Fill Out a Valid Nj 1040 Schedule Nj Bus 1 Template

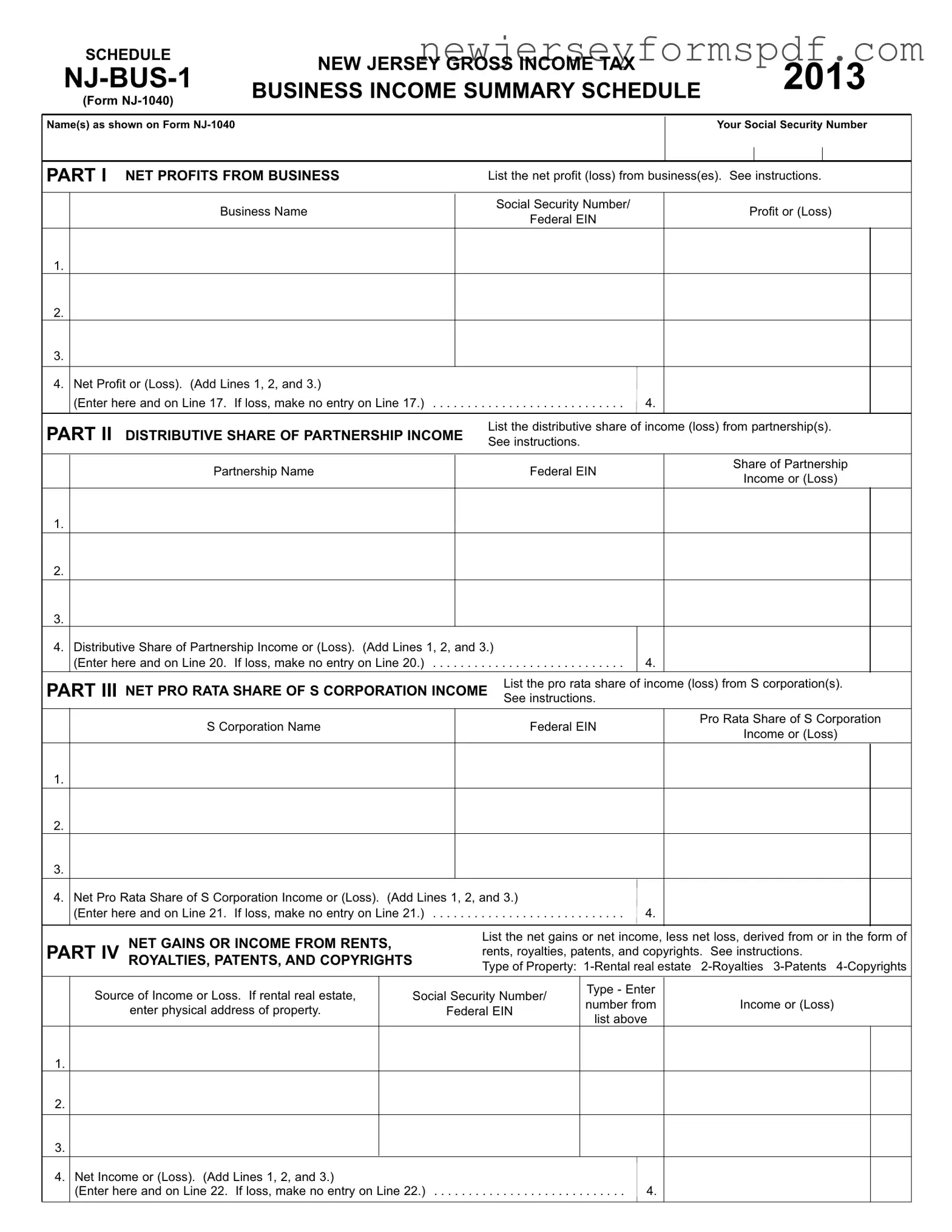

Filing taxes in New Jersey requires an understanding of various forms, especially for those with business income. The NJ 1040 Schedule NJ-BUS-1, a crucial document for reporting business income on your state tax return, encapsulates a detailed overview of an individual's earnings from diverse business ventures. This form is meticulously divided into several parts, each designed to capture specific types of business income. Part I deals with net profits from business, where business owners list their net profit or loss from their ventures. Part II focuses on the distributive share of income from partnerships, ensuring that income from such business structures is accurately reported. The third part delves into the net pro-rata share of S Corporation income, a section critical for shareholders in S corporations. Lastly, Part IV addresses net gains or income from rents, royalties, patents, and copyrights, which encompasses income from property and intellectual properties. For every section, there are detailed instructions on how to list each business' name, the associated social security number or Federal EIN, and the profit or loss incurred. This comprehensive form caters to various business types and income sources, making it a fundamental tool for New Jersey residents to report their business income accurately and comply with state tax obligations.

