Fill Out a Valid Nj 2440 Template

In the complex landscape of tax regulations within the State of New Jersey, the NJ-2440 form serves as a critical document for employees who have received payments through accident and health insurance plans due to personal injuries or sickness. Issued by the State of New Jersey Division of Taxation, this form is designed to support the exclusion of such payments from taxable gross income under specific conditions outlined in the New Jersey Administrative Code (N.J.A.C. 18:35-2.3). To qualify, these payments must compensate for wage loss from an employee's work absence due to injury or sickness, ensuring a level of certainty under a binding contractual agreement within the insurance plan, and cannot be related to discretionary sick leave wage continuation payments. The NJ-2440 form delineates the required information concerning the employee, employer, insurance plan, sickness periods, and payments, establishing a structured process for claiming exclusions. However, even when payments qualify for exclusion from gross income taxation, withholding of the gross income tax may still apply, except under specific circumstances such as payments from the State temporary disability benefit plan or from a commercial insurance company under a health or accident insurance policy. Additionally, the form emphasizes the necessity for all claimants to file with their annual New Jersey Gross Income Tax Return, ensuring proper compliance with state tax laws and providing clear examples to guide both employees and employers through the qualifying conditions and exclusion claims process.

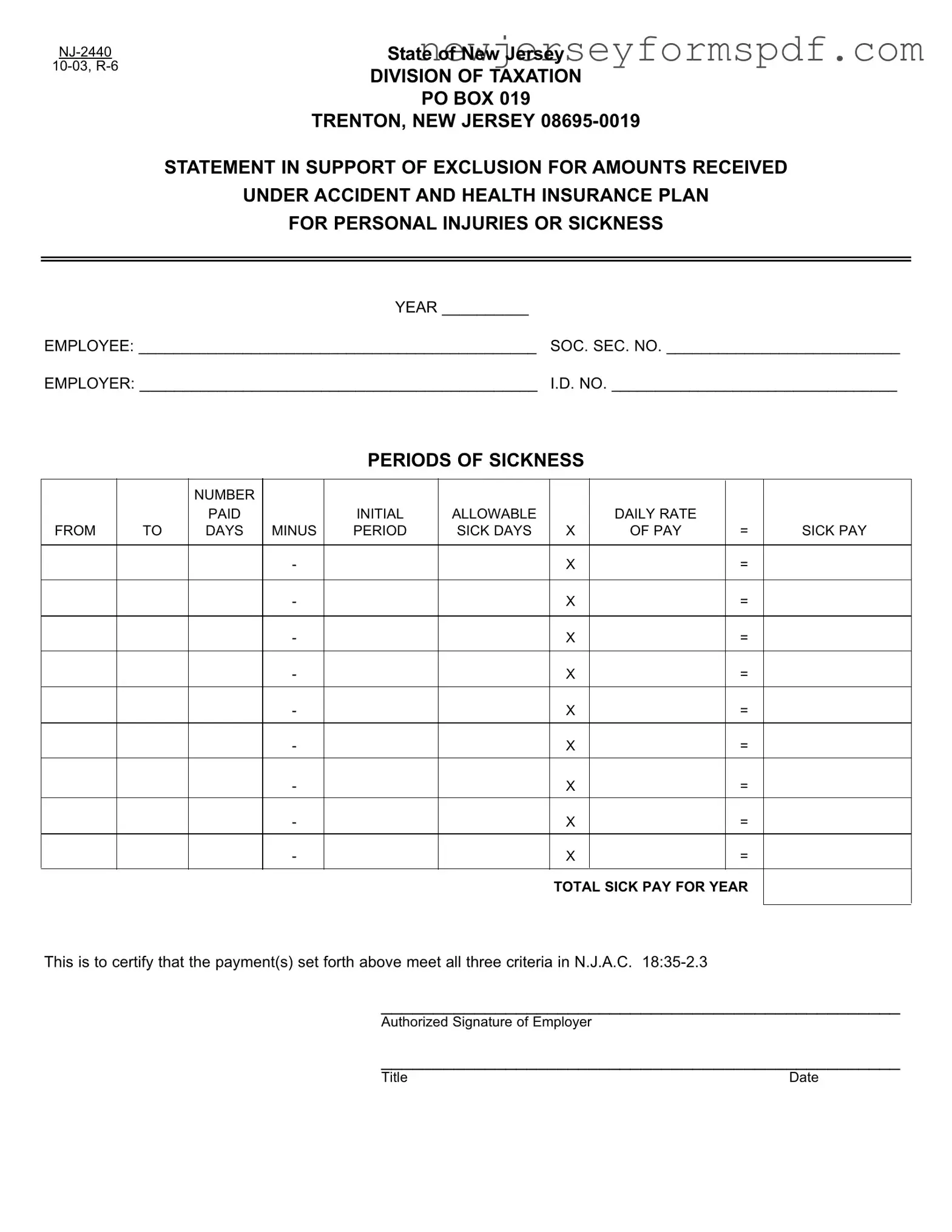

Sample - Nj 2440 Form

State of New Jersey

DIVISION OF TAXATION

POBOX 019

TRENTON, NEW

STATEMENT IN SUPPORT OF EXCLUSION FOR AMOUNTS RECEIVED

UNDER ACCIDENT AND HEALTH INSURANCE PLAN

FOR PERSONALINJURIES OR SICKNESS

YEAR __________

EMPLOYEE: ______________________________________________ SOC. SEC. NO. ___________________________

EMPLOYER: ______________________________________________ I.D. NO. _________________________________

PERIODS OF SICKNESS

|

|

NUMBER |

|

|

|

|

|

|

|

|

|

|

PAID |

|

INITIAL |

ALLOWABLE |

|

DAILY RATE |

|

|

|

FROM |

TO |

DAYS |

MINUS |

PERIOD |

SICK DAYS |

X |

OF PAY |

= |

|

SICK PAY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

|

X |

|

= |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

|

X |

|

= |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

|

X |

|

= |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

|

X |

|

= |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

|

X |

|

= |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

|

X |

|

= |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

|

X |

|

= |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

|

X |

|

= |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

|

X |

|

= |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTAL SICK PAY FOR YEAR |

|

|||

|

|

|

|

|

|

|

|

|

|

|

This is to certify that the payment(s) set forth above meet all three criteria in N.J.A.C.

__________________________________________________

Authorized Signature of Employer

