Fill Out a Valid Nj 1065E Template

The complexities of New Jersey's tax obligations and exemptions for nonresident entities are detailed within the NJ-1065E form, a crucial document for those managing such corporations. This form helps nonresident partners declare that their corporation is exempt from the Corporation Business Tax Act pursuant to N.J.S.A. 54:10A-3 or maintains a regular place of business within New Jersey, other than a mere statutory office. Having a so-called regular business space involves more than merely owning or renting an office; it requires that the space is actively used in the corporation's business operations, staffed by one or more employees. Failure to properly declare a New Jersey-based office can lead to the partnership being responsible for tax on the income attributable to the non-compliant partner. Furthermore, the NJ-1065E form outlines the annual necessity of this declaration and the strict deadline for its submission – no later than the 15th day of the fourth month following the close of the privilege period, or before the return is filed, whichever comes first. This introduction to the form highlights not just its technical details but also its broader implications for nonresident corporations operating in New Jersey, illustrating both the administrative responsibilities and potential financial obligations entailed.

Sample - Nj 1065E Form

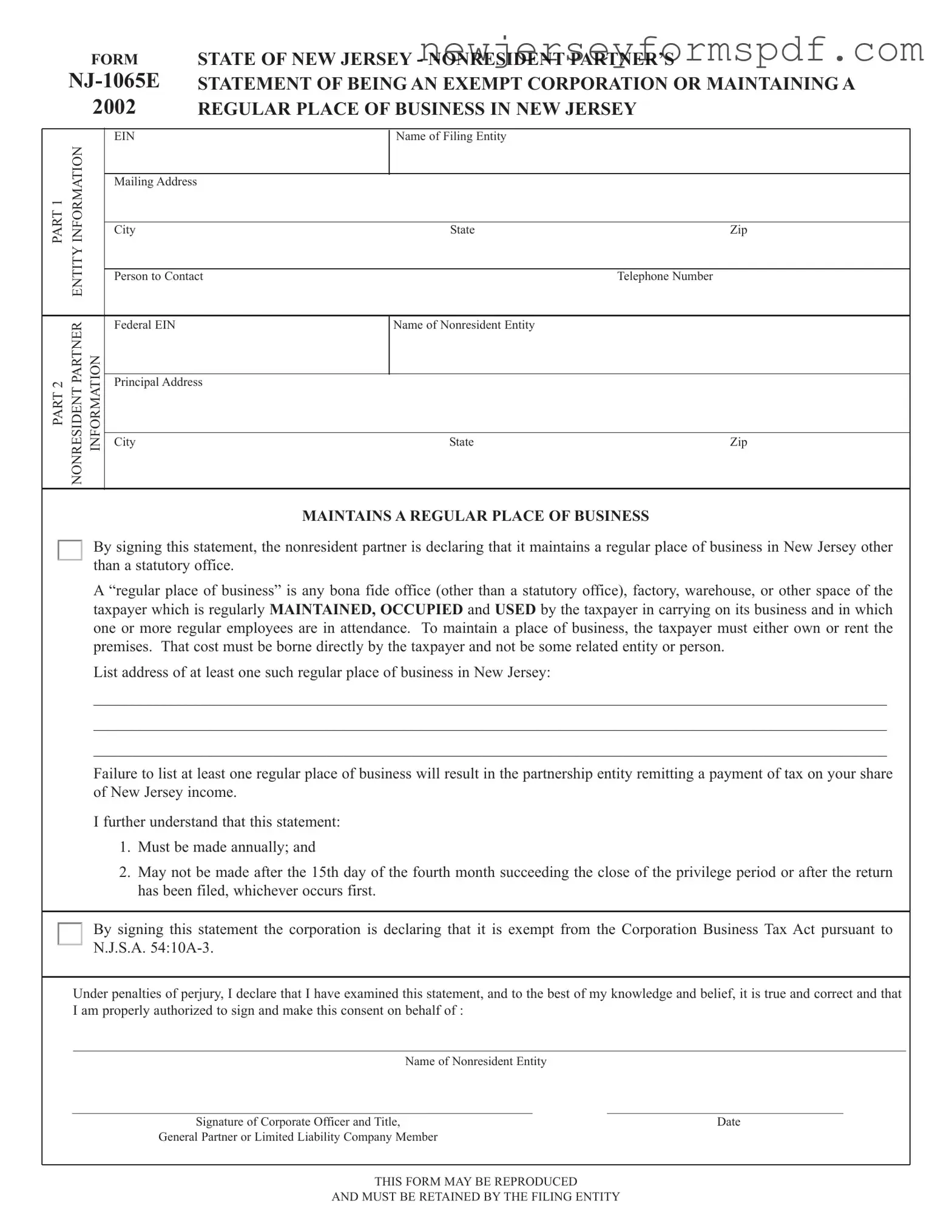

FORM

2002

STATE OF NEW JERSEY - NONRESIDENT PARTNER’S

STATEMENT OF BEING AN EXEMPT CORPORATION OR MAINTAINING A REGULAR PLACE OF BUSINESS IN NEW JERSEY

PART 1 |

INFORMATION |

|

|

ENTITY |

|

PART 2 |

NONRESIDENT PARTNER |

INFORMATION |

EIN

Mailing Address

City

Person to Contact

Federal EIN

Principal Address

City

Name of Filing Entity

State |

Zip |

Telephone Number

Name of Nonresident Entity

State |

Zip |

MAINTAINS A REGULAR PLACE OF BUSINESS

By signing this statement, the nonresident partner is declaring that it maintains a regular place of business in New Jersey other than a statutory office.

A “regular place of business” is any bona fide office (other than a statutory office), factory, warehouse, or other space of the taxpayer which is regularly MAINTAINED, OCCUPIED and USED by the taxpayer in carrying on its business and in which one or more regular employees are in attendance. To maintain a place of business, the taxpayer must either own or rent the premises. That cost must be borne directly by the taxpayer and not be some related entity or person.

List address of at least one such regular place of business in New Jersey:

______________________________________________________________________________________________________

______________________________________________________________________________________________________

______________________________________________________________________________________________________

Failure to list at least one regular place of business will result in the partnership entity remitting a payment of tax on your share of New Jersey income.