Sample - Nj 1040 Schedule Nj Bus 1 Form

SCHEDULE |

NEW JERSEYGROSS INCOME TAX |

2013 |

|

BUSINESS INCOME SUMMARYSCHEDULE |

|||

(Form |

|

|

Name(s) as shown on Form

Your Social Security Number

PART I NET PROFITS FROM BUSINESS |

List the net profit (loss) from business(es). See instructions. |

||

|

|

|

|

Business Name |

Social Security Number/ |

Profit or (Loss) |

|

Federal EIN |

|||

|

|

||

1. |

|

|

|

2. |

|

|

|

3. |

|

|

|

|

|

|

|

4. |

Net Profit or (Loss). (Add Lines 1, 2, and 3.) |

|

|

|

(Enter here and on Line 17. If loss, make no entry on Line 17.) |

. . . . . . . . . . . . . . . . . . . . |

4. |

|

|

|

|

PART II DISTRIBUTIVE SHARE OF PARTNERSHIPINCOME |

List the distributive share of income (loss) from partnership(s). |

||

See instructions. |

|

||

|

|

|

|

|

Partnership Name |

Federal EIN |

Share of Partnership |

|

Income or (Loss) |

||

|

|

|

|

1. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Distributive Share of Partnership Income or (Loss). (Add Lines 1, 2, and 3.) |

|

|

|

|

|

|

|

||||

|

(Enter here and on Line 20. If loss, make no entry on Line 20.) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

4. |

|

|

|

||||||

PART III NET PRO RATASHARE OF S CORPORATION INCOME |

List the pro rata share of income (loss) from S corporation(s). |

|||||||||||

|

|

|

|

|

|

See instructions. |

|

|

||||

|

S Corporation Name |

|

|

|

|

Federal EIN |

|

Pro Rata Share of S Corporation |

||||

|

|

|

|

|

|

Income or (Loss) |

||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

|

|

|

|

|

|

|

|

|

|

|

|

2. |

|

|

|

|

|

|

|

|

|

|

|

|

3. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

4. |

Net Pro Rata Share of S Corporation Income or (Loss). (Add Lines 1, 2, and 3.) |

|

|

|

|

|

|

|||||

|

(Enter here and on Line 21. If loss, make no entry on Line 21.) |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . 4. |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

||||

|

NET GAINS OR INCOME FROM RENTS, |

|

|

List the net gains or net income, less net loss, derived from or in the form of |

||||||||

|

|

|

rents, royalties, patents, and copyrights. See instructions. |

|||||||||

PART IV ROYALTIES, PATENTS, AND COPYRIGHTS |

|

|

||||||||||

|

|

Type of Property: |

||||||||||

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source of Income or Loss. If rental real estate, |

|

Social Security Number/ |

Type - Enter |

|

|

|

|||||

|

|

number from |

|

Income or (Loss) |

||||||||

|

enter physical address of property. |

|

|

Federal EIN |

|

|

||||||

|

|

|

|

list above |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

||

1. |

|

|

|

|

|

|

|

|

|

|

|

|

2. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Net Income or (Loss). (Add Lines 1, 2, and 3.) |

|

|

|

|

|

|

|

|

|

|

|

|

(Enter here and on Line 22. If loss, make no entry on Line 22.) |

. . . . |

. . . . . . |

. . . . |

. . . . . . . |

. 4 |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

Document Specifications

| Fact Name | Description |

|---|---|

| Form Type | NJ-1040 Schedule NJ-BUS-1 is a Business Income Summary Schedule. |

| Purpose | The form is used for reporting net profits from business, distributive share of partnership income, net pro rata share of S corporation income, and net gains or income from rents, royalties, patents, and copyrights. |

| Year | The specific form referenced is for the year 2013. |

| Requirements | Taxpayers must list net profit or loss from businesses, their share of partnership income or loss, their share of S corporation income or loss, and income or loss from rents, royalties, patents, and copyrights. |

| Information Required | Business name, Federal EIN, type of property, and the source of income or loss must be provided. |

| Governing Law | This form is governed by New Jersey state tax laws. |

| Submission | It must be submitted as part of the NJ-1040 State Income Tax Return. |

Detailed Steps for Using Nj 1040 Schedule Nj Bus 1

Filling out the NJ 1040 Schedule NJ-BUS-1 form is a crucial step for residents of New Jersey who need to report various types of business income on their state income tax return. This form encapsulates different sources of business income, including net profits from a business, distributive share of partnership income, net pro rata share of S corporation income, and net gains or income from rents, royalties, patents, and copyrights. The process involves carefully documenting amounts for each category and understanding exactly where this information will feed into the overall tax return.

