Fill Out a Valid Nj 1040 O Template

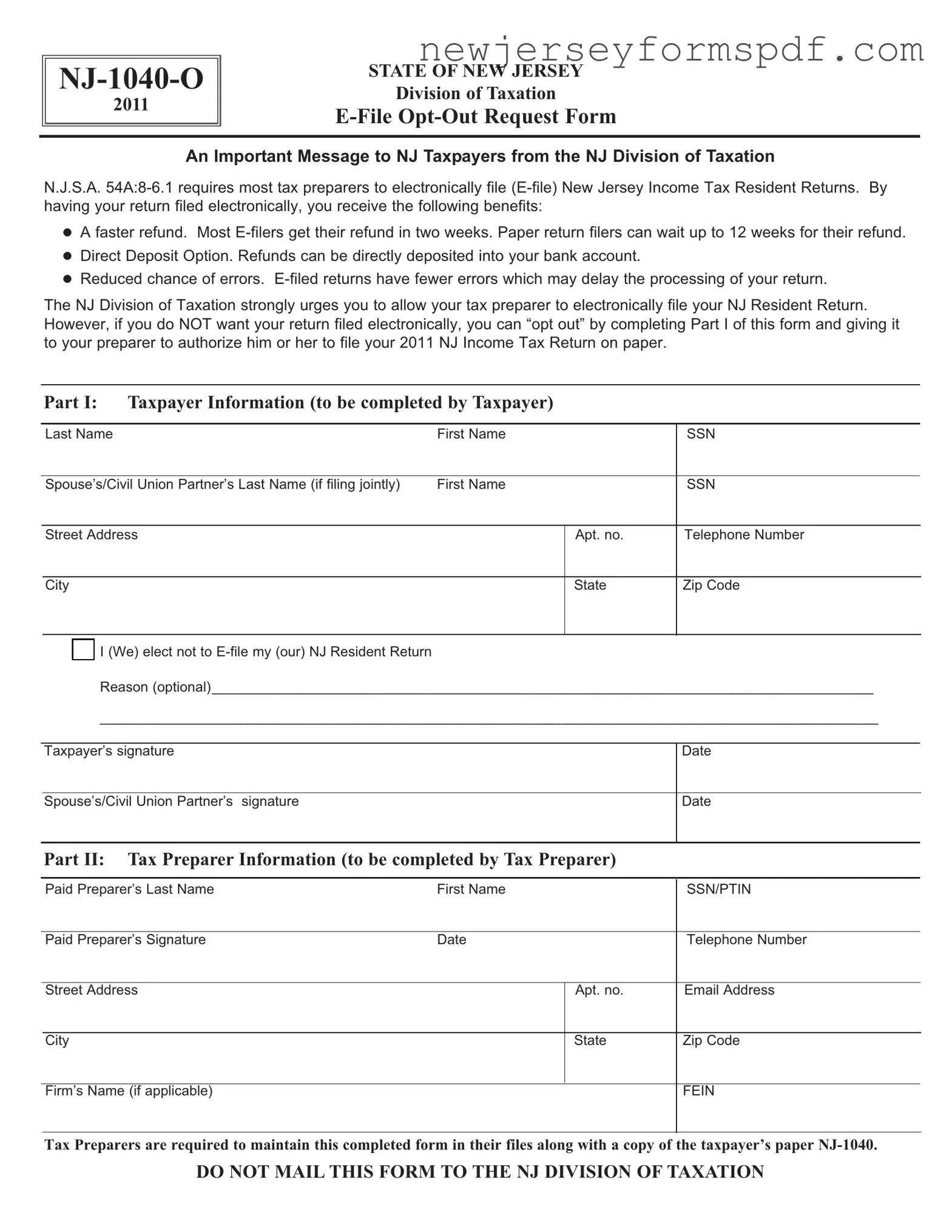

The NJ-1040-O form serves as a critical document within the framework of New Jersey's state taxation, focusing on the intersection between technology, efficiency, and taxpayer autonomy. Mandated by N.J.S.A. 54A:8-6.1, the directive primarily aims at encouraging electronic filing (E-file) for the swift and error-free submission of New Jersey Income Tax Resident Returns. The merits of this method are notable, offering expedited refund processing—often within two weeks as opposed to the up to 12 weeks for paper returns—, an option for direct deposit of refunds, and a notable reduction in filing errors. Nevertheless, the State of New Jersey's Division of Taxation acknowledges the diversity of taxpayer preferences and circumstances by providing an "opt-out" provision through the NJ-1040-O form. This form embodies a conscious balance between technological advancement and individual choice, permitting taxpayers who prefer or require the submission of paper returns to formally do so. By completing Part I of this form, taxpayers can communicate their decision not to utilize electronic filing for their NJ Resident Return, a choice that must then be relayed to and facilitated by their tax preparer, who completes Part II of the document. What stands out about this procedure is not merely the administrative aspect but the broader commitment to accommodating varied taxpayer needs while still advocating for the efficiency of electronic filing. The form, and the process it represents, underscores the evolving nature of tax administration in embracing digital solutions, while also safeguarding taxpayer rights to make informed choices about their filing methods.

Sample - Nj 1040 O Form

2011

STATE OFNEWJERSEY

Division ofTaxation

An Important Message to NJ Taxpayers from the NJ Division of Taxation

N.J.S.A.

A faster refund. Most

Direct Deposit Option. Refunds can be directly deposited into your bank account.

Reduced chance of errors.

The NJ Division of Taxation strongly urges you to allow your tax preparer to electronically file your NJResident Return. However, if you do NOT want your return filed electronically, you can “opt out” by completing Part I of this form and giving it to your preparer to authorize him or her to file your 2011 NJ Income Tax Return on paper.

Part I: TaxpayerInformation (to be completed byTaxpayer)

