Fill Out a Valid Nj 165 Template

At the intersection of state tax policies and individual employment circumstances, the NJ-165 form emerges as a crucial document for many. This form, officially titled "Employee's Certificate of Nonresidence in New Jersey," plays a pivotal role in the financial lives of certain workers in New Jersey. Given its importance, understanding the form's purpose and the specific conditions under which it is utilized is essential for qualifying employees. Primarily, the NJ-165 form is designed for use by Pennsylvania residents who earn income in New Jersey, facilitating an exemption from New Jersey Gross Income Tax withholding due to a reciprocal tax agreement between the two states. Additionally, this form extends its utility to military spouses under the Servicemember Civil Relief Act (SCRA), as amended by the Military Spouses Residency Relief Act, allowing them exemptions from New Jersey income tax on wages under specified conditions. To ensure compliance and benefit from these provisions, employees must accurately complete and submit the form to their employers, who are then responsible for maintaining it on file. This process underscores the nuanced interplay between state tax laws, employment, and individual residency statuses, positioning the NJ-165 form as a critical tool for eligible workers navigating their tax obligations.

Sample - Nj 165 Form

Department of theTreasury |

|

|

|

|

Division ofTaxation |

|

POBox 269 |

|

Trenton, NJ |

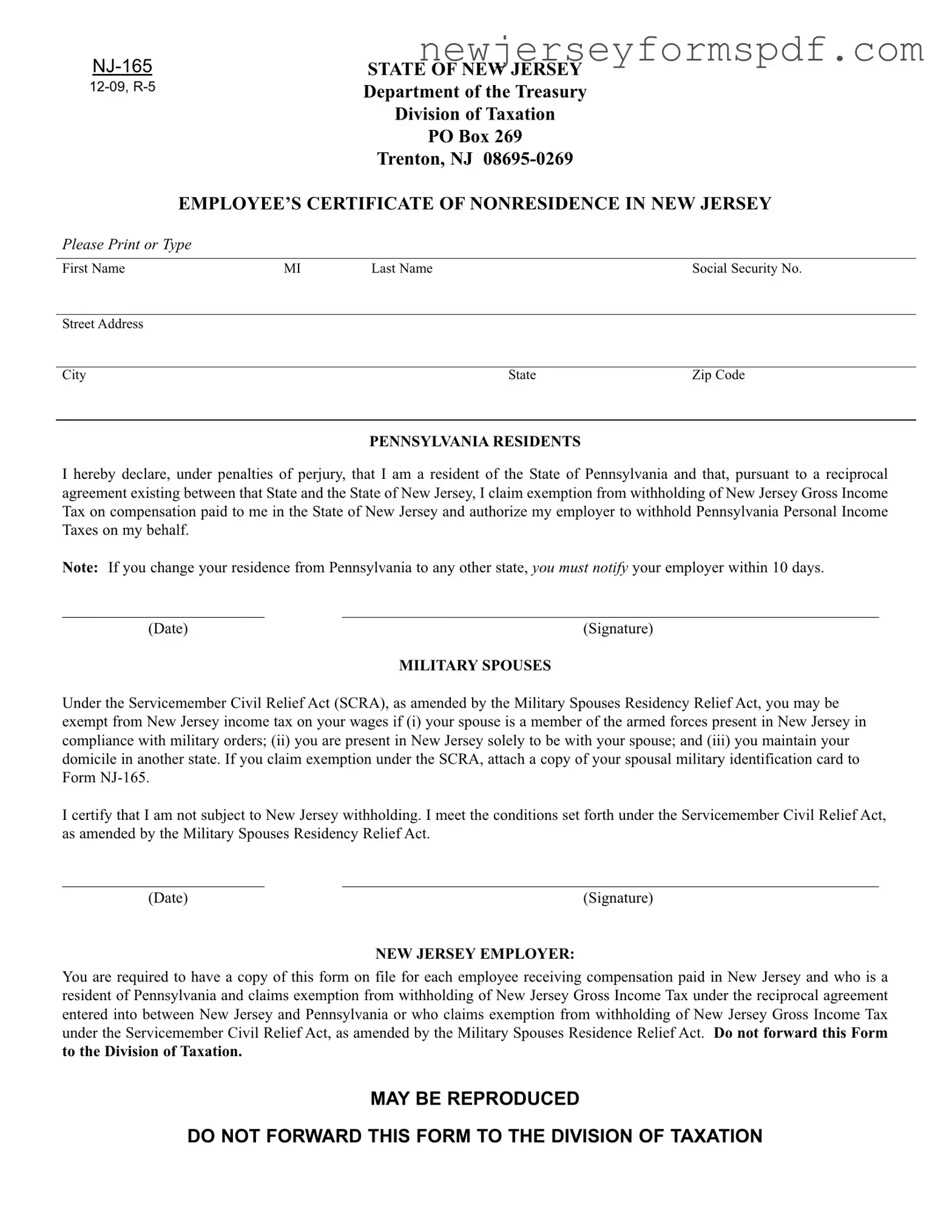

EMPLOYEE’S CERTIFICATE OFNONRESIDENCE IN NEWJERSEY

PleasePrintorType

First Name |

MI |

Last Name |

Social Security No. |

StreetAddress

City |

State |

Zip Code |

PENNSYLVANIARESIDENTS

I hereby declare, under penalties of perjury, that I am a resident of the State of Pennsylvania and that, pursuant to a reciprocal agreementexistingbetweenthatStateandtheStateofNewJersey,IclaimexemptionfromwithholdingofNewJerseyGrossIncome Tax on compensation paid to me in the State of New Jersey and authorize my employer to withhold Pennsylvania Personal Income Taxes on my behalf.

Note: If you change your residence from Pennsylvania to any other state, youmustnotifyyour employer within 10 days.

__________________________ |

_____________________________________________________________________ |

(Date) |

(Signature) |

|

MILITARYSPOUSES |

Under the Servicemember Civil ReliefAct (SCRA), as amended by the Military Spouses Residency ReliefAct, you may be exempt from New Jersey income tax on your wages if (i) your spouse is a member of the armed forces present in New Jersey in compliance with military orders; (ii) you are present in New Jersey solely to be with your spouse; and (iii) you maintain your domicile in another state. If you claim exemption under the SCRA, attach a copy of your spousal military identification card to Form

