Fill Out a Valid Nj 1080E Template

In New Jersey, entities like general and limited partnerships, limited liability companies (LLCs), S corporations, estates, trusts, and professional athletic teams have the option to file a composite gross income tax return on behalf of their qualified nonresident members, partners, shareholders, or beneficiaries. This filing convenience is facilitated through the NJ-1080E form, which serves as an Election to Participate in a Composite Return by those qualified individuals who are nonresidents throughout the entire tax year, do not maintain a permanent residence in New Jersey, and derive their income solely from sources within the state. By signing this election, participants agree to several conditions, including waiving their right to personal exemptions, credits, or deductions, and having their income taxed at the highest rate for single taxpayers. Entities retaining these elections must make them available upon request by the Division of Taxation, and there are specific deadlines and liabilities associated with the submission of the NJ-1080E form. Additionally, the form mandates annual renewal, is binding on the signatory’s heirs and cannot be revoked once submitted by the specified deadline. This facilitative measure aims to streamline tax filing processes for nonresident individuals and the entities they are involved with, ensuring that tax liabilities are met efficiently and in compliance with New Jersey tax laws.

Sample - Nj 1080E Form

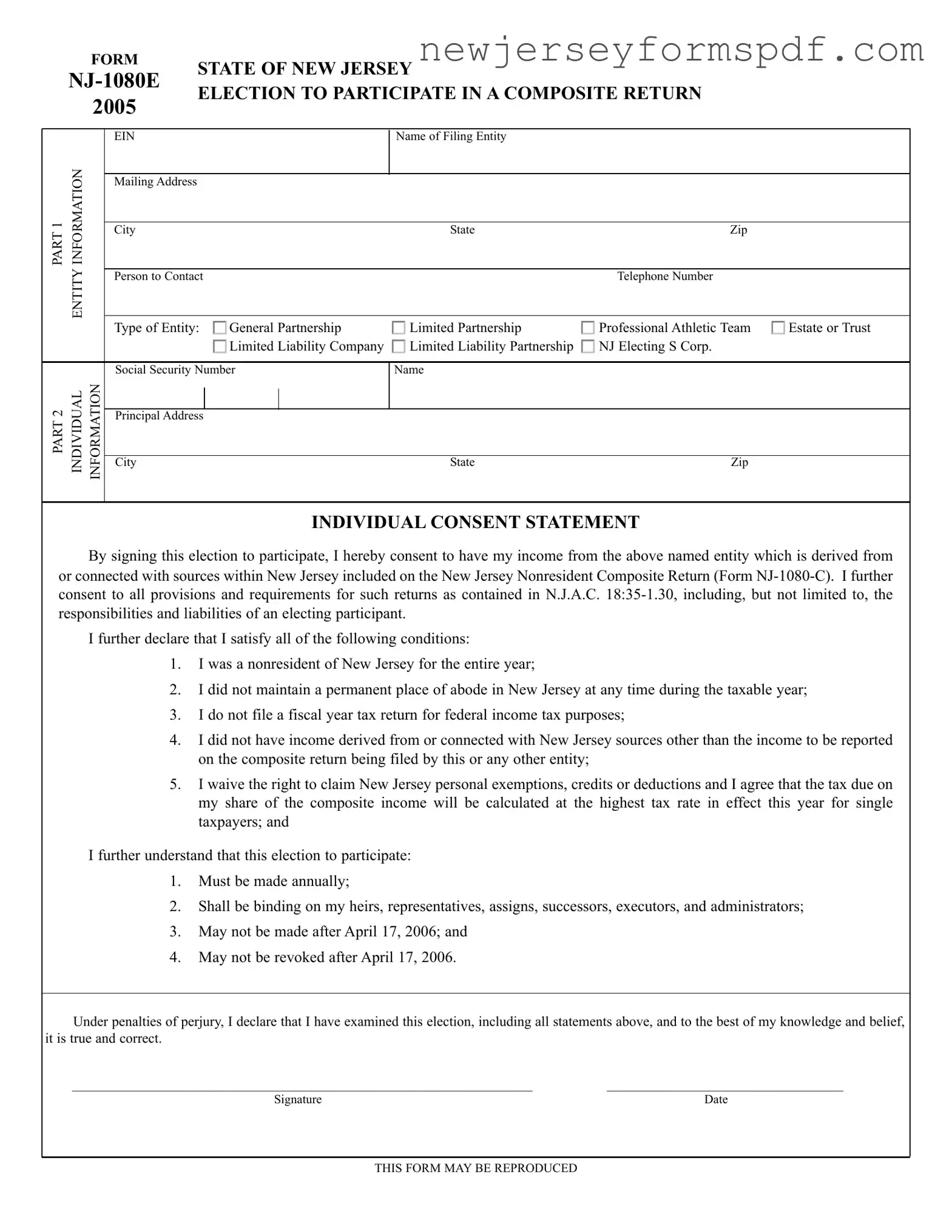

FORM STATE OF NEW JERSEY

2005

ELECTION TO PARTICIPATE IN A COMPOSITE RETURN

PART 1 |

INFORMATION |

|

ENTITY |

PART 2 |

INDIVIDUAL |

INFORMATION |

EIN |

Name of Filing Entity |

|

|

|

|

Mailing Address |

|

|

|

|

|

City |

State |

Zip |

|

|

|

Person to Contact |

|

Telephone Number |

Type of Entity: |

|

|

General Partnership |

|

|

Limited Partnership |

|

Professional Athletic Team |

|

Estate or Trust |

|

|

|

|

Limited Liability Company |

|

|

Limited Liability Partnership |

|

NJ Electing S Corp. |

|

|

|

|

|

|

|

|

|

|

|

||||

Social Security Number |

|

Name |

|

|

|

|

|||||

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Principal Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

|

|

State |

|

Zip |

|

|

INDIVIDUAL CONSENT STATEMENT

By signing this election to participate, I hereby consent to have my income from the above named entity which is derived from or connected with sources within New Jersey included on the New Jersey Nonresident Composite Return (Form

I further declare that I satisfy all of the following conditions:

1.I was a nonresident of New Jersey for the entire year;

2.I did not maintain a permanent place of abode in New Jersey at any time during the taxable year;

3.I do not file a fiscal year tax return for federal income tax purposes;