Last Name |

First Name |

SSN

Spouse’s/Civil Union Partner’s Last Name (if filing jointly) |

First Name |

SSN

Street Address

Apt. no.

Telephone Number

City

State

Zip Code

I (We) elect not to

Reason (optional)_____________________________________________________________________________________

____________________________________________________________________________________________________

Taxpayer’s signature |

Date |

Spouse’s/Civil Union Partner’s signature

Date

Part II: Tax PreparerInformation (to be completed byTax Preparer)

Paid Preparer’s Last Name |

First Name |

SSN/PTIN

Paid Preparer’s Signature |

Date |

Telephone Number

Street Address

Apt. no.

Email Address

City

State

Zip Code

Firm’s Name (if applicable)

FEIN

Tax Preparers are required to maintain this completed form in their files along with a copy of the taxpayer’s paper

DO NOTMAILTHIS FORMTOTHE NJ DIVISION OFTAXATION

Document Specifications

| Fact Number | Detail |

|---|---|

| 1 | The form number is NJ-1040-O for the year 2011 |

| 2 | It is issued by the State of New Jersey Division of Taxation |

| 3 | Its primary purpose is to serve as an E-File Opt-Out Request Form |

| 4 | Governed by N.J.S.A. 54A:8-6.1 |

| 5 | Targets NJ income tax resident returns |

| 6 | E-filing is mandated for most tax preparers, but taxpayers can opt out |

| 7 | Benefits of E-filing include faster refunds, direct deposit options, and reduced chance of errors |

| 8 | Opting out requires completing Part I, which necessitates taxpayer information |

| 9 | Tax preparers must maintain a completed copy of this form and a copy of the taxpayer’s paper NJ-1040 |

| 10 | The form should not be mailed to the NJ Division of Taxation |

Detailed Steps for Using Nj 1040 O

Filling out the NJ-1040-O form is a straightforward process that enables taxpayers in New Jersey to opt out of electronically filing their state income tax returns. While e-filing is encouraged due to its benefits such as faster refunds, direct deposit options, and a reduced chance of errors, some taxpayers may prefer or need to file a paper return. Following the steps below will guide you through completing the NJ-1040-O form accurately.

- Start by entering your Last Name and First Name in the designated fields.

- If filing jointly, provide your spouse’s or civil union partner’s Last Name and First Name.