I certify that I am not subject to New Jersey withholding. I meet the conditions set forth under the Servicemember Civil ReliefAct, as amended by the Military Spouses Residency ReliefAct.

__________________________ |

_____________________________________________________________________ |

(Date) |

(Signature) |

NEWJERSEYEMPLOYER:

You are required to have a copy of this form on file for each employee receiving compensation paid in New Jersey and who is a resident of Pennsylvania and claims exemption from withholding of New Jersey Gross Income Tax under the reciprocal agreement entered into between New Jersey and Pennsylvania or who claims exemption from withholding of New Jersey Gross Income Tax under the Servicemember Civil ReliefAct, as amended by the Military Spouses Residence ReliefAct. Do not forward this Form

to the Division ofTaxation.

MAYBE REPRODUCED

DO NOT FORWARD THIS FORM TO THE DIVISION OF TAXATION

Document Specifications

| Fact Name | Description |

|---|---|

| Form Identification | The form is identified as NJ-165, titled "Employee's Certificate of Nonresidence in New Jersey". |

| Purpose | This form is intended for employees who are residents of Pennsylvania working in New Jersey, or military spouses meeting specific conditions, to claim exemption from New Jersey Gross Income Tax withholding. |

| Reciprocal Agreement | The form facilitates the implementation of a reciprocal agreement between New Jersey and Pennsylvania, allowing Pennsylvania residents to exempt themselves from New Jersey income tax withholding in favor of having their employer withhold Pennsylvania income taxes. |

| Military Spouses Provision | Under the Servicemember Civil Relief Act (SCRA) and the Military Spouses Residency Relief Act, military spouses who meet certain criteria are allowed to claim exemption from New Jersey income tax on their wages. |

| Responsibility of New Jersey Employers | New Jersey employers are required to keep a copy of the completed NJ-165 form for each qualifying employee, but should not forward the form to the New Jersey Division of Taxation. |

Detailed Steps for Using Nj 165

When starting work in New Jersey but living in Pennsylvania or as a military spouse meeting certain criteria, it's necessary to complete the NJ-165 form. This document is essential for ensuring the correct state income tax is withheld from your paycheck. Following the precise steps to fill out this form accurately is crucial. Here is a straightforward guide on how to do just that.

- At the top of the form, clearly print your first name, middle initial, and last name as they appear on official documents.

- Enter your Social Security Number without dashes or spaces.