I further understand that this statement:

1.Must be made annually; and

2.May not be made after the 15th day of the fourth month succeeding the close of the privilege period or after the return has been filed, whichever occurs first.

By signing this statement the corporation is declaring that it is exempt from the Corporation Business Tax Act pursuant to N.J.S.A.

Under penalties of perjury, I declare that I have examined this statement, and to the best of my knowledge and belief, it is true and correct and that I am properly authorized to sign and make this consent on behalf of :

_______________________________________________________________________________________________________________________

Name of Nonresident Entity |

|

__________________________________________________________________________ |

______________________________________ |

Signature of Corporate Officer and Title, |

Date |

General Partner or Limited Liability Company Member |

|

|

|

THIS FORM MAY BE REPRODUCED |

|

AND MUST BE RETAINED BY THE FILING ENTITY

REVISED STATUTES OF NEW JERSEY, 1937, TITLE 54 TAXATION, SUBTITLE 4 PARTICULAR TAXES ON CORPORATIONS AND OTHERS, PART 1PROVISIONS APPLICABLE TO CORPORATIONS GENERALLY, Ch. 10A Corporation Business Tax Act (1945)

Sec.

The following corporations shall be exempt from the tax imposed by this act:

(a)Corporations subject to a tax assessed upon the basis of gross receipts, other than the alternative minimum assessment determined pursuant to section 7 of P.L.2002, c.40

(b)Corporations which operate regular route autobus service within this State under operating authority conferred pursuant to

(c)Railroad, canal corporations, production credit associations organized under the Farm Credit Act of 1933, or agricultural cooperative associations incorporated or domesticated under or subject to chapter 13 of Title 4 of the Revised Statutes and exempt under Subtitle A, Chapter 1F, Part IV, Section 521 of the federal Internal Revenue Code (26 U.S.C. s.521);

(d)Cemetery corporations not conducted for pecuniary profit or any private shareholder or individual;

(e)Nonprofit corporations, associations or organizations established, organized or chartered, without capital stock, under the provisions of Title 15, 16 or 17 of the Revised Statutes, Title 15A of the New Jersey Statutes or under a special charter or under any similar general or special law of this or any other state, and not conducted for pecuniary profit of any private shareholders or individual;

(f)Sewerage and water corporations subject to a tax under the provisions of P.L.1940, c.5