- Enter Social Security Numbers (SSN) for both yourself and your spouse or civil union partner, if applicable.

- Fill in your complete Street Address, including the Apt. no. if you live in an apartment.

- Provide a Telephone Number where you can be reached.

- Include your City, State, and Zip Code.

- In the section labeled "I (We) elect not to E-file my (our) NJResident Return", you have the option to explain your reason for opting out of electronic filing. Though it's optional, detailing your reason can provide useful feedback.

- Sign and date the form in the designated area. If filing jointly, your spouse or civil union partner must also sign and date the form.

For tax preparers completing Part II:

- Enter your Last Name, First Name, and SSN/PTIN.

- Sign and date the form in the space provided.

- Include your Telephone Number and Email Address for communication purposes.

- Provide your Street Address, including Apt. no., City, State, and Zip Code.

- If applicable, fill in your firm’s Name and FEIN.

After completing the form, remember that it should not be mailed to the New Jersey Division of Taxation. Instead, tax preparers are required to keep the completed form along with a copy of the taxpayer's paper NJ-1040 form in their records. This step ensures compliance with state regulations and facilitates a smooth filing process for both the taxpayer and the preparer.

Learn More on Nj 1040 O

What is the NJ-1040-O Form?

The NJ-1040-O form is an E-File Opt-Out Request Form designed for New Jersey residents. It allows taxpayers to request that their tax preparer file a paper return instead of submitting it electronically. The state of New Jersey usually requires tax returns to be filed electronically due to the benefits such as faster refunds, direct deposit options, and a reduced chance of errors. However, if a taxpayer prefers not to use electronic filing, they can complete the NJ-1040-O form to opt out.

Why would someone choose to opt-out of electronic filing?

There are various reasons why a taxpayer might choose to opt-out of electronic filing. Some individuals might not have reliable internet access, while others may simply prefer paper documentation for their personal records. Additionally, some taxpayers might be concerned about electronic security and therefore prefer the physical submission of their tax returns. The form allows taxpayers to indicate their reason for opting out, but providing a reason is optional.

How can I opt-out of E-filing my New Jersey Income Tax Return?

To opt-out of E-filing your New Jersey Income Tax Return, you need to:

- Complete Part I of the NJ-1040-O Form, which includes your personal information and, if filing jointly, your spouse’s or civil union partner’s information.

- Indicate your choice to opt out of E-filing by signing the form. Your spouse or civil union partner must also sign if filing jointly.

- Provide the completed form to your tax preparer, authorizing them to file your NJ Income Tax Return on paper.

What should I do with the NJ-1040-O form after completing it?

After you complete the NJ-1040-O form, you should not mail it to the New Jersey Division of Taxation. Instead, give the completed form to your tax preparer. The tax preparer is required to keep the form in their files along with a copy of your paper NJ-1040 tax return. This form serves as authorization for the tax preparer to file a paper return on your behalf.

Are there any benefits to E-filing opposed to opting out?

Yes, there are several benefits to E-filing your New Jersey Income Tax Return, including:

- A faster refund, with most E-filers receiving their refund within two weeks compared to up to 12 weeks for paper return filers.

- The option to have your refund directly deposited into your bank account.

- A reduced chance of errors in your tax return, which may delay the processing of your return.

Common mistakes

When filling out the NJ-1040-O form, people often make mistakes that can potentially delay the processing of their tax documents or affect their tax outcomes. It's crucial to pay attention to detail and accurately complete every section. Here are six common mistakes to avoid:

Not double-checking the Taxpayer Information. Ensure that all personal information, including the Social Security Number (SSN), address, and names, is correctly filled out. Mistakes here can lead to delays or misfiled returns.

Skipping the spouse’s or civil union partner’s details. If filing jointly, it’s essential to provide accurate information for both parties. Omitting the spouse’s or civil union partner's SSN or name can invalidate your opt-out request.

Forgetting to sign and date the form. Both the taxpayer and the spouse or civil union partner must sign and date the form. Unsigned forms are not processed, causing delays in return filings.