- Provide your complete street address, including any apartment or suite number, city, state, and zip code.

- For Pennsylvania residents, read the declaration section carefully. If it applies to you—that is, you are a Pennsylvania resident working in New Jersey and wish to claim exemption from New Jersey Gross Income Tax—proceed to the next step. If not, skip to Step 7.

- Sign and date the form in the provided spaces to verify the declaration. Your signature certifies your claim for exemption under the reciprocal agreement between Pennsylvania and New Jersey.

- For military spouses, to claim exemption under the Servicemember Civil Relief Act (SCRA) and the Military Spouses Residence Relief Act, ensure you meet the listed criteria. If you do, attach a copy of your spousal military identification card to the form.

- Similar to Pennsylvania residents, sign and date the form in the designated areas to affirm your eligibility for exemption as a military spouse.

- Keep a copy of the completed form for your records and provide the original to your employer. Remember, it's your responsibility to notify your employer if your residence changes from Pennsylvania to another state within 10 days.

Once the NJ-165 form is correctly filled out and submitted to your employer, they will adjust your state income tax withholdings accordingly. This is a critical step for ensuring that your income taxes are properly managed according to your residency status, avoiding potential issues down the line. Remember, do not send this form to the Division of Taxation. Instead, your employer should retain it for their records.

Learn More on Nj 165

What is the NJ-165 form?

The NJ-165 form, also known as the Employee’s Certificate of Nonresidence in New Jersey, is a document used by individuals who are either residents of Pennsylvania working in New Jersey, or military spouses living in New Jersey under specific conditions, to claim exemption from New Jersey Gross Income Tax withholding. It allows these individuals to have their employer withhold taxes for their state of residence or not at all, in the case of military spouses, instead of New Jersey.

Who needs to fill out the NJ-165 form?

There are two groups of people who need to complete the NJ-165 form:

- Pennsylvania residents working in New Jersey who wish to claim exemption from New Jersey income tax withholding due to a reciprocal agreement between Pennsylvania and New Jersey.

- Military spouses who are in New Jersey to be with their spouse on military orders, maintain domicile in another state, and wish to claim exemption from New Jersey income tax withholding under the Servicemember Civil Relief Act, as amended by the Military Spouses Residency Relief Act.

What is required to claim exemption as a Pennsylvania resident?

Pennsylvania residents must declare, under penalties of perjury, their residency in Pennsylvania and their intention to claim exemption from New Jersey Gross Income Tax withholding due to the reciprocal agreement between Pennsylvania and New Jersey. Additionally, they authorize their employer to withhold Pennsylvania Personal Income Taxes in lieu of New Jersey taxes. It is crucial that these individuals inform their employer within 10 days if they change their residence from Pennsylvania to another state.

How do military spouses claim exemption under the NJ-165?

Military spouses seeking to claim exemption under the NJ-165 must certify that they are not subject to New Jersey withholding by meeting specific conditions set forth under the Servicemember Civil Relief Act, as amended by the Military Spouses Residency Relief Act. These conditions include the spouse being a member of the armed forces present in New Jersey due to military orders, the spouse being in New Jersey solely to be with their military spouse, and maintaining domicile in another state. A copy of the spousal military identification card must be attached to the Form NJ-165 when submitted.

What should New Jersey employers do with the completed NJ-165 form?

New Jersey employers are required to keep a copy of the completed NJ-165 form on file for each employee who is a resident of Pennsylvania and claims the tax withholding exemption under the reciprocal agreement, or for military spouses claiming exemption under the Servicemember Civil Relief Act. Importantly, employers should not forward this form to the Division of Taxation.

Can the NJ-165 form be reproduced?

Yes, the NJ-165 form may be reproduced. Employers or employees may make copies as needed to ensure that all necessary documentation is properly filled out and retained for records. However, each copy must be completed with accurate and current information by the employee.

What is the penalty for not properly filling out or submitting the NJ-165?

Individuals who fail to properly complete or submit the NJ-165 form, or who provide false information, may be subject to penalties under perjury. As the form is a declaration of the individual’s tax status and intentions, accuracy and timeliness are crucial to avoid potential legal and financial repercussions. Employers who do not maintain accurate records as required may also face penalties from the state.