__________________________________________________

Title |

Date |

Gross Income Tax

Employee Accident or Health Insurance Exclusion

N.J.A.C.

(a)Amounts received by an employee through an accident or health insurance plan for personal injuries or sickness are not subject to tax under the New Jersey Gross Income Tax Act.

(b)Amounts received by an employee on account of personal injury or sickness qualify for exclusion from taxable gross income when received under the provisions of an employee accident or health insur- ance plan which satisfies the following requirements:

1.The payments must be compensation for wage loss which results from absence due to injury or sickness of the employee; and

2.The payments must have a requisite certainty under an enforce- able contractual obligation under the plan (see N.J.A.C.

3.Thepaymentsmustnotrelatetosickleavewagecontinuation,the taking of which is largely discretionary and the payments are made regardless of the reason for absence from work.

(c)The exclusion from taxable gross income applies to payments to employees under a health or accident insurance plan regardless of whether insurance coverage is with a commercial insurance company to which premiums are paid by both employees and employer or sole- ly by the employer; or whether insurance coverage is provided by an employer’s

(d)The exclusion from taxable gross income applies to payments required to be made to employees under the State mandated tempo- rary disability benefit plan pursuant to the New Jersey Temporary Disability Law (N.J.S.A.

(e)Where payment to employees under the health or accident insurance plan is largely discretionary with the employer, such as dur- ing the initial period (for example, first seven days), the exclusion from taxable gross income does not apply. Such payments to the employ- ee are subject to tax as wages and salaries. In order for a wage loss payment made under an accident or health insurance plan to be excludable from taxable gross income, the payment to the employee must have a requisite certainty under an enforceable contractual oblig- ation.

(f)Effective June 1, 1982, withholding of the gross income tax shall be required on all payments of wages and salaries made to an employee by an employer. The withholding or the tax is required even though such payments meet all the conditions for exclusion from tax- able gross income as made through an accident or health insurance plan for personal injuries or sickness under this section. The only exceptions for the withholding of tax shall be for the following:

1.Temporary disability benefit payments required to be made under the State Plan which is administered by the Bureau of State Plan Disability Benefits under the New Jersey Disability Law;

2.Temporary disability benefit payments required to be made to employees under a company’s private plan established pursuant to New Jersey law in lieu of the State Plan described in (f)1 above and which has been approved by the Bureau of Private Plan Disability Benefits, Division of Unemployment Insurance and Disability Insurance; and

3.Payments made to employees for personal injuries or sickness under a health or accident insurance policy by a commercial insurance company.