Here are the steps to properly fill out the NJ 1040 Schedule NJ-BUS-1 form:

- Start by entering your name(s) as shown on Form NJ-1040 and your Social Security Number at the top of the form.

- Part I - Net Profits From Business:

- List each business name, along with the associated Social Security Number or Federal EIN, and the profit or (loss) from the business.

- Add up lines 1, 2, and 3, and enter the total net profit or (loss) on line 4. If the result is a loss, do not make any entry on Line 17 of your NJ-1040 form.

- Part II - Distributive Share of Partnership Income:

- For each partnership, list the partnership name, Federal EIN, and your share of the partnership income or (loss).

- Add up lines 1, 2, and 3, and enter the distributive share of partnership income or (loss) on line 4. If the result is a loss, do not enter it on Line 20 of your NJ-1040 form.

- Part III - Net Pro Rata Share of S Corporation Income:

- List each S corporation name, Federal EIN, and your pro rata share of the S corporation's income or (loss).

- Add up lines 1, 2, and 3, and input the sum on line 4 as your net pro rata share. If it's a loss, refrain from entering it on Line 21 of your NJ-1040.

- Part IV - Net Gains or Income from Rents, Royalties, Patents, and Copyrights:

- Identify the type of property (using the number from the list provided) and describe the source of income or loss. If it involves rental real estate, include the physical address of the property.

- Combine the amounts from lines 1, 2, and 3, and document the net income or (loss) on line 4. If a loss is recorded, do not enter it on Line 22 of your NJ-1040.

After completing these steps, review the form for accuracy and consistency with your records. This schedule will help ensure that your business income is accurately reported and that your New Jersey tax return reflects your financial activity correctly.

Learn More on Nj 1040 Schedule Nj Bus 1

What is the NJ 1040 Schedule NJ-BUS-1 form?

The NJ 1040 Schedule NJ-BUS-1 form is a business income summary schedule required by the state of New Jersey as part of the NJ-1040 personal income tax return. It is used to report income or losses from businesses, partnerships, S corporations, and income or losses derived from rents, royalties, patents, and copyrights.

Who needs to fill out the NJ-BUS-1 form?

Individuals who have earned income or incurred losses from business activities conducted in New Jersey, or those who have distributive share of income or losses from partnerships, S corporations, or income from rents, royalties, patents, and copyrights, are required to fill the NJ-BUS-1 form along with their NJ-1040 personal income tax return.

How do you calculate net profits from business for Part I of the form?

To calculate net profits for Part I, list each business, its social security number or Federal EIN, and the net profit or loss. The net profit or loss is typically determined by subtracting business expenses from business income. Total the net profits or losses from each listed business to determine the combined net profit or loss to report on Line 4.

What information is needed for Part II regarding partnership income?

For Part II, you'll need the name of each partnership, its Federal EIN, and your distributive share of income or loss from each partnership. Compile the information for all partnerships and calculate the total distributive share of income or losses to report on Line 4 of this section.

How is the net pro rata share of S corporation income calculated in Part III?

In Part III, list the name and Federal EIN of each S corporation and your pro rata share of income or loss from these entities. Sum all the individual pro rata shares to determine the net amount to be reported on Line 4 of this section.

How should income from rents, royalties, patents, and copyrights be reported in Part IV?

For Part IV, identify each source of income by type—rental real estate, royalties, patents, or copyrights. Next, provide the source of income or loss, including the physical address for rental real estate, and enter the income or loss for each. Sum these amounts to calculate the total net income or loss for this section to be reported on Line 4.

What are the common mistakes to avoid when filling out the NJ-BUS-1 form?

- Failure to report all income sources or incorrectly categorizing them.

- Incorrectly calculating net profits or losses.

- Omitting social security numbers or Federal EINs for businesses or partnerships.