Common mistakes

Filling out the NJ-165 form, which is an Employee’s Certificate of Nonresidence in New Jersey, is crucial for certain Pennsylvania residents and military spouses working in New Jersey. Here are six common mistakes to avoid to ensure the process is smooth and accurate:

Not correctly identifying residency status - It’s important to clearly state if you are a Pennsylvania resident or a military spouse qualifying under the Servicemember Civil Relief Act. This form allows specific individuals to claim exemption from New Jersey Gross Income Tax, and misidentifying can lead to incorrect withholding.

Failing to include necessary documentation - Military spouses need to attach a copy of their spousal military identification card with the NJ-165 form. Overlooking this requirement can result in the rejection of your exemption claim.

Incorrect or incomplete personal information - Ensuring that your first name, middle initial, last name, social security number, and address are filled out correctly and legibly is crucial. Errors or illegible handwriting can lead to processing delays.

Not notifying the employer of a change in residence - If you change your residence from Pennsylvania to another state, you must notify your employer within 10 days. Neglecting to update your employer on time can cause compliance issues with state tax laws.

Forgetting to sign and date the form - The NJ-165 requires your signature and the date to certify your claims under penalty of perjury. An unsigned or undated form is not valid and will not be processed.

Ignoring the notation that this form should not be sent to the Division of Taxation - A common mistake is sending the completed form to the wrong place. Remember, this form must stay with your employer and is not to be forwarded to New Jersey’s Division of Taxation.

By avoiding these mistakes, employees can ensure they are correctly taking advantage of the tax benefits provided by the NJ-165 form. It's about being diligent, precise, and timely in your submissions to ensure everything is in order.

Documents used along the form

When dealing with employee tax forms, particularly for those who live in one state and work in another, it's essential to ensure all necessary documents are prepared and submitted correctly. Alongside the NJ-165 form, several critical documents often come into play. Each serves its distinct purpose and complements the information provided on the NJ-165.

- W-4 Form (Employee's Withholding Certificate): This is a critical document for all employees as it indicates how much federal income tax should be withheld from their pay. It's particularly relevant for those claiming non-residence in New Jersey, as their withholding requirements might differ from residents.

- Local Earned Income Tax Residency Certification Form: Required in some locations, this form helps ensure that local earned income taxes are withheld and remitted to the correct municipality or locality, especially crucial for residents of Pennsylvania working in New Jersey.

- Document verifying Pennsylvania residency: While not a formal form like the others, having a utility bill, lease agreement, or similar document can be necessary for substantiating the claim of Pennsylvania residency on the NJ-165 form.

- Direct Deposit Authorization Form: Many employers offer direct deposit. While not directly related to tax withholding, it's a form employees might complete at the same time as the NJ-165, helping ensure their paychecks are deposited directly into their bank accounts.

- Power of Attorney (POA) Form: In cases where someone else will act on behalf of the employee in tax matters, a POA form might be necessary. This document grants the designated person authority to make decisions and handle transactions related to the employee’s taxes.

- Military Spousal ID Copy: Specifically for military spouses claiming exemption under the Servicemember Civil Relief Act as amended by the Military Spouse Residency Relief Act, a copy of the military ID verifies their eligibility for the exemption claimed on the NJ-165.

Understanding and gathering these documents can streamline the process of correctly filing and claiming exemptions or benefits under tax laws. Whether an employee is moving to a new state, beginning a new job, or navigating tax responsibilities due to changes in their personal situation, being prepared with the right paperwork is a step towards ensuring compliance with state and federal tax regulations.

Similar forms

The W-4 form, known as the Employee's Withholding Certificate, shares similarities with the NJ-165 form in that both are utilized by employees to determine the amount of taxes to be withheld from their paychecks. While the NJ-165 specifically aids in claiming exemption from New Jersey state taxes for nonresidents or military spouses, the W-4 focuses more broadly on federal income tax withholdings based on the individual's filing status, income, and deductions. Both forms play crucial roles in ensuring the correct tax amount is withheld, thereby preventing large dues or refunds during tax season.

The IT-2104 form, or Employee's Withholding Allowance Certificate for the state of New York, parallels the NJ-165 form in its purpose of addressing state tax withholdings, but for New York residents or those earning income in New York. Like the NJ-165, it is designed to help employees claim exemptions or adjust withholding amounts based on personal exemptions and additional allowances. Both forms essentially function to match an employee's state tax withholdings with their anticipated annual tax liabilities.

