Fill Out a Valid Nj Estate Template

When dealing with the aftermath of a loved one's passing, navigating through the paperwork required by the New Jersey Division of Taxation can feel daunting, especially concerning the Inheritance and Estate Tax Application for Extension of Time to File a Return. This crucial document, known formally as IT-EXT, serves as a lifeline for executors, administrators, heirs-at-law, or estate representatives who find themselves needing more time to compile the necessary information to accurately complete estate or inheritance tax returns. The form requires detailed information about the decedent including their name, social security number, date of death, and county of residence, and it distinguishes between those who have left a will (testate) and those who have not (intestate). Applicants have the option to request extensions for filing inheritance tax and estate tax returns, which are initially due 8 and 9 months after the decedent's death, respectively. While an extension grants additional time to file, it does not extend the time to pay any taxes owed, with interest accruing after the original due dates. It is also worth noting that the pursuit of an extension may not halt the receipt of computer-generated delinquent notices, underscoring the importance of timely action and thorough understanding of the extensions' limitations and requirements. With penal implications for perjury, it is crucial that all information provided on the form is accurate and truthful, making the process of applying for an extension not just a procedural step, but a commitment to handling a decedent's estate with the utmost integrity and diligence.

Sample - Nj Estate Form

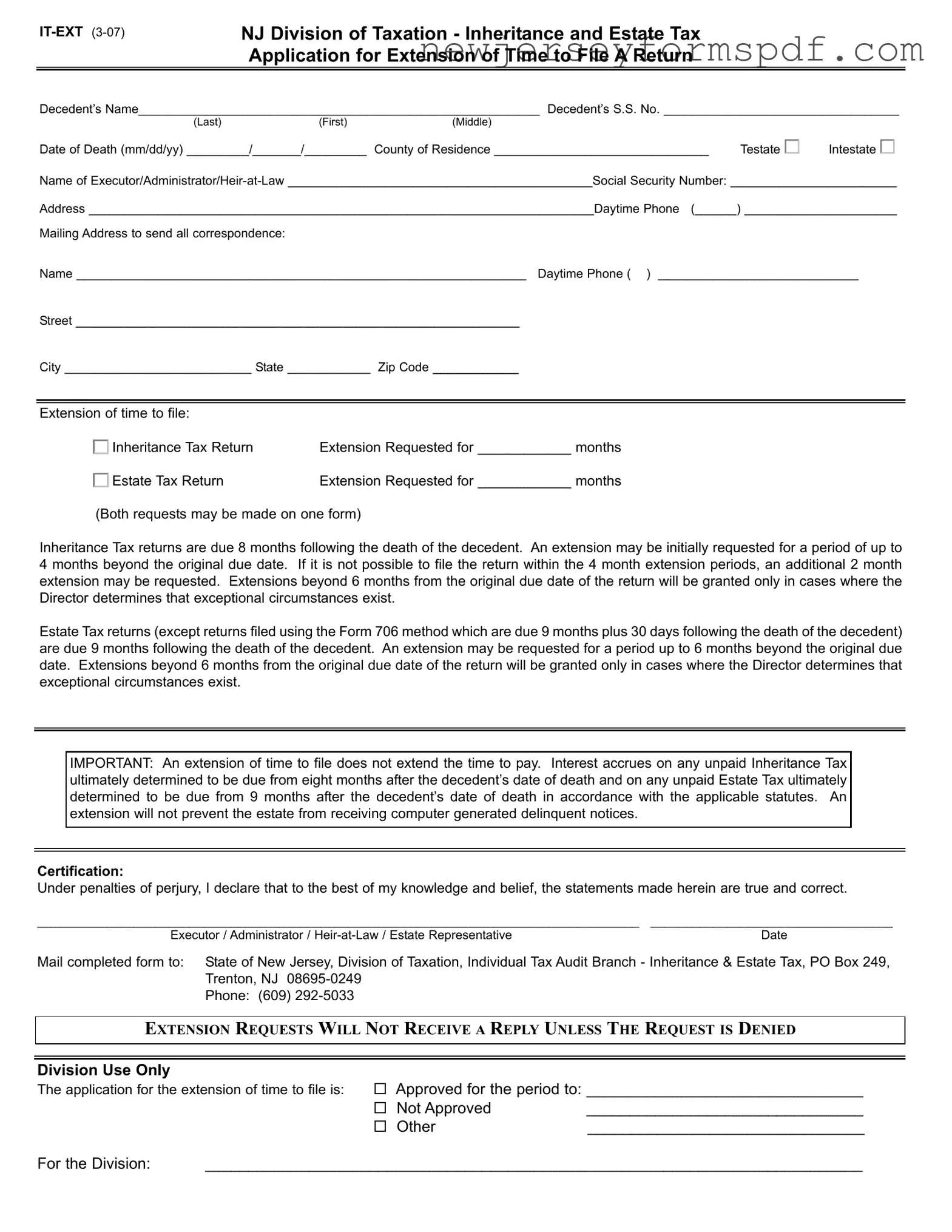

NJ Division of Taxation - Inheritance and Estate Tax Application for Extension of Time to File A Return

Decedent’s Name__________________________________________________________ Decedent’s S.S. No. __________________________________

(Last) |

(First) |

(Middle) |

|

|

Date of Death (mm/dd/yy) _________/_______/_________ |

County of Residence _______________________________ |

Testate |

Intestate |

|

Name of

Address _________________________________________________________________________Daytime Phone (______) ______________________

Mailing Address to send all correspondence:

Name _________________________________________________________________ Daytime Phone ( ) _____________________________

Street _________________________________________________________

City ___________________________ State ____________ Zip Code ___________

Extension of time to file: |

|

Inheritance Tax Return |

Extension Requested for ____________ months |

Estate Tax Return |

Extension Requested for ____________ months |

(Both requests may be made on one form)

Inheritance Tax returns are due 8 months following the death of the decedent. An extension may be initially requested for a period of up to 4 months beyond the original due date. If it is not possible to file the return within the 4 month extension periods, an additional 2 month extension may be requested. Extensions beyond 6 months from the original due date of the return will be granted only in cases where the Director determines that exceptional circumstances exist.