(g)All taxpayers will be required to file with their annual New Jersey Gross Income Tax Return a claim form furnished by the direc- tor for the exclusion of any amounts received by them as an employee through an accident or health insurance plan for personal injuries or sickness which meet all the conditions for exclusion from taxable gross income under (f) 1, 2 and 3 above.

EXAMPLES:

i. An employee of Company X is allowed 12 vacation days and 15 sick days for the year 1982. The employee uses 12 vacation days and 10 sick days in 1982 for which he receives his regular wage payment, regardless of the cause for his absence. The amounts received by the employee in 1982 for the 12 vacation days and 10 sick days are sub- ject to tax as wage and salary income to the employee and the employ- er must also withhold gross income tax on such payments.

ii. Company Y has a

iii. Employee C receives a payment in 1982 from the New Jersey Disability Benefit Fund during an absence from work because of tem- porary disability resulting from illness. Both the employee and employ- er have contributed to the disability benefit fund. The total amount received by the employee from the New Jersey Disability Benefit Fund is excludable from taxable gross income as a payment for health or accident insurance and is not subject to withholding tax.

iv.Employee D is absent from work in 1982 because of illness and receives from the X Insurance Company the full amount of his wages during the period of his absence from work. The payment was made from a health or accident insurance policy to which only the employer has contributed. The amounts received by the employee are exclud- able from taxable gross income as health or accident insurance and are not subject to withholding tax.

Document Specifications

| Fact | Description |

|---|---|

| Form Identification | NJ-2440 is designed for reporting exclusions for amounts received under accident and health insurance plans for personal injuries or sickness. |

| Governing Law | The form is governed by the New Jersey Administrative Code N.J.A.C. 18:35-2.3 and New Jersey Gross Income Tax Act. |

| Eligibility | Payments must compensate for wage loss due to employee's injury or sickness and have enforceable contractual certainty under the plan. |

| Exclusion Criteria | Payments not related to sick leave wage continuation where taking of leave is discretionary are excluded from taxable gross income. |

| Insurance Plan Requirements | The exclusion applies regardless of whether the insurance coverage is through a commercial insurance company, by the employer solely, or a self-insured plan by the employer. |

| Inclusion of State Mandated Benefits | Payments under state-mandated temporary disability benefit plans are included in the exclusion from taxable gross income. |

| Discretionary Payments | If payments under the health or accident insurance plan are largely discretionary by the employer, the exclusion does not apply, and such payments are subject to tax. |

| Withholding Requirement | Withholding of gross income tax is required on wage and salary payments unless specified exceptions are met. |

| Filing Requirements | Taxpayers must file a claim form with their New Jersey Gross Income Tax Return for the exclusion of any amounts received under an accident or health insurance plan. |

Detailed Steps for Using Nj 2440

Before embarking on filling out the NJ-2440 form, it's important to gather all necessary information regarding the periods of sickness, the total sick pay for the year, and any deductions. Understanding the details of your accident and health insurance plan is also crucial, as this form is used to certify payments that meet certain criteria for exclusion from taxable gross income in New Jersey. Keep in mind that the aim here is to accurately report these figures to ensure compliance with New Jersey tax laws. Follow the steps carefully, and consult with your employer or insurance plan administrator if you have any doubts.

- Enter the tax year concerned at the top of the form where "YEAR" is mentioned.

- Fill in the "EMPLOYEE" section with your full name as indicated on your employment records.

- Write your Social Security Number in the designated space next to "SOC. SEC. NO.".

- Under "EMPLOYER," provide the name of your employer as recognized officially.

- Input the Employer Identification Number (I.D. NO.) next to the employer’s name.

- For each period of sickness, enter the starting and ending dates in the "FROM" and "TO" columns, respectively.

- Record the number of allowable sick days paid out for each period in the "DAYS" column.

- Identify and enter the initial allowable "DAILY RATE" of sick pay.

- Calculate the total sick pay for each period by subtracting the period from the daily rate times the number of sick days, and enter these amounts in the corresponding columns.

- Sum up all the figures in the "TOTAL SICK PAY FOR YEAR" row at the bottom of the form.

- Once all information is recorded, ensure the form is verified with an "Authorized Signature of Employer," along with the title of the signatory and the date.