The DE 4 form, serving as California's version of an employee withholding allowance certificate, is akin to the NJ-165 in functionality but tailored to California's state tax system. Employees use both forms to declare their residency status and to specify exemptions that reduce the amount of state income tax withheld from their wages. Each form is specific to its state's tax laws while similarly empowering employees to manage their state taxation at the source.

The VA-4 form is to Virginians what the NJ-165 is to New Jersey's nonresident employees and military spouses, focusing on withholding amounts for state taxes in Virginia. This form allows Virginian employees to designate exemptions or additional withholding amounts, closely mirroring the intentions behind the NJ-165. Both documents ensure that employees' state tax withholdings align closely with their expected end-of-year tax obligations, providing a mechanism for financial planning and stability throughout the tax year.

Pennsylvania's Residency Certification Form serves a dual role similar to the NJ-165, not only documenting an employee's residency for local Earned Income Tax (EIT) purposes but also facilitating the correct local withholding based on reciprocal agreements between jurisdictions. While its primary focus is local rather than state tax, the form operates under a similar principle to the NJ-165, ensuring that taxes are properly allocated according to the employee's residence and work locations.

The Military Spouses Residency Relief Act (MSRRA) Certificate form, specific to military spouses, parallels the section of the NJ-165 dedicated to military spouses. Both documents are key in asserting tax exemptions based on the MSR RA's protections, which allow military spouses to retain a legal residence for tax purposes in their home state despite relocating under military orders. They ensure that military families are not penalized with additional state taxes due to their required mobility.

The Nonresident Alien Employee's Withholding W-4 Form serves a specialized audience compared to the NJ-165, focusing on federal withholding for employees who are nonresident aliens in the U.S. Despite this difference in target demographic, it shares the NJ-165's objective of ensuring tax withholdings accurately reflect the individual's taxable income and exemptions. Both forms adjust the process of withholding to meet the specific needs of certain groups of employees, thereby streamlining their tax obligations.

The Reciprocal Agreement Between States Form, found between numerous states that allow for cross-border income tax arrangements, like the agreement cited in the NJ-165, directly facilitates such interstate cooperation. These agreements and the forms that support them, including the NJ-165, alleviate tax burdens on employees who work in one state but reside in another by allowing them to pay income taxes only to their state of residence. This ensures fair treatment and simplifies tax compliance for interstate workers.

The Employee's Statement of Nonresidence in the District of Columbia (D-4A) shares its core purpose with the NJ-165, specifically aiding employees who work in D.C. but maintain residency in another state, in claiming exemption from D.C. income tax withholding. Both forms recognize the unique situation of interstate commuters and provide a means to avoid dual taxation, focusing on maintaining the financial rights of individuals who cross state lines for employment.

The Certificate for the Exemption from Withholding for a Dependent Child of Military Personnel Form, while more narrowly focused, similarly offers a tax withholding exemption akin to the NJ-165's section for military spouses. This form specifically benefits children of military personnel who earn income, emphasizing the broader theme of tax relief for military families. Though its audience is more specific, the underlying principle of considering individual circumstances to ensure fair taxation mirrors that of the NJ-165.

Dos and Don'ts

When it comes to filling out the NJ-165 form, it's important to get everything right the first time. This document, critical for certain Pennsylvania residents and military spouses working in New Jersey, ensures that income tax withholding is handled properly. Here's a comprehensive list of dos and don'ts to consider:

- Do thoroughly read the form instructions before you begin to fill it out. Understanding every requirement can save you time and prevent mistakes.

- Do print or type your information clearly. This helps prevent misunderstandings or processing delays by the relevant department or your employer.

- Do double-check your Social Security Number for accuracy. This is a common area for mistakes and is critical for your tax records and identification.

- Do attach a copy of your spousal military identification card if you are claiming exemption under the Servicemember Civil Relief Act (SCRA) and Military Spouses Residency Relief Act, as this is mandatory for the exemption to be processed.

- Don't leave any requested details blank. If a section doesn't apply to you, mark it as "N/A" (not applicable). This indicates you didn't overlook the question.

- Don't forget to sign and date the form. An unsigned form is considered incomplete and will not be processed.

- Don't send this form to the New Jersey Division of Taxation. It is meant to be retained by your employer for record-keeping purposes.

Following these guidelines, you can ensure that the NJ-165 form is filled out correctly, helping to streamline the process for both you and your employer. Remember, taking a few moments to review and double-check your form can prevent potential issues down the line.

