’s value.

Signature Authority: A significant point of confusion lies in who needs to sign the form. If a representative is signing on behalf of the seller(s), it’s often mistaken that a Power of Attorney is always necessary. While that’s one method, a letter signed by the seller(s) granting authority to the representative is also acceptable. This flexibility aids in situations where a Power of Mortgage hasn’t been configured.

Tax Payment Calculation: Another frequent misconception is about how the tax payment is determined. The form stipulates that the payment is calculated by multiplying the gain on the sale of the property by New Jersey's highest Gross Income Tax rate of 8.97%, debunking the myth that the payment is a flat or arbitrary fee. However, it’s also clarified that the payment can't be less than 2% of the received consideration, ensuring a minimum threshold.

These clarifications aim to demystify the NJ 1040 ES form and facilitate a smoother transaction process for all parties involved. Understanding these key points ensures compliance with New Jersey’s tax regulations and avoids common pitfalls during property sales.

Key takeaways

When managing the complexities of real estate transactions in New Jersey, particularly for nonresident individuals, estates, or trusts, it is essential to accurately complete and use the NJ 1040-ES form. Here are key takeaways to guide you through this process:

- The NJ 1040-ES form is specifically designed for nonresident sellers declaring estimated taxes on the sale of property within New Jersey.

- Accurate seller information, including names and address details, must be provided. This information should reflect the seller's primary residence or place of business, not the address of the sold property.

- A detailed description of the property, including block and lot numbers, is required to correctly identify the estate in question.

- The form requires the seller's percentage of ownership and the total consideration received from the sale, guiding the tax calculation.

- Understanding the term "consideration" is crucial; it encompasses the total compensation for the property transfer, including monetary value and any assumed liabilities.

- Sellers must sign and date the declaration, with the stipulation that any representative signing on their behalf must have a recorded Power of Attorney or an attached authorization letter from the sellers.

- Payment should be made via check or money order to the State of New Jersey - Division of Taxation, with the seller’s social security number or federal tax identification number included to ensure accurate processing.

- Failure to accurately complete and submit the NJ-1040-ES form and associated payment at the time of closing will prevent the deed from being recorded, emphasizing the importance of completeness and timeliness in these transactions.

Handling the NJ-1040-ES form with diligence ensures compliance with New Jersey’s real estate taxation laws, avoiding potential legal and financial repercussions. Sellers, and their representatives, are advised to thoroughly review and verify the form’s contents before submission, alongside adhering to specified payment instructions. This due diligence safeguards the interests of all parties involved in the transaction.

Popular PDF Documents

Are Employment Applications Required by Law - Define your employment interests with options ranging from full-time positions to weekend shifts, indicating your flexibility and availability.

New Jersey Boiler License Renewal - The document’s detailed instructions and general information section serve as a comprehensive guide for successful license renewal, aiding applicants in navigating the process with ease.