4.I did not have income derived from or connected with New Jersey sources other than the income to be reported on the composite return being filed by this or any other entity;

5.I waive the right to claim New Jersey personal exemptions, credits or deductions and I agree that the tax due on my share of the composite income will be calculated at the highest tax rate in effect this year for single taxpayers; and

I further understand that this election to participate:

1.Must be made annually;

2.Shall be binding on my heirs, representatives, assigns, successors, executors, and administrators;

3.May not be made after April 17, 2006; and

4.May not be revoked after April 17, 2006.

Under penalties of perjury, I declare that I have examined this election, including all statements above, and to the best of my knowledge and belief, it is true and correct.

__________________________________________________________________________ |

______________________________________ |

Signature |

Date |

THIS FORM MAY BE REPRODUCED

(a)A general partnership, a limited partnership, a limited liability partnership (LLP), a limited liability company (LLC), a New Jersey electing S corporation, an estate, a trust, or a professional athletic team (as defined in N.J.A.C. 18:35- 1.29) doing business or conducting activities in New Jersey or having income derived from or connected with sources within New Jersey may file a composite New Jersey Nonresident gross income tax return (Form

1. Any entity which files a composite return on behalf of its qualified nonresident individual members shall be referred to as the “filing entity”.

(b)A qualified nonresident individual is one who elects to participate in the composite return and satisfies all of the following conditions:

1. The individual was a nonresident for the entire taxable year;

2. The individual did not maintain a permanent place of abode in New Jersey at any time during the taxable year;

3. The individual was not a fiscal year filer;

4. The individual did not have income derived from or connected with New Jersey sources other than the income reported on this or any other composite return;

5. The individual waives the right to claim any New Jersey personal exemption, credit or deduction and agrees to have the tax calculated directly on such income at the highest tax rate in effect for single taxpayers for the tax year; and

6. The individual elects to be included in a composite return by completing and delivering to the filing entity a Form

i.Such election must be made annually;

ii.Such election shall be binding on the participant’s heirs, representatives, assigns, successors, executors and administrators;

iii.Such election shall be an express consent to personal jurisdiction in New Jersey for New Jersey personal income tax purposes; and

iv.A qualified electing nonresident participant may not revoke an election to be included in the composite return or make an election to be included in the composite return after April 15 following the close of the taxable year.