(g)Nonstock corporations organized under the laws of this State or of any other state of the United States to provide mutual ownership housing under federal law by tenants, provided, however, that the exemption hereunder shall continue only so long as the corporations remain subject to rules and regulations of the Federal Housing Authority and the Commissioner of the Federal Housing Authority holds membership certificates in the corporations and the corporate property is encumbered by a mortgage deed or deed of trust insured under the National Housing Act (48 Stat.1246) as amended by subsequent Acts of Congress. In order to be exempted under this subsection, corporations shall annually file a report on or before August 15 with the commissioner, in the form required by the commissioner, to claim such exemption, and shall pay a filing fee of $25.00;

(h)Corporations not for profit organized under any law of this State where the primary purpose thereof is to provide for its shareholders or members housing in a retirement community as the same is defined under the provisions of the "Retirement Community Full Disclosure Act," P.L.1969, c.215

(i)Corporations which are licensed as insurance companies under the laws of another state, including corporations which are surplus lines insurers declared eligible by the Commissioner of Banking and Insurance pursuant to section 11 of P.L.1960, c.32 (C.17:22- 6.45) to insure risks within this State; and

(j)(1) Municipal electric corporations that were in existence as of January 1, 1995 provided that all of their income is from sales, exchanges or deliveries of electricity derived from customers using electricity within their municipal boundaries; and (2) Municipal electric utilities that were in existence as of January 1, 1995 provided that all of their income is from sales, exchanges or deliveries of electricity derived from customers using electricity within their franchise area existing as of January 1, 1995. If a municipal electric corporation derives income from sales, exchanges or deliveries of electricity from customers using the electricity outside its municipal boundaries, such municipal electric corporation shall be subject to the tax imposed by this act on all income. If a municipal electric utility derives income from sales, exchanges or deliveries of electricity from customers using electricity outside its franchise area existing as of January 1, 1995, such municipal electric utility shall be subject to the tax imposed by the act on all income.

(As amended by Ch. 236, Laws 1949; Ch. 130, Laws 1951; Ch. 174, Laws 1960; Ch. 59, Laws 1963; Ch. 48, Laws 1967; Ch. 211, Laws 1972; Ch. 275, Laws 1973; Ch. 170, Laws 1975; Ch. 184, Laws 1991; Ch. 338, Laws 1993; Ch. 162, Laws 1997; Ch. 114 (A.B. 262), Laws 1998; Ch. 40 (A. B. 2501), Laws 2002, applicable to privilege periods and taxable years beginning on or after January 1, 2002.

Document Specifications

| Fact | Detail |

|---|---|

| Form Title | FORM NJ-1065E 2002 STATE OF NEW JERSEY - NONRESIDENT PARTNER’S STATEMENT OF BEING AN EXEMPT CORPORATION OR MAINTAINING A REGULAR PLACE OF BUSINESS IN NEW JERSEY |

| Purpose | Allows nonresident partners to declare either exemption from Corporation Business Tax or maintenance of a regular business place in New Jersey. |

| Regular Place of Business Requirement | A bona fide office, factory, warehouse, or space in New Jersey that is regularly maintained, occupied, and used in business operations with at least one regular in-house employee. |

| Ownership or Rental of Premises | The taxpayer must own or rent the premises, bearing the cost directly. |

| Failure to List a Business Place | Results in the partnership entity remitting payment of tax on the nonresident's share of New Jersey income. |

| Annual Declaration Requirement | The statement must be made annually by the nonresident partner. |

| Declaration Deadline | Cannot be made after the 15th day of the fourth month following the close of the privilege period or after the return has been filed, whichever occurs first. |

| Exemption under Corporation Business Tax Act | Declaration that the corporation is exempt pursuant to specific criteria outlined in N.J.S.A. 54:10A-3. |

| Governing Law | The form is governed by the REVISED STATUTES OF NEW JERSEY, 1937, TITLE 54 TAXATION, SUBTITLE 4 PARTICULAR TAXES ON CORPORATIONS AND OTHERS, PART 1, Ch. 10A Corporation Business Tax Act (1945) Sec. 54:10A-3. |

Detailed Steps for Using Nj 1065E

Filing the NJ-1065E form is an essential task for certain nonresident partners and entities operating within New Jersey. This form serves as a declaration by nonresident partners that they are either exempt from the Corporation Business Tax Act pursuant to specific sections of the N.J.S.A. 54:10A-3 or that they maintain a regular place of business in New Jersey outside of just a statutory office. Ensuring accurate and timely completion of this form is crucial, as it impacts the partnership's obligations and the partner's tax liability in New Jersey. Follow these detailed steps to fill out the NJ-1065E form properly.