Incomplete Tax Preparer Information. If a tax preparer is involved, all their details, including the SSN/PTIN and contact information, must be accurately provided. Incomplete information can affect the credibility and traceability of the filed return.

Not accurately stating the reason for opting out. While it's optional, providing a clear reason for not e-filing can help in the documentation and understanding of taxpayers' preferences. Vague or missing reasons might raise unnecessary questions.

Ignoring the instruction to not mail the form to the NJ Division of Taxation. This form should be handed to the tax preparer and not mailed directly to the NJ Division of Taxation. Doing so can lead to misplacement or loss of your form, delaying the process further.

Avoiding these common mistakes can streamline the process of opting out of electronic filing and ensure your NJ-1040-O form is correctly processed without unnecessary delay.

Documents used along the form

Navigating the complexities of tax filings can sometimes feel like solving a puzzle with pieces scattered everywhere. For New Jersey residents, the NJ-1040-O form represents one of these pieces, specifically designed for those who choose to opt-out of electronic filing. This decision, while not common, triggers the need for additional forms and documents that ensure one's tax affairs are in complete order. Here, we introduce a subset of documents often accompanying the NJ-1040-O form, shedding light on the cohesive picture of tax filing in the Garden State.

- NJ-1040: This is the New Jersey Resident Income Tax Return. It's the main form for residents to report their annual income. When someone opts out of electronic filing with the NJ-1040-O, they must submit this paper form to detail their income, deductions, and calculate their tax liability or refund.

- Schedule NJ-BUS-1: New Jersey Business Income Summary Schedule. This form accompanies the NJ-1040 for those who report income from business operations, rent, royalties, or partnerships. It helps organize the flow of this specific type of income into the New Jersey resident income tax return.

- NJ-1040-ES: Estimated Tax Voucher for Individuals. For taxpayers who anticipate owing more than a certain amount in taxes and do not have sufficient withholdings, this voucher allows them to make quarterly estimated tax payments to avoid penalties for underpayment.

- NJ-2450: Claim for Excess Unemployment/Disability/Family Leave Insurance Contributions. Workers who have had more than one employer and earned above a certain threshold may have paid more into the state's unemployment, disability, or family leave insurance than required. This form lets them claim a refund for those overpayments.

- NJ-2210: Underpayment of Estimated Tax by Individuals, Estates, or Trusts. This form is for filers who did not pay enough in estimated tax throughout the year, either through quarterly payments or withholdings. The NJ-2210 helps calculate any penalties due for underpayment of estimated taxes.

Filing taxes is a civic duty that, while complex, contributes to the wider community's well-being. Each form, including and beyond the NJ-1040-O, plays a crucial part in ensuring individuals meet their obligations accurately and efficiently. The documents listed here form a backbone to the tax filing process in New Jersey, guiding taxpayers through various scenarios from traditional income reporting to specific circumstances requiring further detail or claim for overpaid funds. Understanding the purpose and application of these forms demystifies the process, turning what can often feel like a daunting task into a manageable and, yes, even fulfilling contribution to society.

Similar forms

The Form 1040 for the IRS is quite similar to the NJ-1040-O due to its fundamental role in the federal income tax filing process. Like the NJ-1040-O, which is specific to New Jersey residents, the IRS Form 1040 serves as the primary income tax form for individuals within the United States. Both forms collect essential taxpayer information, including income sources, tax credits, and deductions which are crucial for determining the taxpayer's liability or refund. However, the IRS Form 1040 applies federally, while the NJ-1040-O is state-specific.

The NJ-1040-ES, the Estimated Tax for Individuals form, shares commonalities with the NJ-1040-O, as both are integral to New Jersey's tax filing requirements. The NJ-1040-ES is used for estimating and paying quarterly taxes, while the NJ-1040-O pertains to opting out of electronic filing for annual returns. Each form serves taxpayers at different stages of their tax obligations, ensuring compliance and facilitating smooth processing by the state's taxation division.

The U.S. 4868 Form, an Application for Automatic Extension of Time To File U.S. Individual Income Tax Return, parallels the NJ-1040-O in providing taxpayers with a specific request mechanism. While the 4868 Form allows taxpayers more time to file their federal returns, the NJ-1040-O lets New Jersey taxpayers request paper filing as opposed to the default e-filing. Both forms are crucial for taxpayers who wish to deviate from standard filing procedures.