(c)Each filing entity must retain the completed and signed election forms (Form

(d)An individual may participate in more than one New Jersey gross income tax composite return, providing the requirements of subsections (b)1 through (b)6, above, are satisfied.

(e)Nonresident individuals who are not eligible to participate in the composite return because they do not satisfy all of the requirements of subsection (b), or who do not wish to participate in the composite return, must file a Form NJ- 1040NR reflecting their income from all sources, as well as from New Jersey sources.

(f)The composite return shall be due on the fifteenth day of the fourth month following the close of the taxable year of the qualified electing nonresident participants. An extension of time to file will be granted on a composite basis only and must be requested in accordance with N.J.A.C.

(g)If the filing entity has filed a composite return previously and the amount which the filing entity estimates to be the total income tax liability for the composite return for the current tax year exceeds $100, the filing entity must file a declaration of estimated tax and make quarterly estimated tax payments in accordance with N.J.S.A.

(h)The tax due shall be calculated using the highest gross income tax rate in effect for single taxpayers for the tax year for which the composite return is being filed, without benefit of personal exemptions, deductions or credits.

(i)The filing of a composite return shall be considered to be a group of separate returns meeting the individual filing requirements for each qualified electing nonresident participant as imposed by the Gross Income Tax Act. N.J.S.A

1.Each qualified electing nonresident participant is personally liable for the timely filing of returns and payment of such individual’s liability, including, but not limited to, any assessment resulting from an audit of the composite return.

2.Each qualified electing nonresident participant adopts the statements contained in the filed composite return relating to the filing entity and to him or herself (but not as to statements made on the composite return relating solely to other participants), and shall take, under penalties of perjury, full responsibility for the truth of the statements contained in the filed composite return.

3.Each qualified electing nonresident participant adopts, as his or her own, any actions of the filing entity that may affect the composite return, including, but not limited to, a waiver of the statute of limitations for assessment or any decision to accept the results of an audit by the Division.

4.The Director retains the right to require the filing of an individual New Jersey Nonresident Gross Income Tax Return (Form

(j)Each composite return shall include the following for each qualified electing nonresident participant:

1.Name and address;

2.Social Security Number;

3.The participant’s share of income derived from or connected with New Jersey sources;

4.The New Jersey gross income tax attributable to the participant’s share of income derived from or connected with New Jersey source; and

5.A copy of the following;

i.Schedule

ii.Schedule

iii.Schedule

iv.Form

(k)Each return must include the names, addresses, and social security numbers of all members of the filing entity who are not included in the composite return.

(l)Any composite return which is filed on behalf of 25 or more participants must be filed on diskette or by using magnetic media.

(m)The composite New Jersey Nonresident gross income tax return (Form

1.The tax matters partner, if the filing entity is a general partnership, a limited partnership, or a limited liability partnership;

2.An officer of the corporation, if the filing entity is an S corporation;

3.The executor or administrator, if the filing entity is an estate;

4.A trustee, if the filing entity is a trust; or

5.An authorized member, if the filing entity is a limited liability company.

6.If the filing entity is a professional athletic team the return must be signed as required in subsections 1 through 5 above, depending on the entity type of the team.

(n)If, after the final composite return has been filed, a qualified, electing, nonresident participant discovers income derived from or connected with New Jersey sources other than from the filing entity, such participant shall file a Nonresident New Jersey Gross Income Tax Return (Form

1.The participant’s Form

2.Such participant shall be entitled to a credit on the Form

(o)For members of general and limited partnerships and professional athletic teams this rule shall apply to all tax years beginning on or after January 1, 1995. For members of New Jersey electing S corporations, limited liability partnerships, limited liability companies, and estates and trusts this rule shall apply to all tax years beginning on or after January 1, 1996.