- Begin with Part 1 - Information of Filing Entity. Enter the Name of Filing Entity, Economic Identification Number (EIN), and the mailing address, including city, state, and zip code. Also, provide a principal address if different from the mailing address and the name and telephone number of a person to contact regarding the form.

- Proceed to Part 2 - Nonresident Partner Information. Input the Name of Nonresident Entity and its State of registration. Fill in the Federal Employer Identification Number (EIN) and the registered office's address, including street, city, state, and zip code.

- Under the section titled "MAINTAINS A REGULAR PLACE OF BUSINESS", if applicable, declare that the nonresident partner maintains a regular place of business in New Jersey that is not merely a statutory office. This place must be a bona fide office, factory, warehouse, or other spaces regularly maintained, occupied, and used in conducting its business, where one or more regular employees work. List at least one such New Jersey business address completely.

- Comprehend the section highlighting that failure to list at least one regular place of business will result in the partnership remitting payment of tax on your share of New Jersey income. Acknowledge the statement needs to be made annually and cannot be made after the 15th day of the fourth month following the close of the privilege period or after the return has been filed, whichever comes first.

- Review the certification statement emphasizing the declaration made by the nonresident partner to be exempt from the Corporation Business Tax Act according to specified exemptions listed in N.J.S.A. 54:10A-3.

- Complete the bottom section by printing the name of the Nonresident Entity again. Then, a corporate officer, general partner, or limited liability company member authorized to sign on behalf of the nonresident partner must sign, provide their title, and date the form.

Once the form is completed and signed, it should be retained by the filing entity as required. The completion of the NJ-1065E form is a critical step for nonresident partners to comply with New Jersey taxation laws, ensuring their operations are recognized as compliant and potentially avoiding unnecessary tax implications. It is advisable to consult with a tax professional to ensure proper completion and submission of this form.

Learn More on Nj 1065E

What is Form NJ-1065E?

Form NJ-1065E is a document used by nonresident partners in New Jersey to declare their exemption from the Corporation Business Tax Act. This is applicable either because they are part of an exempt corporation or they maintain a regular place of business in New Jersey that is not merely a statutory office.

Who needs to file Form NJ-1065E?

Nonresident partners of partnerships operating in New Jersey who want to claim an exemption from the Corporation Business Tax need to file this form. This includes those who are exempt under specific statutes or those who have a bona fide office or business space in New Jersey.

What constitutes a "regular place of business" for Form NJ-1065E?

A "regular place of business" includes any bona fide office, factory, warehouse, or other space which is:

- Regularly maintained, occupied, and used by the taxpayer in carrying on its business

- Manned by one or more regular employees in attendance

- Owned or rented directly by the taxpayer, with the cost borne by them and not by a related entity or person

What are the consequences of not listing at least one regular place of business in New Jersey on Form NJ-1065E?

Failing to list at least one regular place of business in New Jersey will result in the partnership being required to remit payment of tax on the nonresident partner's share of New Jersey income.

When is Form NJ-1065E due?

The form must be filed annually. It cannot be filed after the 15th day of the fourth month following the close of the privilege period or after the return has been filed, whichever occurs first.

What are the exemptions from the Corporation Business Tax Act?

Entities exempt from the Corporation Business Tax Act include, but are not limited to:

- Corporations taxed on gross receipts or insurance premiums

- Railroad and canal corporations

- Non-profit organizations not conducted for profit of any private shareholders or individuals

- Agricultural cooperative associations

- Cemetery corporations not conducted for pecuniary profit

- Sewerage and water corporations

- Nonstock corporations providing mutual ownership housing under federal law

- Retirement community housing corporations

- Insurance companies licensed under laws of another state

- Municipal electric corporations and utilities in existence as of January 1, 1995

How can one declare a nonresident entity as an exempt corporation?