New Jersey's GIT/REP-3, the Nonresident Seller's Tax Declaration, also relates closely to the NJ-1040-O form. Both are utilized under specific circumstances by New Jersey residents or parties conducting transactions within the state. The NJ-1040-O serves residents opting out of e-filing for their income tax, whereas the GIT/REP-3 is used by nonresidents to declare income from New Jersey sources, highlighting the state's effort to accommodate diverse taxpayer needs.

The W-2 Form, issued by employers to report employee wage and salary information to the IRS, shares a foundational purpose with the NJ-1040-O. Both are critical for accurately reporting income, albeit in different contexts. The W-2 is necessary for employees to complete their 1040 forms, and similarly, the NJ-1040-O is essential for New Jersey taxpayers who choose to file paper returns, underlining their roles in the broader tax reporting ecosystem.

New Jersey's NJ-1040NR form, for Nonresident Income Tax Return filing, while distinct, shares similarities with the NJ-1040-O. Both cater to specific groups within New Jersey's tax framework - the NJ-1040NR for nonresidents earning in NJ, and the NJ-1040-O for residents opting out of electronic filing. Each form ensures that all taxpayers, regardless of residency status or filing preferences, are accommodated within the state's taxation system.

The IRS Schedule C, used by sole proprietors to report profits and losses from their business, aligns with the NJ-1040-O in its focus on specific taxpayer situations. While Schedule C pertains to federal tax obligations for individual business owners, the NJ-1040-O addresses New Jersey residents' preference for paper filing over electronic submission. Both documents cater to niche aspects of tax filing, ensuring diverse taxpayer needs are met efficiently.

Finally, the Form W-9, Request for Taxpayer Identification Number and Certification, is somewhat analogous to the NJ-1040-O. Although the W-9 is used to provide necessary taxpayer identification information to entities that pay them, aligning with federal requirements, its importance in ensuring accurate tax reporting mirrors the role of the NJ-1040-O in New Jersey's state taxation context. Both forms help streamline tax administration, ensuring accurate reporting and compliance.

Dos and Don'ts

When dealing with the NJ-1040-O form, a document essential for New Jersey residents who opt out of electronically filing their tax returns, it's important to follow certain guidelines to ensure the process is handled correctly. Below is a list of dos and don'ts that could help in filling out the NJ-1040-O form accurately and efficiently.

Do:

Read the form thoroughly before you start filling it out to make sure you understand all the requirements.

Ensure all taxpayer information is filled out completely and accurately, including the last name, first name, social security number (SSN), and contact details.

Check if you're filing jointly and include your spouse’s or civil union partner's details if applicable.

Clearly state your reason for opting out of electronic filing if you choose to provide one, as this section is optional.

Sign and date the form, as this signifies your decision to opt-out and is a crucial step for the process.

Don't:

Leave any required fields blank, especially in the Taxpayer Information section, as this could lead to the form being returned or processed incorrectly.

Forget to give the completed form to your tax preparer, as they need it for their records and to proceed with filing your NJ-1040 paper return.

Mail this form to the NJ Division of Taxation, as it should only be retained by your tax preparer.

Dismiss the option to e-file without considering the benefits, such as faster refunds and reduced chances of errors, unless you have a specific reason to opt out.

It's imperative to follow these guidelines closely to ensure your NJ-1040-O form is completed correctly and to avoid any unnecessary delays in processing your paper tax return. Keep in mind that electronic filing offers several advantages but opting out is your right if you prefer to file a paper return.

Misconceptions

When discussing the New Jersey 1040-O form, it's important to address common misconceptions that often confuse taxpayers. Clarifying these misunderstandings can help ensure taxpayers are fully informed about their filing options and the implications of their choices.