- Not including all necessary supplemental documentation.

Can losses reported on the NJ-BUS-1 form be used to offset other income?

Yes, losses reported on the NJ-BUS-1 form can generally be used to offset other sources of income on your NJ-1040 return. However, specific limitations and rules apply depending on the type of loss and income. Consulting the instructions for the NJ-1040 and NJ-BUS-1 form or a tax professional is recommended for guidance on your specific situation.

Where can individuals find assistance in completing the NJ-BUS-1 form?

Assistance for completing the NJ-BUS-1 form can be found in the instructions provided with the form, on the New Jersey Division of Taxation's website, or through a professional tax preparer or accountant familiar with New Jersey tax law and regulations.

Common mistakes

When filling out the NJ 1040 Schedule NJ-BUS-1 form, many people tend to make a handful of mistakes that can potentially lead to issues down the line. Understanding these common mistakes can help ensure that you fill out the form accurately, thereby avoiding possible hiccups with your tax return. Here are five mistakes to be aware of:

- Incorrect Social Security or Federal EIN numbers: It's crucial to double-check that all Social Security numbers (SSNs) and Employer Identification Numbers (EINs) entered on the form are accurate. Mistaking these numbers can lead to processing delays or incorrect tax calculations.

- Omitting or misreporting income: Failing to list all sources of income, or incorrectly reporting the profit (loss) from businesses, can result in penalties. Make sure every business activity is accounted for and properly reported.

- Miscalculating net profit or loss: When calculating net profit or loss, it's important to ensure that all necessary expenses and incomes are correctly figured into the equation. This common error can affect the bottom line of what's owed to or refundable from the state.

- Forgetting to include distributive share of partnership income: If you're part of a partnership, your distributive share of the income (or loss) must be included. Overlooking this detail can lead to an incomplete return.

- Mixing up types of income or losses: The form requires separation of different types of income (e.g., net profits from business, distributive share of partnership income, S corporation income, and gains or income from rents, etc.). Mixing these up or entering them in the wrong section can lead to inaccuracies in calculating your taxable income.

Being mindful of these mistakes when filling out the NJ 1040 Schedule NJ-BUS-1 form can save you time, stress, and potentially money. Accuracy is key to ensuring your tax obligations are met correctly. Always review your form at least once for any possible errors before submitting it.

Documents used along the form

When tackling taxes, especially for business-related income in New Jersey, the NJ 1040 Schedule NJ-BUS-1 form plays a pivotal role in summarizing your business income on your personal tax return. However, this form does not stand alone. To complete your taxes accurately, additional documents are often required to provide a comprehensive view of your financial situation. Here's an overview of other essential forms and documents often used alongside the NJ 1040 Schedule NJ-BUS-1 form:

- Form NJ-1040: This is the New Jersey Individual Income Tax Return form. It's where you finalize your total income, deductions, and tax credits to calculate your tax liability or refund for the state. The Schedule NJ-BUS-1 is actually a part of this larger form, contributing detailed information about business profits or losses.

- Schedule NJ-K-1: Used by individuals who are part of a partnership or S corporation, this form details the distributive share of partnership income, deductions, and credits. Information from Schedule NJ-K-1 helps fill parts of the NJ-BUS-1 and the main NJ-1040 form, especially for those involved in partnerships or S corporations.

- Form NJ-CBT-100S: This document is the New Jersey S Corporation Business Tax Return form. It's crucial for S corporations operating in New Jersey as it outlines the corporation's income, gains, losses, deductions, and credits. While primarily for the corporation, information from NJ-CBT-100S is needed for individual shareholders to accurately complete their Schedule NJ-BUS-1 and NJ-K-1 forms.

- Form 1099-MISC: For individuals who are self-employed or have income from rents, royalties, or other non-employee compensation, the Form 1099-MISC is key. It reports income received from various sources not related to employment. Information from this form helps fill out the NJ-BUS-1, particularly in the sections covering rent, royalty, and other income.

Successfully navigating the complexities of New Jersey's tax system requires attention to detail and an understanding of how these forms and documents interconnect. Each piece of information helps illuminate your financial picture, ensuring compliance and potentially optimizing your tax situation. Whether you're self-employed, a partner, or a shareholder in an S corporation, coordinating these documents is essential for an accurate and complete tax return.