Document Specifications

| Fact Name | Description |

|---|---|

| Form Identification | The form is known as the NJ-1080E, pertaining to the 2005 election to participate in a composite return. |

| Purpose | It allows qualifying nonresident individuals of certain entities to elect inclusion on a New Jersey Nonresident Composite Return (Form NJ-1080-C). |

| Participants | General partnerships, limited partnerships, professional athletic teams, estates or trusts, limited liability companies (LLC), limited liability partnerships (LLP), and NJ Electing S Corps can file on behalf of qualified nonresident individuals. |

| Election Conditions | Participants must be nonresidents for the entire year, have no permanent abode in New Jersey during the year, not be fiscal year filers, have no income from NJ sources other than what's reported on the composite return, and waive the right to claim New Jersey personal exemptions, credits, or deductions. | \

| Annual Election | The election to participate must be made annually and cannot be made after April 17, 2006, for the year in question. |

| Binding Agreement | This election is binding on the participant’s heirs, representatives, assigns, successors, executors, and administrators and cannot be revoked after April 17, 2006. |

| Composite Return Filing Deadline | The composite return is due on the fifteenth day of the fourth month following the close of the taxable year. |

| Governing Law | The provisions and requirements for these returns are contained in N.J.A.C. 18:35-1.30, under the jurisdiction of New Jersey law. |

Detailed Steps for Using Nj 1080E

Filing the NJ-1080E form is an essential task for eligible nonresident individuals who want to be included in a New Jersey Nonresident Composite Return. This process simplifies tax filings for nonresidents earning income in New Jersey from certain entities, allowing them to be taxed collectively rather than individually. The form requires attention to detail and accuracy to ensure that all the necessary information is provided correctly. Follow these steps carefully to complete the NJ-1080E form.

- Start by entering the Entity Information in Part 1:

- Provide the Employer Identification Number (EIN) of the filing entity.

- Write the full name of the filing entity.

- Fill in the mailing address, city, state, and ZIP code of the entity.

- Include a contact person’s name and telephone number.

- Specify the type of entity from the options listed (e.g., General Partnership, Limited Liability Company, NJ Electing S Corp., etc.).

- Move on to Part 2: Individual Information:

- Enter your Social Security Number.

- Write your full name as it appears on your Social Security card.

- Provide your principal address, including city, state, and ZIP code.

- Read the Individual Consent Statement thoroughly, which outlines your consent to have your income included on the New Jersey Nonresident Composite Return and other conditions.

- Check that you satisfy all conditions listed in the consent statement such as being a nonresident for the entire year, not maintaining a permanent abode in NJ, not filing a fiscal year tax return, among others.

- Sign and date the form at the bottom to indicate your consent and that you've met all necessary conditions.

- Ensure that the information provided is accurate and that you've adhered to the deadlines mentioned in the instructions.

- Retain a copy of the completed NJ-1080E form for your records before submitting it to the filing entity.

The NJ-1080E form must be submitted to the filing entity, not directly to the state. Once the entity receives your completed form, it will include your information when submitting the composite return (Form NJ-1080-C). This collective approach to filing simplifies the taxation process for nonresidents involved with eligible entities in New Jersey. Remember, the NJ-1080E is an annual election, so it's important to complete this process each year you're eligible and choose to participate.

Learn More on Nj 1080E

What is the NJ-1080E form?

The NJ-1080E form, also known as the Election to Participate in a Composite Return, is a document used by qualifying nonresident individuals who earn income from sources within New Jersey through various entities such as partnerships, S corporations, and trusts. By signing this form, these individuals agree to have their New Jersey source income included in a special group tax return filed by the entity, referred to as a composite return (Form NJ-1080-C). This process simplifies tax filing requirements for both the entities and the qualifying nonresident individuals.

Who can participate in a Composite Return using the NJ-1080E form?

To be eligible for participation in a Composite Return, nonresident individuals must satisfy certain criteria, including:

- Being a nonresident of New Jersey for the entire tax year.

- Not maintaining a permanent place of abode in New Jersey at any time during the tax year.

- Not filing a fiscal year tax return for federal income tax purposes.

- Having no New Jersey source income other than what is reported on the composite return.

- Waiving the right to claim New Jersey personal exemptions, credits, or deductions.

This election must be made annually and is binding on the individual's heirs and representatives. The form must be signed and delivered to the filing entity before the deadline, which is April 15th following the close of the tax year.

What responsibilities do participants have after filing the NJ-1080E?

Upon completing and submitting the NJ-1080E form, participants agree to several commitments:

- They consent to include their New Jersey sourced income in the composite return.