By signing the Form NJ-1065E, the corporate officer or partner is declaring, under penalty of perjury, that the nonresident entity is exempt from the Corporation Business Tax Act based on the outlined exemptions.

Do I need to renew my exemption status annually with Form NJ-1065E?

Yes, the exemption status claimed through Form NJ-1065E must be declared annually to ensure compliance with New Jersey's tax laws.

Where should I list my regular place of business on Form NJ-1065E?

The address of at least one regular place of business in New Jersey should be clearly listed in the specified section of Form NJ-1065E to comply with its conditions for claiming exemption.

What information is required on Form NJ-1065E?

The form requires specific details about the filing entity, including:

- The name and contact details of the filing entity and nonresident partner

- The entity and personal Federal EIN

- Principal and mailing addresses

- Signatures from an authorized corporate officer, general partner, or LLC member

Common mistakes

Filling out the NJ-1065E form, a crucial document for nonresident partners declaring their business presence in New Jersey, requires careful attention. Unfortunately, mistakes are common and can lead to complications or even penalties. Here are eight common errors to avoid to ensure the process is as smooth as possible:

- Not listing a physical business address in New Jersey. The form explicitly requires the specification of at least one genuine business location within the state. Failure to do so can result in the partnership being taxed on your share of New Jersey income.

- Omitting the signature of a corporate officer or authorized individual. The statement must be signed by someone with the proper authority to make declarations on behalf of the entity. An unsigned form is not valid.

- Incorrectly filling out contact information. Providing incorrect or incomplete mailing addresses, telephone numbers, or other contact details can lead to missed communications.

- Failing to annually update the statement. The declaration that a nonresident partner maintains a regular business place in New Jersey is not a one-time affair. It must be updated annually, a requirement that is often overlooked.

- Filling out the form after the deadline. Submissions must be made before the 15th day of the fourth month following the close of the privilege period or after the return has been filed, whichever comes first. Late submissions are a common mistake.

- Inaccurate or incomplete description of the business location. Vaguely listing a business address or providing incomplete details can result in your submission being questioned or rejected.

- Failure to claim exemption properly. For entities that are exempt from the Corporation Business Tax Act, there’s a specific section to declare this status. Mistakes in claiming this exemption, such as failing to provide sufficient supporting information or misunderstanding eligibility, are frequent missteps.

- Not retaining a copy for your records. The form clearly states it may be reproduced and must be retained by the filing entity. Neglecting to keep a copy can lead to issues if the submitted information is later questioned.

Avoiding these mistakes not only prevents delays but also ensures compliance with New Jersey’s tax laws. Taking care when filling out the NJ-1065E form is crucial for nonresident entities operating within the state. By being diligent and verifying all the information before submission, you can navigate this process more seamlessly and avoid potential issues with state authorities.

Documents used along the form

When preparing or reviewing the New Jersey Form NJ-1065E, several other forms and documents are often used in conjunction to ensure compliance with state tax obligations and regulatory requirements. Below is a list of these supplementary forms and documents, providing a comprehensive toolkit for businesses and practitioners navigating the complexities of New Jersey's tax law and business environment.

- NJ-1065: This is the Partnership Return Form. It is utilized by partnerships to report their income, deductions, and credits to the State of New Jersey. The NJ-1065E serves as an attachment to this form for nonresident partners claiming exemption.

- NJ-CBT-1065: New Jersey Partnership Tax Payment Form. It outlines the income tax payment that must be submitted on behalf of all nonresident partners, unless exemption criteria are met as outlined in the NJ-1065E form.

- NJ-REG: This form is necessary for business registration in New Jersey. It covers business entities of all types, including partnerships needing to establish or update their business and tax records with the state.

- Schedule NJ-K-1: This document provides detailed information about each partner's share of partnership income, deductions, and credits. It's instrumental for partners in preparing their individual New Jersey income tax returns.

- NJ-1040NR: Nonresident Income Tax Return Form. Nonresident individuals who receive income from a New Jersey source, including partnerships, use this form to report and pay their state income tax.

- Certificate of Authority: This legal document authorizes out-of-state corporations to do business in New Jersey. Companies that meet the NJ-1065E exemption criteria by maintaining a regular business location in New Jersey may need this certification.