Similar forms

The NJ 1040 Schedule NJ-BUS-1 form, primarily focused on various types of business income, shares similarities with other tax forms that cater to different facets of income and financial activities. Among these, the IRS Schedule C (Form 1040) stands out. This form is designed for sole proprietors to report the income and expenses of their business, allowing them to calculate the net profit or loss for the year. Just like Schedule NJ-BUS-1 emphasizes the net profits from business by listing business names alongside profits or losses, Schedule C offers a comprehensive breakdown of business activities to evaluate the net business income accurately subject to federal taxation.

Another counterpart is the IRS Schedule E (Form 1040), which is utilized for reporting income or loss from rental real estate, royalties, partnerships, S corporations, estates, and trusts. The similarity to Schedule NJ-BUS-1 lies in the provision for declaring distributive share income from partnerships and S corporations, and net gains or income from rents, royalties, patents, and copyrights. While Schedule NJ-BUS-1 sums these incomes for state tax purposes, Schedule E focuses on how these sources contribute to an individual's income according to federal tax laws.

The IRS Schedule K-1 (Form 1065) is pivotal for partners in a partnership, as it details each partner's share of the partnership's profits, losses, deductions, and credits. This mirrors the PART II of Schedule NJ-BUS-1, which deals with distributive share of partnership income. Both documents ensure that income from partnerships is reported accurately for tax purposes, albeit Schedule K-1 is more specific to the partnership's reporting requirements at the federal level.

Similarly, the Schedule K-1 (Form 1120S) is used by shareholders of S corporations to report their pro-rata share of the corporation's income, deductions, and credits. This is akin to PART III of the NJ-BUS-1 schedule, where S corporation income is detailed. Both forms play a crucial role in ensuring that income from S corporations is correctly reported and taxed both at the state (for NJ-BUS-1) and federal levels (for Schedule K-1 1120S).

The IRS Form 8825, relevant for rental real estate activities conducted by partnerships or S corporations, also shares parallels with Schedule NJ-BUS-1. While Form 8825 is used to report income and expenses associated with rental real estate specifically, PART IV of NJ-BUS-1 encompasses a broader set of income sources, including rents. Their commonality rests in the mechanism of reporting rental income to accurately determine taxable income stemming from real estate operations.

For individuals invested in creative works, the IRS Schedule E section for royalties, patents, and copyrights mirrors the similar provision in Schedule NJ-BUS-1 PART IV. Both forms account for income derived from intellectual property, ensuring this niche area of income generation is included in an individual's overall tax obligations. However, Schedule NJ-BUS-1 consolidates these sources with other business income types for state tax purposes, while Schedule E addresses it within the broader context of supplemental income at the federal level.

Finally, Form 5695, which is used for residential energy credits, indirectly correlates with the essence of reporting specific income types or deductions on Schedule NJ-BUS-1. Although Form 5695 is tailored towards energy credits, the principle of delineating specific financial movements for tax benefits runs parallel to how NJ-BUS-1 sections are divided by income types. Both forms reflect the broader principle of tax accounting: categorizing financial activities for a transparent calculation of tax liabilities or benefits.

Dos and Don'ts

When it comes to filling out the NJ 1040 Schedule NJ-BUS-1 form, accuracy and attention to detail are crucial. Below are some guidelines to help ensure the process is done correctly and efficiently.

- Do follow instructions carefully. The form provides specific guidelines for each section, which can help in accurately reporting business income.

- Do accurately report your Social Security Number or Federal Employer Identification Number (EIN) where required. This information is crucial for identification and must be correct.

- Do list all sources of business income or losses. Transparency is key to properly filling out this form and avoiding any discrepancies with the Internal Revenue Service.

- Do ensure that the profit or loss is accurately calculated and reported for each business or source of income listed. This includes double-checking your math and ensuring that all figures are correctly entered.

- Don't leave any required fields blank. If a section does not apply, it is better to enter "0" or "N/A" rather than leaving it empty, unless instructions specifically direct otherwise.

- Don't enter losses on Line 17 or Line 20 if they are not allowed. Follow the form's instructions carefully to understand when and how losses should be reported.

- Don't forget to list the type of property and source of income for rents, royalties, patents, and copyrights in Part IV. Providing complete information is necessary for accurate processing.

- Don't overlook the final check of the form before submission. Errors or omissions can lead to processing delays or unnecessary queries from the Department of Taxation.

By following these guidelines, individuals can ensure a smoother and more accurate process when reporting business income on the NJ 1040 Schedule NJ-BUS-1 form. Always remember, when in doubt, referring back to the form's instructions or seeking professional advice can help clarify any uncertainties.