- Participants waive their rights to personal exemptions and agree that taxes due will be calculated at the highest rate for single taxpayers for the year.

- The election is considered an irrevocable consent to personal jurisdiction in New Jersey for tax purposes.

- Participants are personally liable for timely filing and payment of taxes, including any penalties or interest from audits.

What are the filing deadlines and payment requirements?

The composite tax return must be filed by the 15th day of the fourth month following the close of the taxable year. For entities that estimate their total tax liability to exceed $100, estimated tax payments are required quarterly. Participants in the composite return cannot make individual estimated payments; instead, the filing entity is responsible for making these payments on behalf of all participants.

How does participating in a Composite Return affect individual New Jersey tax filings?

Participating in a Composite Return changes how nonresident individuals report their New Jersey source income. Instead of filing an individual New Jersey Nonresident Gross Income Tax Return (NJ-1040NR) for the income covered by the composite return, their share of the income and tax is reported through the composite return filed by the entity. However, if a participant has additional New Jersey source income not included in the composite return, they must file an individual NJ-1040NR, and they can claim a credit for the tax paid through the composite return.

Common mistakes

When filling out the New Jersey 1080E form, people often make mistakes that can lead to complications or delays. Understanding these common errors can help ensure that the process goes smoothly. Here are four frequent mistakes:

- Incorrect or Incomplete Information: One of the most common mistakes is providing incorrect or incomplete information about the entity or the individual. This includes errors in the Employer Identification Number (EIN), social security numbers, and mailing addresses.

- Overlooking Entity Type Designation: Failing to correctly specify the type of entity (e.g., General Partnership, Limited Liability Company, Estate or Trust, etc.) can result in processing delays. Each entity type has specific filing requirements and benefits, making this a crucial step.

- Missing Signatures and Dates: The form requires a signature and date to confirm the accuracy and consent of the information provided. Skipping this step can render the form invalid, as it indicates an agreement to all provisions, responsibilities, and liabilities associated with filing a composite return.

- Late Elections: Individuals must elect to be included in a composite return annually. Missing the deadline to make this election (April 17, 2006, for the year in question) or attempting to revoke an election after this date is a mistake that cannot be rectified and may affect tax obligations.

Each part of the NJ-1080E form serves a specific function in ensuring the correct and efficient processing of a composite return. Common errors often involve failing to provide accurate and complete information, not properly identifying the entity type, omitting signatures and dates, and misunderstanding election timings. Avoiding these mistakes helps in the accurate filing of tax returns and adherence to New Jersey tax laws.

Documents used along the form

When preparing to file the Form NJ-1080E, Election to Participate in a Composite Return, there are several other forms and documents that individuals and entities in New Jersey may also need to consider filing. These ancillary documents ensure compliance with all tax requirements and facilitate the thorough completion of tax obligations within New Jersey. Below is a list of these relevant forms and a brief description of each.

- NJ-1080-C: New Jersey Nonresident Composite Return - This form is filed by the entity on behalf of its qualified nonresident individuals, summarizing the income derived from or connected with New Jersey sources and the tax due on that income.

- NJ-1040NR: New Jersey Nonresident Income Tax Return - Nonresident individuals who do not participate in a composite return must file this form to report their income from all sources, including New Jersey sources.

- Form 1040-ES: Estimated Tax for Individuals - Entities that file composite returns and anticipate owing more than $100 in taxes for the current year are required to make quarterly estimated tax payments using this form.

- Form NJ-630: Application for Extension of Time to File New Jersey Gross Income Tax Return - This form is used to request an extension for filing the composite return on behalf of all qualified electing nonresident individuals.

- Schedule NJK-1: New Jersey Partnership Schedule K-1 - Included in the composite return if the filing entity is a partnership, limited liability company, or limited liability partnership, detailing each participant’s share of income and tax paid.

- Schedule NJ-K-1: New Jersey S Corporation Schedule K-1 - Included in the composite return for entities electing S corporation status in New Jersey, detailing each shareholder’s share of income and tax paid.

Each of these forms plays a crucial role in ensuring that nonresident individuals and entities engaged in business or earning income in New Jersey fulfill their state tax obligations accurately and completely. Whether part of a composite return or filing individually, it’s important for participants to be aware of and understand each form’s purpose and requirements. Understanding these accompanying documents contributes to a smoother and more efficient tax filing process.