After completing and submitting the NJ-2440 form, the State of New Jersey Division of Taxation will review the information to confirm that the payments received under your accident and health insurance plan for personal injuries or sickness meet the necessary criteria for exclusion from your taxable gross income. This step is part of ensuring that individuals receive the correct treatment under New Jersey's tax laws for such payments. Recognizing the nuances of these exclusions and properly documenting them can help ensure compliance and potentially reduce taxable income, reflecting accurately on annual tax returns.

Learn More on Nj 2440

What is the NJ-2440 form?

The NJ-2440 form is a document provided by the State of New Jersey Division of Taxation. It is utilized to support the exclusion of certain amounts received under accident and health insurance plans for personal injuries or sickness from taxable gross income. Employees use this form to certify sickness-related payments that meet specific criteria outlined by New Jersey regulations.

Who needs to fill out the NJ-2440 form?

This form needs to be completed by employees who have received payments through an accident or health insurance policy due to personal injury or sickness. These payments must meet specific conditions to qualify for exclusion from taxable gross income under New Jersey law.

What are the conditions for payments to be excluded from taxable gross income?

For payments to be excluded from taxable gross income, they must satisfy the following conditions:

- The payments must serve as compensation for wage loss resulting from the employee's absence due to injury or sickness.

- There must be a requisite certainty to the payments under an enforceable contractual obligation of the plan.

- The payments should not be related to sick leave wage continuation where taking leave is largely discretionary, and payments are made regardless of the reason for the absence.

Are all insurance payments excludable from gross income tax?

No, not all insurance payments are excludable. The exclusion from taxable gross income applies to payments under a health or accident insurance plan, including payments from commercial insurance companies or employer’s self-insured plans, and state-mandated temporary disability benefit plans. However, payments made to employees during discretionary periods (like the initial days of absence) or for any sick leave wage continuation are subject to tax as wages.

Are there any exceptions to gross income tax withholding on these payments?

Yes, there are exceptions. While gross income tax withholding is required on most wage and salary payments, exceptions include:

- Temporary disability benefit payments under the State Plan administered by the Bureau of State Plan Disability Benefits.

- Temporary disability benefit payments under a company’s private plan approved by the Bureau of Private Plan Disability Benefits.

- Payments for personal injuries or sickness made under a health or accident insurance policy by a commercial insurance company.

How do employees claim an exclusion for these insurance payments on their tax returns?

Employees must file a claim form with their annual New Jersey Gross Income Tax Return to claim an exclusion for any amounts received through an accident or health insurance plan for personal injuries or sickness. These claims are subject to all conditions for exclusion from taxable gross income.

Common mistakes

When filling out the NJ-2440 form, many individuals often overlook or incorrectly handle certain aspects. It's crucial to avoid these mistakes to ensure the process proceeds smoothly and accurately. Here’s a list of common errors:

- Incorrect Employee Information: Filling in the wrong Social Security number or misspelling the employee's name can lead to processing delays.

- Inaccurate Employer Details: Similar to employee information, incorrectly entering the employer’s name or I.D. number can cause significant issues.

- Miscalculating Sick Pay: Incorrect calculations of the total sick pay, including wrong initial allowable daily rate, sick days paid, or incorrect deductions, can misrepresent an employee's entitlement.

- Omitting Periods of Sickness: Failure to include all periods of sickness within the taxable year can result in underreporting of sick pay received.

- Forgetting to Sign: The form requires an authorized signature from the employer. Neglecting this can invalid the submission.

- Misunderstanding Exclusion Criteria: Mistakes often happen when individuals do not correctly understand what payments qualify for exclusion under the N.J.A.C. 18:35-2.3 regulations.

To further explain, let’s break down the types of payments often misunderstood for exclusion:

- Payments received during the discretionary period by the employer are often wrongly considered for exclusion.

- Temporary disability benefit payments under the State Plan or an approved private plan often cause confusion regarding their taxability.

- Payments from a health or accident insurance policy by a commercial insurance company, where the employer contributes, are sometimes mistakenly thought to be taxable.

Understanding and avoiding these common errors can streamline the filing process and ensure that every employee's form is accurately and efficiently handled.

Documents used along the form

When it comes to handling the NJ-2440 form, which supports the exclusion of certain amounts received under an accident and health insurance plan for personal injuries or sickness from New Jersey gross income tax, it's often part of a larger documentation process. Being aware of other forms and documents that frequently accompany or are related to the NJ-2440 can simplify the process of claiming these exclusions and ensure compliance with New Jersey tax regulations.