Misconceptions

When it comes to the NJ 1040 Schedule NJ-BUS-1 form, several misconceptions can lead to confusion. Understanding these misconceptions can help ensure accurate completion and submission of the form:

- Misconception 1: Only traditional businesses need to file this form. In reality, any individual earning income from business activities in New Jersey, including freelancers and independent contractors, should complete it.

- Misconception 2: All parts of the NJ-BUS-1 form must be filled out by every filer. Actually, you should only complete the sections that apply to your specific types of business income—whether that's net profits from a business, distributive share of partnership income, net pro rata share of S corporation income, or income from rents, royalties, patents, and copyrights.

- Misconception 3: Losses should always be entered on the form. In contrast, if your business incurs a loss, you make no entry on the line totals for Parts I, II, and III where indicated.

- Misconception 4: The NJ-BUS-1 form is a separate tax return. It's actually a schedule that supplements your NJ-1040 form, summarizing your business income for state tax purposes.

- Misconception 5: Personal and business social security numbers are interchangeable on this form. You must use your personal social security number for identification and may need to enter a federal Employer Identification Number (EIN) for your business where required.

- Misconception 6: Profit or loss from business should be estimated if exact figures are not available. You are required to use exact amounts from your financial records to ensure accurate tax reporting and compliance.

- Misconception 7: Income from all sources can be lumped together. This form separates income by source (e.g., business profits, partnership income, S corporation shares, and income from rents or royalties) to accurately assess tax obligations.

- Misconception 8: You do not need to list the physical address of rental real estate properties. For rental income, the specific physical address of each property must be disclosed to accurately associate income with New Jersey property locations.

- Misconception 9: You can file the NJ-BUS-1 form independently of the NJ-1040 form. This schedule must be submitted as part of your NJ-1040 tax return package and cannot be filed separately.

- Misconception 10: Electronic filing is not an option for the NJ-BUS-1 form. You can and are encouraged to file this form electronically along with your NJ-1040 for faster processing and record-keeping convenience.

By addressing these misconceptions, taxpayers can better navigate the process of reporting their business income on the NJ 1040 Schedule NJ-BUS-1 form, leading to a smoother tax filing experience.

Key takeaways

Understanding how to correctly fill out and use the NJ 1040 Schedule NJ-BUS-1 form is crucial for New Jersey taxpayers who have earned income from business activities. Here are six key takeaways that can help ensure the process is handled accurately:

- Identification is paramount: The top section of the form requires your name(s) as it appears on Form NJ-1040 and your Social Security Number. This information must be accurate to ensure your business income is correctly matched to your tax records.

- Detail your net profits from business: Part I of the form is where you list the net profit (or loss) your business(es) have generated. You must include the business name, Social Security Number/Federal EIN, and the profit or (loss). Make sure you calculate this accurately, as it affects your taxable income.

- Including partnership income: If you have income from partnerships, Part II asks for the distributive share of income (or loss). This part is essential for accurately reporting income from partnerships and ensuring it aligns with reported federal income.

- Reporting S Corporation income: For those involved with S corporations, Part III requires your pro rata share of income (or loss). This section is critical for S corporation shareholders to report their income correctly under New Jersey’s tax laws.

- Income from rents, royalties, patents, and copyrights: Part IV provides space to list net gains or income from these sources. Specific instructions regarding the type of property and the source of income or loss are important for accurate reporting and to avoid common mistakes such as misclassification of income types.

- Summarization: The form requires you to calculate and enter your total net profit or (loss) from various income sources at the end of each section. These figures must then be reported on your main NJ-1040 form. Accurate summarization and transference of these totals are essential for the correct calculation of your tax liability or refund.

This form reflects the diverse sources of business income that an individual may have and underscores the importance of meticulous record-keeping and understanding the tax implications of business operations. By following these key takeaways, a taxpayer can navigate the complexities of reporting business income in New Jersey more effectively.

Popular PDF Documents

Njcaa Ejection - Submission requirements emphasize timeliness and accuracy, with a noon local time deadline on the first business day post-ejection.

What Does Getting Fingerprinted Mean - The miscellaneous section, including codes like REBSL, is clarified for those in the real estate field preparing for fingerprinting.

1040 Vs 1040ez - Encouragement for organ and tissue donor awareness through this form signifies the state's investment in life-saving initiatives.