Together, these forms create a framework that supports compliance with state tax laws, ensuring proper reporting and payment of taxes by partnerships and their members. It's crucial for entities engaged in business within New Jersey to familiarize themselves with these documents, as they provide the structure for tax responsibilities, exemptions, and filings specific to partnerships and their nonresident partners.

Similar forms

The Form 1040NR, used by nonresident aliens to file U.S. tax returns, bears a similarity to the NJ 1065E in that both are designed for nonresidents conducting activities within a jurisdiction. While the NJ 1065E pertains specifically to nonresident entities in New Jersey claiming an exemption or maintaining a business presence, the 1040NR addresses individual income tax responsibilities on a federal level. Each form requires detailed entity or individual information, and sternly emphasizes the importance of accurate reporting under the penalty of perjury.

The Form 1120, the U.S. Corporation Income Tax Return, is akin to the NJ 1065E in its function of reporting to tax authorities. Specifically, the Form 1120 is used by corporations to declare their income, gains, losses, deductions, and credits to the Internal Revenue Service (IRS). Similar to the NJ 1065E, which exempts specific nonresident entities from the Corporation Business Tax, the Form 1120 requires corporations to disclose comprehensive operational details and calculate their tax liability or exemptions based on federal laws.

Similar to the NJ 1065E, the Form 1065, U.S. Return of Partnership Income, serves partnerships operating within the U.S. It requires detailed reporting of income, financial transactions, and operational entity specifics. Both forms play crucial roles in ensuring partnerships and nonresident entities comply with their respective tax obligations, though the 1065 focuses on federal partnership reporting while the NJ 1065E targets nonresident partners operating in New Jersey and their specific state exemptions.

The Form NJ-REG, needed to register a business in New Jersey for tax and employer purposes, shares objectives with the NJ 1065E by gathering entity information to meet state regulatory and tax requirements. Whereas the NJ-REG is the first step in acknowledging and establishing a business’s presence for state tax liabilities, the NJ 1065E further delineates the status of nonresident entities and their operation scope within the state, highlighting their exemptions and commitments.

Resembling the NJ 1065E, Schedule NJ-NR-A serves a related purpose for nonresident taxpayers in declaring income from New Jersey sources. This schedule is often a requisite for nonresidents who need to report and calculate their New Jersey income taxes. Both documents are integral to New Jersey’s tax structure, specifically addressing nonresident participation and ensuring equitable tax contributions based on state-sourced income.

The UBTI (Unrelated Business Taxable Income) Form 990-T is used by exempt organizations to report and pay income tax on unrelated business income. While it serves a different taxpayer base, this form shares the NJ 1065E's objective of identifying exemptions and taxable income within a specific framework. Both forms require detailed entity and financial information to assess tax obligations related to operational activities distinctly categorized by legal stipulations.

The Form 5472, Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business, parallels the NJ 1065E in targeting entities with specific international ties and business practices within the jurisdiction. Like the NJ 1065E, emphasizing the need for transparency and accuracy, Form 5472 collects data on the transactions between the U.S. businesses and their foreign affiliates, ensuring compliance with U.S. taxation laws and regulations.

Finally, the Application for Employer Identification Number (EIN), Form SS-4, shares a procedural step with the NJ 1065E in the realm of business operations and tax reporting. While Form SS-4’s primary purpose is to obtain an identifier for business entities within the United States, including those owned by nonresidents, the NJ 1065E uses this identifier for specific nonresident entities to claim exemptions or affirm their operational stance in New Jersey. Both are foundational to navigating the complexities of tax identity and obligations in the U.S.

Dos and Don'ts

When filling out the NJ 1065E form, it’s crucial to follow specific guidelines to ensure accuracy and compliance. Below are things you should and shouldn’t do:

- Do thoroughly read the instructions before beginning to fill out the form. This ensures you understand the requirements.

- Do ensure that the name of the nonresident entity is correctly and consistently written throughout the form.

- Do verify the accuracy of the Employer Identification Number (EIN) before submitting the form.

- Do list at least one regular place of business in New Jersey, if applicable, including the complete address.

- Do sign and date the form, as it is a declaration under the penalties of perjury. Make sure an authorized corporate officer, general partner, or limited liability company member provides the signature.

- Do not leave mandatory fields blank. Incomplete forms may lead to processing delays or rejection.