- New Jersey W-4 Form: Used by employees to determine the amount of state income tax to be withheld from their paychecks. It's an important document for anyone who's claiming exclusions based on accident or health insurance plans, as it might affect withholdings.

- NJ Temporary Disability Claim Form: Required for those seeking to receive temporary disability benefits under a state or private plan in New Jersey. This document is often filed in conjunction with the NJ-2440 when disabilities or illnesses lead to wage loss.

- Employment Verification Form: Confirms an individual's employment status and income level. Although not specific to the NJ-2440, it may be requested to verify eligibility for certain exclusions or benefits.

- Medical Certification Form: Used by healthcare providers to certify the nature of an employee's injury or sickness. This form provides the necessary medical details to support the claim for exclusion on the NJ-2440.

- Wage and Tax Statement (W-2 Form): This form reports an employee's annual wages and the amount of taxes withheld from their paycheck. It might be reviewed in conjunction with the NJ-2440 to ensure that excluded payments are properly accounted for.

- Private Insurance Claim Form: For individuals whose accident or health insurance plans are through private insurers rather than through the employer or the state. The information might be needed to complete or support entries on the NJ-2440.

- Policy Documents for Employer-provided Accident or Health Plan: These documents outline the coverage, benefits, and exclusions of an employer-provided plan and can help determine which payments qualify for exclusion on the NJ-2440.

Understanding and gathering the appropriate documents is crucial for correctly filling out the NJ-2440 and ensuring that all relevant exclusions are claimed. Keeping good records and staying informed about the requirements can help streamline the process and potentially reduce tax liability.

Similar forms

The NJ-2440 form, focusing on the exclusion of amounts received under an accident and health insurance plan for personal injuries or sickness from taxable gross income, shares similarities with the IRS Form W-2. The W-2 form, used for reporting wages paid and taxes withheld by an employer to an employee, also delineates various types of income and deductions, including pre-tax contributions to health plans, which can affect taxable income. Both forms serve as critical documents for accurately determining the tax obligations related to employment income and benefits, emphasizing the importance of understanding diversified income sources and their tax implications.

Another document akin to the NJ-2440 form is the IRS Form 1099-MISC, which is used to report payments made in the course of a trade or business to others who are not employees. Similar to the NJ-2440, the 1099-MISC includes provisions for reporting payments that may not be subject to standard wage taxes but are still relevant for tax purposes. While the 1099-MISC captures a broader spectrum of payments, including rents, royalties, and non-employee compensation, it, like the NJ-2440, highlights the complexity and breadth of taxable and non-taxable income, underscoring the meticulous nature required in tax reporting and compliance.

Comparable to the NJ-2440, the Schedule C (Form 1040), used by sole proprietors to report income and expenses, emphasizes the individual's responsibility in declaring various income types and the potential for exclusions or deductions. Like the NJ-2440’s focus on excluding specific insurance payments from gross income, Schedule C allows for the exclusion of certain expenses that can reduce taxable income. Both documents necessitate a detailed understanding of what constitutes taxable income and allowable deductions or exclusions, showcasing the nuanced nature of tax law and its impact on personal and business finances.

Similarly, the IRS Form 8839, Qualified Adoption Expenses, is related to the NJ-2440 in its provision for excluding specific personal expenses from taxable income. Form 8839 enables individuals to claim a tax credit for certain expenses related to the adoption of a child, demonstrating the IRS's recognition of significant personal life events and their financial implications. Like the NJ-2440 form, which allows for the exclusion of health or accident insurance payments from taxable income, Form 8839 emphasizes the government's role in providing tax relief for particular personal circumstances, illustrating the varied ways tax policy supports individuals through different life stages and challenges.

Dos and Don'ts

Filling out the NJ-2440 form, which involves reporting amounts received under an accident and health insurance plan for personal injuries or sickness, requires careful attention to detail to ensure accuracy and compliance with New Jersey tax laws. Here are some recommended dos and don't who can facilitate the process:

- Do ensure you have all the relevant information on hand before you start filling out the form, including the employee's social security number, the employer's identification number, and details about the periods of sickness.

- Do carefully read through N.J.A.C. 18:35-2.3 to understand the criteria for exclusions from taxable gross income to ensure accurate reporting.

- Do check that the amounts reported reflect payments for wage loss due to personal injury or sickness and that these payments meet the requisite certainty under an enforceable contractual obligation.