- Electronic Filing is Mandatory for All Taxpayers:

One widespread misconception is that electronic filing (E-filing) is compulsory for every taxpayer in New Jersey. While N.J.S.A. 54A:8-6.1 mandates that most tax preparers must E-file New Jersey Income Tax Resident Returns, individuals have the option to opt-out. This form, NJ-1040-O, is specifically designed for taxpayers who prefer not to E-file, allowing them to authorize their preparer to submit a paper return instead.

- The Form Must Be Mailed to the NJ Division of Taxation:

Another common misunderstanding is the belief that the NJ-1040-O form must be mailed to the New Jersey Division of Taxation. The instructions clearly indicate that this form should not be mailed to the NJ Division of Taxation. Instead, it is retained by the tax preparer, who keeps the completed form alongside a copy of the taxpayer's paper NJ-1040 return in their records.

- Opting Out Will Delay Your Refund Significantly:

Many believe that choosing to file a paper return by using the NJ-1040-O form will lead to a significant delay in receiving their tax refund. While it’s true that E-filers typically receive their refund faster — usually within two weeks — paper return filers might wait up to 12 weeks. However, this timeframe is not excessively prolonged, and for some taxpayers, the benefits of paper filing might outweigh the waiting period.

- Filing Electronically Is Prone to More Errors:

Conversely, a less common but equally erroneous belief is that electronic filing is more susceptible to mistakes than paper filing. The reality, as promoted by the NJ Division of Taxation, is that E-filed returns have a reduced chance of errors. This accuracy contributes to the efficiency of processing returns and issuing refunds. The NJ-1040-O form exists not due to concerns about electronic filing accuracy but to provide taxpayers who, for various reasons, prefer or require a paper filing option.

Understanding these misconceptions surrounding the NJ-1040-O form can help taxpayers make informed decisions about their tax filing options while ensuring they comply with New Jersey's tax laws. Whether choosing to E-file or opting out, the key is knowing your rights and responsibilities as a taxpayer.

Key takeaways

Completing and using the NJ-1040-O form, known as the E-File Opt-Out Request Form, involves specific procedures and considerations for taxpayers in New Jersey. Below are key takeaways that individuals should understand when dealing with this form:

- The NJ-1040-O form is specifically designed for New Jersey taxpayers who choose not to file their NJ Resident Return electronically, despite electronic filing (E-filing) being the preferred method by the New Jersey Division of Taxation.

- New Jersey State Law, under N.J.S.A. 54A:8-6.1, mandates most tax preparers to electronically file New Jersey Income Tax Resident Returns due to the associated benefits, such as faster refunds and a reduced chance of errors.

- Benefits of E-filing include receiving refunds within two weeks, the option for direct deposit of refunds, and fewer errors in the processing of returns.

- Paper return filers, as opposed to E-filers, may wait up to 12 weeks for their refund, highlighting the efficiency of E-filing.

- To opt-out of E-filing, taxpayers must complete Part I of the NJ-1040-O form, providing essential information such as names, social security numbers, and contact details.

- Upon deciding to opt-out, taxpayers need to provide their tax preparer with the completed NJ-1040-O form to authorize the paper filing of their New Jersey Income Tax Return.

- The form allows taxpayers to state their reason for opting out of E-filing, although providing a reason is optional.

- Both the taxpayer and, if applicable, the spouse or civil union partner must sign the form, indicating their collective or individual decision to opt-out.

- Tax preparers are required to fill out Part II of the form, which includes the preparer’s information, and maintain the completed NJ-1040-O form along with a copy of the taxpayer's paper NJ-1040 in their files.

- It is crucial for taxpayers and tax preparers alike to note that the NJ-1040-O form should not be mailed to the New Jersey Division of Taxation.

Understanding these key aspects of the NJ-1040-O form ensures that taxpayers in New Jersey can make informed decisions about their filing options while complying with state tax regulations.

Popular PDF Documents

New Jersey D 3 - Features sections for the committee to provide contact details and addresses, ensuring communication pathways are established.

Nj Annulment Forms Pdf - Completing the NJ CN 10482 accurately is critical as it ensures the fair assessment of financial obligations and rights.

What Is Nj 1040 Form - Part-year residents and fiscal year filers have dedicated sections to report their specific circumstances.