- Do not list a statutory office as a regular place of business. Only bona fide operational locations should be listed.

- Do not miss the filing deadline. The form must be made annually and no later than the 15th day of the fourth month following the close of the privilege period, or after the return has been filed, whichever occurs first.

- Do not fabricate or alter information on the form. Providing false information can result in penalties.

Misconceptions

There are several misconceptions about the NJ-1065E form and understanding the facts can help clarify its purpose and requirements. Here are ten common misunderstandings:

- Only for Individual Partners: It's a misconception that the NJ-1065E form is solely for individual partners. In reality, it applies to nonresident entities acting as partners in a partnership. These entities must declare their presence in New Jersey through a regular place of business or their exemption status.

- Filing Deadlines Are Flexible: Many believe that the filing deadlines for the NJ-1065E form are flexible. However, the declaration must be made annually and can't be made after the 15th day of the fourth month following the close of the privilege period, or after the entity’s return has been filed; whichever situation comes first.

- Ownership of Premises Is Necessary: A common misconception is that to maintain a "regular place of business" in New Jersey, the entity must own the premises. The truth is, the business can either own or rent the space, as long as the cost is borne directly by the entity, not by a related party.

- Applies to All Business Entities: Some think that the NJ-1065E form applies to all business entities. It specifically concerns nonresident entities that are partners in a partnership needing to declare their regular business place or exemption status in New Jersey.

- Only For Profit Entities Must File: There's a misconception that only for-profit entities must file this form. Exempt organizations under specific conditions also need to declare their exemption annually through the NJ-1065E.

- Signature Requirements Are Lax: The assumption that just anyone from the entity can sign the NJ-1065E form is incorrect. The statement must be signed by a duly authorized corporate officer, general partner, or LLC member, affirming under penalties of perjury that the provided information is accurate.

- No Need for Employee Attendance at Business Places: It's incorrectly assumed that for a location to be considered a regular place of business, there's no need for regular employee attendance. The definition explicitly requires one or more regular employees to be in attendance at the space.

- A Single Declaration Is Sufficient for Multiple Entities: Some believe that if one entity in a partnership files the NJ-1065E, it covers all nonresident entities within the partnership. Each nonresident entity must separately declare its physical presence or exemption status.

- No Consequences for Failure to Declare: There's a misconception that failing to list at least one regular place of business has no financial consequences for the nonresident partner. In reality, not doing so will result in the partnership being taxed on the partner's share of New Jersey income.

- Statutory Offices Qualify as Regular Business Places: A common misunderstanding is that a statutory office can be listed as a regular place of business on the form. The form specifies that a statutory office does not qualify and a bona fide office, factory, warehouse, or other space regularly maintained, occupied, and used by the taxpayer must be listed.

By addressing these misconceptions, nonresident entities can ensure they correctly understand and comply with the requirements of the NJ-1065E form, avoiding potential pitfalls and penalties.

Key takeaways

- The NJ-1065E form is an important document for nonresident partners in New Jersey, verifying that they maintain a regular place of business in the state outside of just a statutory office.

- By signing this form, the nonresident partner confirms that the regular place of business in New Jersey is genuinely used in the daily operations of the business, with at least one regular employee present.

- Ownership or rental of the premises where the business is conducted must be directly by the taxpayer, ensuring no third-party involvement in the business premises' costs.

- Partners must list at least one regular business address in New Jersey on the form. Failure to do so could lead to the partnership having to pay tax on the nonresident partner's share of New Jersey income.

- The statement on the form must be made annually and cannot be submitted after the 15th day of the fourth month following the close of the privilege period or after the return has been filed, whichever is earlier.

- Furthermore, the form indicates that by signing it under penalty of perjury, the signatory asserts the information is true and correct and declares eligibility for exemption under specific sections of the Corporation Business Tax Act as per N.J.S.A. 54:10A-3.

Popular PDF Documents

Subpoena Deuces Tecum - The form is part of a legal protocol to ensure that all relevant facts and materials are presented during a court case, contributing to a fair trial.

Nj Reg - The NJ-REG form is crucial for businesses engaging in the sale of regulated products, such as alcohol, tobacco, and gasoline in New Jersey.

Proof of Service Nj - Military service verification is streamlined through the U.S. Department of Defense or respective military branch inquiries for absent guardians in the service.