- Do verify that the exclusion claimed does not relate to sick leave wage continuation, as payments for discretionary sick leave taken are not eligible for exclusion.

- Do sign the form and have it authorized by the employer to certify that the payments reported meet all the criteria for exclusion.

- Don't skip any sections or leave blanks on the form; if a section does not apply, indicate this with a "N/A" or "0" as appropriate to show that it has been reviewed.

- Don't try to claim exclusions for amounts that do not qualify under the strict conditions outlined in N.J.A.C. 18:35-2.3, such as payments for discretionary sick leave or those that fail to meet the requisite certainty under an enforceable contractual obligation.

- Don't forget to include all periods of sickness during the year, even if some of them might not qualify for exclusion, to provide a complete record.

- Don't overlook the need to keep copies of all documentation supporting the exclusion claimed, including insurance policies and medical documentation, in case of a future audit.

- Don't disregard the fact that even if amounts are excluded from taxable gross income, they might still be subject to withholding of gross income tax as per subsection (f) unless specifically exempted.

Misconceptions

Many people have misconceptions about the New Jersey Form NJ-2440, which is used for reporting the exclusion of income received under an accident and health insurance plan for personal injuries or sickness. Below are five common misunderstandings and explanations to clarify them.

Form NJ-2440 allows all sickness or accident insurance payments to be non-taxable. This is incorrect. Only amounts received for personal injury or sickness under certain conditions qualify for exclusion from taxable gross income. The insurance plan must compensate for wage loss due to injury or sickness, and the payments must have a requisite certainty under an enforceable contractual obligation. Payments related to sick leave wage continuation that is largely discretionary do not qualify.

Employees need not report payments excluded from their taxable income. Contrary to this belief, all taxpayers must file a claim form with their annual New Jersey Gross Income Tax Return for any amounts excluded under this provision. This ensures proper documentation and compliance with state tax laws.

Only payments from commercial insurance companies can be excluded. This misunderstanding overlooks that exclusions also apply to payments under an employer’s self-insured plan or those mandated under the New Jersey Temporary Disability Law, irrespective of the source, as long as they meet the qualifying criteria.

Tax withholding is not required on any payments made through insurance plans for personal injuries or sickness. This is not entirely true. Effective June 1, 1982, withholding of gross income tax is required on all payments made to employees, with limited exceptions such as certain temporary disability benefit payments.

The form is only for employer use. While it may seem that way, since an authorized employer signature is required to certify the payments, the form actually benefits both employers and employees by officially documenting the exclusion of specific payments from taxable gross income. This documentation is crucial for both parties come tax season.

Understanding the specifics of Form NJ-2440 is crucial for both employees and employers to ensure that they comply with New Jersey's tax laws while accurately reporting income and exclusions related to accidents and health insurance plans for personal injuries or sickness.

Key takeaways

When filing out and using the NJ-2440 form in the State of New Jersey, understanding its purpose and requirements is crucial. Below are six key takeaways to guide individuals through this process:

- Objective of NJ-2440: This form supports the exclusion of certain amounts received under accident and health insurance plans for personal injuries or sickness from taxable gross income.

- Qualifying Payments: Amounts received by an employee for wage loss due to absence from work because of injury or sickness, under an enforceable plan, qualify for exclusion.

- Non-Qualifiable Payments: Payments related to sick leave wage continuation, which are largely discretionary and made regardless of absence reason, do not qualify for exclusion.

- Insurance Coverage: The exclusion applies whether the insurance coverage is through a commercial insurance company paid by both employer and employee, solely by the employer, or under an employer’s self-insured plan not funded by employee premiums.

- Withholding Requirements: Despite exclusion from taxable income, withholding of gross income tax on these payments is mandatory, with specific exceptions for certain types of disability benefits.

- Filing Requirements: Taxpayers must file a claim form with their New Jersey Gross Income Tax Return to exclude amounts received under an accident or health insurance plan for personal injuries or sickness, adhering to the conditions outlined in the NJ-2440 form.

These points are intended to clarify the process of excluding certain insurance payments from gross income tax in New Jersey, aiding employees in navigating their tax obligations appropriately.

Popular PDF Documents

Working Papers - The form is part of New Jersey's efforts to regulate youth employment and ensure fair labor practices for minors.

Nj Annulment Forms Pdf - Filing the NJ CN 10482 form involves detailed instructions to ensure that all necessary information is provided for the court’s consideration.