Similar forms

The NJ 1040NR form, designed for nonresident individuals to report income from New Jersey sources, closely resembles the NJ 1080E form in purpose and audience. Both forms are tailored for individuals who have financial obligations to New Jersey without being residents, focusing on incomes tied to activities or entities within the state. While the NJ 1080E form captures the election to participate in a composite return, the NJ 1040NR is a comprehensive declaration of income, ensuring nonresidents fulfill their tax responsibilities on earnings from New Jersey sources.

Form NJ-1080-C, or the New Jersey Nonresident Composite Return, directly correlates with the NJ 1080E through its function as the collective filing mechanism for participants who have elected via the NJ 1080E form. This form aggregates the income of all participating nonresidents, offering a streamlined approach to tax filing for entities with nonresident members who have income from New Jersey, simplifying the process and reducing the need for multiple individual returns.

Form 1040-ES (NJ), specifically for estimated tax payments, shares a procedural connection with the NJ 1080E, as entities that file a composite return may need to make quarterly estimated tax payments. This form is vital for managing the tax obligations of the composite group throughout the year, ensuring that adequate payments are made in anticipation of the final tax liability, thus linking it back to the composite filing process initiated by the NJ 1080E.

The Schedule NJK-1, affiliated with Form NJ-1065, bears similarity to the NJ 1080E in its role of delineating the income and tax information for individual members within a partnership or LLC engaging in business within New Jersey. The completion of Schedule NJK-1 is necessary for accurately reporting each member's share of income or loss, integral to the composite return process championed by the NJ 1080E form for nonresident participants.

Schedule NJ-K-1 from Form CBT-100S aligns with the NJ 1080E in that it provides key information for members of a New Jersey S corporation about their share of the corporation's income, deductions, and credits. Similar to the NJ 1080E's goal of simplification and group consent, this form helps in organizing the data necessary for nonresident shareholders to be included in a composite return, showcasing each individual's New Jersey source income and respective tax liabilities.

The Federal Schedule K-1 (Form 1041) shares similarities with the NJ 1080E as it deals with the distribution of estate or trust income. When a trust or an estate has income from New Jersey sources and nonresident beneficiaries elect to participate in a composite return, this federal form provides the needed breakdown of income, deductions, and credits that feed into the larger composite reporting process.

Form W-2 for professional athletes who are nonresidents of New Jersey and earn income from the state is related to the NJ 1080E form. Given the unique nature of professional athletes' incomes being sourced from various states, the W-2 form provides essential information for athletes included in a composite return, similar to how the NJ 1080E form facilitates group filing for nonresident individuals.

The United States Federal Nonresident Alien Income Tax Return (Form 1040NR) parallels the NJ 1080E in that it caters to a specific group's tax obligations—nonresident aliens—for their income associated with U.S. sources. Like the NJ 1080E enables nonresidents to fulfill their New Jersey tax obligations collectively, the 1040NR form allows nonresidents to report and pay taxes on their U.S.-sourced income at the federal level.

New Jersey's Estimated Tax Payment form (NJ-630) is indirectly connected to the NJ 1080E form as entities that file composite returns may also need to address their estimated tax payment obligations using this form. It serves to organize the payment of taxes in advance based on the projected tax liability of the entity, thereby influencing the overall process that begins with the election to file a composite return via the NJ 1080E.

The Declaration of Estimated Income Tax (Form 1040-ES) for the federal system aligns with the NJ 1080E in its approach to managing anticipated tax liabilities. While the 1040-ES deals with federal taxes, and the NJ 1080E concerns state taxes for nonresidents, both documents are geared towards ensuring taxpayers accurately report and prepay their income taxes, thereby highlighting the importance of planning and compliance in tax affairs.

Dos and Don'ts

When filling out the NJ-1080E form, there are specific do's and don'ts to ensure the process is completed correctly and efficiently. Here are five of each to guide you:

Things You Should Do:

- Ensure you meet all the eligibility criteria listed under the INDIVIDUAL CONSENT STATEMENT section before signing the election to participate.

- Double-check that you did not maintain a permanent place of abode in New Jersey at any time during the taxable year, as this affects eligibility.