Misconceptions

Understanding the NJ-165 form is crucial for individuals working in New Jersey but residing in Pennsylvania or living under special circumstances, like military spouses. However, several misconceptions surround this form. Here, five common misunderstandings are addressed to provide clarity.

It's only for Pennsylvania residents: A prevalent misconception about the NJ-165 form is that it exclusively serves Pennsylvania residents. While Pennsylvania residents can use it to claim exemption from New Jersey Gross Income Tax due to a reciprocal tax agreement, the form also caters to military spouses eligible under the Military Spouses Residency Relief Act. These individuals can claim exemption from New Jersey income tax if they meet specific criteria related to their spouse's military duty in New Jersey.

Completion guarantees no tax responsibility: Another misunderstanding is that filing this form absolves one of any tax responsibilities. In reality, while it allows an individual to claim exemption from New Jersey state tax withholding, Pennsylvania residents are still responsible for filing and paying Pennsylvania state taxes. Military spouses, while exempt from New Jersey taxes when qualifying conditions are met, must ensure compliance with any tax obligations in their state of domicile.

Employees send the form to the New Jersey Division of Taxation: Employees often mistakenly believe that they must send the completed NJ-165 form to the New Jersey Division of Taxation. The instructions explicitly state not to forward this form to the Division of Taxation. Instead, employees should submit it to their employer, who is then responsible for retaining a copy and managing withholding accordingly.

Any change of address doesn't affect the form: Employees sometimes assume once the NJ-165 form is filled out, changes in residence do not impact its validity. However, if a Pennsylvania resident moves to another state or a military spouse's domicile state changes, they must notify their employer within 10 days. Such changes could affect their tax withholding and exemption status.

The form covers all types of income: A common misunderstanding is that the NJ-165 form applies to all types of income earned in New Jersey. The exemption from New Jersey Gross Income Tax withholding under this form specifically applies to compensation for services paid to the employee. Other types of income, such as income from New Jersey sources other than employment, may not be covered by this exemption and could be subject to New Jersey taxation.

Clearing up these misconceptions is essential for ensuring that eligible Pennsylvania residents and military spouses understand their rights and obligations concerning the NJ-165 form. Properly completing and submitting this form helps individuals comply with tax laws while taking advantage of exemptions for which they qualify.

Key takeaways

Understanding the NJ-165 form is crucial for employees who are either residents of Pennsylvania working in New Jersey or military spouses living in New Jersey due to their spouse's military orders. Here are some key takeaways that can help with its completion and use:

- The NJ-165 form is a declaration by an employee that exempts them from withholding New Jersey Gross Income Tax if they are a resident of Pennsylvania or a military spouse meeting certain criteria.

- For Pennsylvania residents, this form serves as a claim for exemption based on a reciprocal agreement between New Jersey and Pennsylvania, allowing these individuals to have Pennsylvania Personal Income Taxes withheld instead of New Jersey Gross Income Tax.

- Military spouses who are in New Jersey to accompany their active-duty spouse and maintain their domicile in another state can use this form to claim exemption from New Jersey income tax on their wages under the Servicemembers Civil Relief Act (SCRA) as amended by the Military Spouses Residency Relief Act.

- A critical requirement for military spouses claiming exemption is the necessity to attach a copy of their spousal military identification card to the NJ-165 form.

- It is essential for Pennsylvania residents and military spouses to notify their employer within 10 days if there is a change in their residence status or if they no longer meet the exemption criteria.

- Employers in New Jersey are mandated to keep a copy of the NJ-165 form on file for each eligible employee but should not forward this form to the Division of Taxation. The statement, "Do not forward this form to the Division of Taxation," helps ensure that the form is used correctly and kept for record-keeping purposes only by the employer.

Correctly completing and submitting the NJ-165 form ensures that eligible employees are not subject to New Jersey Gross Income Tax withholding unnecessarily and aids in proper tax compliance for both employers and employees.

Popular PDF Documents

Nj Petit Juror Questionnaire - Provides a mechanism for new installations, registration of unregistered tanks, and amendments to existing registrations under New Jersey law.

Proof of Service Nj - Delineates the financial oversight and budget management responsibilities of the role.

New Jersey D 3 - Aids in the organization of a committee's financial infrastructure, providing a clear framework for managing campaign funds.