- Verify your nonresident status for the entire tax year and that you are not a fiscal year filer for federal income tax purposes.

- Confirm you do not have income from New Jersey sources other than what is reported through the composite return.

- Clearly print your name, Social Security Number, and the address in the INDIVIDUAL INFORMATION section to avoid processing delays.

Things You Shouldn't Do:

- Do not leave the signature and date fields at the end of the INDIVIDUAL CONSENT STATEMENT section blank. Your form will be considered invalid without them.

- Avoid making the election to participate after the April 17, 2006, deadline, as it will not be accepted.

- Do not file this form if you maintained a permanent place of abode in New Jersey at any time during the taxable year.

- Do not try to revoke your election after the April 17, 2006, deadline, as it is bound to be unsuccessful.

- Refrain from claiming New Jersey personal exemptions, credits, or deductions on your share of the composite income. Acknowledge that your tax will be calculated at the highest rate for single taxpayers.

Misconceptions

Misunderstandings often surround the NJ-1080E form, leading to confusion about its purpose and requirements. Let's clarify some common misconceptions:

- Only for Individuals: Many assume the NJ-1080E is exclusively for individual taxpayers. However, it's actually designed for entities like partnerships, S corporations, and trusts to elect on behalf of their nonresident members to participate in a composite return.

- One-Time Filing: Another common misconception is that once you file NJ-1080E, you're set for life. The truth is, the election to participate in a composite return must be made annually, making it crucial for entities and their nonresident members to stay on top of their filing obligations.

- No Personal Deductions or Credits: Participants sometimes miss that by agreeing to be part of a composite return, they waive the right to claim New Jersey personal exemptions, credits, or deductions. This means the tax due is calculated at the highest rate for single taxpayers, without those potential savings.

- Revoking the Election: There's a belief that you can revoke your election to participate after it's been made. Actually, once the deadline passes (April 17, 2006, for the tax year in the example), the election is irrevocable. This emphasizes the importance of making informed decisions before opting in.

Understanding the NJ-1080E form and the associated responsibilities helps ensure compliance and avoid potential pitfalls of the composite return process. Whether you're part of an entity looking to file on behalf of nonresident members or an individual considering joining a composite return, clarity on these points can guide your decisions.

Key takeaways

Filling out and using the NJ-1080E form is a key step for nonresident individuals who want to be included in a composite New Jersey Nonresident Gross Income Tax Return. Here are six crucial takeaways to keep in mind:

- The NJ-1080E form is an election by a nonresident of New Jersey to have their income included on a composite return filed by an entity, such as a partnership or S corporation, which they are a part of. This allows for a simplified filing process for individuals who are not residents of New Jersey.

- To be eligible to participate in a composite return, individuals must meet several conditions, including being a nonresident for the entire year, not maintaining a permanent place of abode in New Jersey, and not having New Jersey-derived income outside of the composite return.

- By signing the NJ-1080E form, individuals waive their right to claim any personal exemptions, credits, or deductions on their New Jersey income, and agree that their tax will be calculated at the highest rate for single taxpayers.

- The election to participate in the composite return must be made annually, and once made, it cannot be revoked after April 17 of the following year. This decision is also binding on the individual’s heirs and successors.

- The filing entity is responsible for retaining the completed NJ-1080E forms and must provide them to the New Jersey Division of Taxation upon request. These documents serve as consent for the individual’s inclusion in the composite return.

- If, after the composite return is filed, an individual discovers additional income from New Jersey sources not included in the composite return, they must file an individual New Jersey Nonresident Gross Income Tax Return (NJ-1040NR) for that year and include this income. They are entitled to claim a credit for any tax paid on their behalf through the composite return.

This simplified option can make tax season a bit easier for nonresident individuals with New Jersey income, but as always, it's important to ensure all eligibility conditions are met and that the form is correctly completed to avoid any potential issues.

Popular PDF Documents

Tdi Nj - Claimants are required to file the NJ Temporary Disability Form (DS-1) promptly after ceasing work due to disability.

Can an S Corp Be an Llc - Includes a section for corporate information, required payment details, and consent statements essential for retroactive tax status changes.

Nj Raffle Report - Its structured format guides organizations through the reporting process, helping to standardize the submission of important financial data.