Estate Tax returns (except returns filed using the Form 706 method which are due 9 months plus 30 days following the death of the decedent) are due 9 months following the death of the decedent. An extension may be requested for a period up to 6 months beyond the original due date. Extensions beyond 6 months from the original due date of the return will be granted only in cases where the Director determines that exceptional circumstances exist.

IMPORTANT: An extension of time to file does not extend the time to pay. Interest accrues on any unpaid Inheritance Tax ultimately determined to be due from eight months after the decedent’s date of death and on any unpaid Estate Tax ultimately determined to be due from 9 months after the decedent’s date of death in accordance with the applicable statutes. An extension will not prevent the estate from receiving computer generated delinquent notices.

Certification:

Under penalties of perjury, I declare that to the best of my knowledge and belief, the statements made herein are true and correct.

_______________________________________________________________________________________ ___________________________________

Executor / Administrator / |

Date |

||

Mail completed form to: |

State of New Jersey, Division of Taxation, Individual Tax Audit Branch - Inheritance & Estate Tax, PO Box 249, |

||

|

Trenton, NJ |

|

|

|

Phone: (609) |

|

|

|

|||

EXTENSION REQUESTS WILL NOT RECEIVE A REPLY UNLESS THE REQUEST IS DENIED |

|||

|

|

|

|

|

|

|

|

Division Use Only |

|

Approved for the period to: ________________________________ |

|

The application for the extension of time to file is: |

|||

|

|

Not Approved |

________________________________ |

|

|

Other |

________________________________ |

For the Division: |

____________________________________________________________________________ |

||

Document Specifications

| Fact Name | Description |

|---|---|

| Form Title | IT-EXT (3-07) Inheritance and Estate Tax Application for Extension of Time to File A Return |

| Issuing Body | NJ Division of Taxation |

| Intended Use | Application for extending the filing deadline for Inheritance and Estate Tax Returns |

| Inheritance Tax Return Original Due Date | 8 months following the decedent's date of death |

| Estate Tax Return Original Due Date | 9 months following the decedent's date of death |

| Maximum Initial Extension Period | Up to 4 months for Inheritance Tax; 6 months for Estate Tax |

| Additional Extension | 2 more months for Inheritance Tax, under specific conditions; Estate Tax extensions beyond 6 months require exceptional circumstances |

| Payment of Tax vs. Filing Extension | An extension to file does not extend the time to pay the tax due |

| Governing Law | NJ State Tax statutes as applicable to Inheritance and Estate Taxes |

Detailed Steps for Using Nj Estate

Filing for an extension of time to file an inheritance or estate tax return in New Jersey can give you the breathing room needed to accurately gather and report pertinent financial information following the death of a loved one. It's a straightforward process, but it must be done carefully to ensure proper adherence to deadlines and avoid unnecessary complications. Below are step-by-step instructions on how to fill out the NJ Estate form IT-EXT, ensuring you meet all requirements for a successful application.

- Begin by writing the decedent's name in the designated space, making sure to include their last, first, and middle names as applicable.

- Enter the decedent's Social Security Number immediately following their name.

- Specify the date of death (mm/dd/yy) in the next section.

- Fill in the county of residence of the decedent at the time of their death.

- Determine if the decedent died with a will (testate) or without a will (intestate) and mark the appropriate box.

- Provide the name of the Executor/Administrator/Heir-at-Law alongside their Social Security Number.

- Write down the address and daytime phone number of the Executor/Administrator/Heir-at-Law.

- Under the "Mailing Address to send all correspondence" section, reiterate the name, street address, city, state, zip code, and daytime phone number where all correspondence should be sent.

- Select whether you are requesting an extension for the Inheritance Tax Return, the Estate Tax Return, or both. Then, specify the number of months the extension is requested for, adhering to the maximum period allowed for each type of return.

- Acknowledge that an extension to file does not extend the time to pay any taxes due, and understand that interest accrues on any unpaid taxes after their respective deadlines.

- Read and sign the certification statement, confirming that all information provided is true and correct to the best of your knowledge. The Executor/Administrator/Heir-at-Law or Estate Representative should sign and date here.

- Lastly, mail the completed form to the State of New Jersey, Division of Taxation, Individual Tax Audit Branch - Inheritance & Estate Tax, at the provided PO Box address in Trenton, NJ.

Remember, if your extension request is approved, you will not receive a confirmation unless the request is denied. It's therefore crucial to direct any queries regarding the status of your extension to the Division of Taxation directly, using the provided contact information. It’s important to take these steps diligently to ensure all paperwork is in order for the extension to be thoroughly processed and granted appropriately.

Learn More on Nj Estate

What is the NJ Estate Form IT-EXT?

The NJ Estate Form IT-EXT is an application utilized by the New Jersey Division of Taxation. It is specifically designed for requesting an extension of time to file an Inheritance and Estate Tax Return. This form is necessary when the executor, administrator, or heir-at-law of a deceased individual's estate needs additional time beyond the original filing deadline to prepare and submit the required tax returns.

When are Inheritance and Estate Tax Returns due in New Jersey?

Inheritance Tax Returns are due 8 months following the decedent's date of death. For Estate Tax Returns filed without using the Form 706 method, the due date is 9 months after the decedent's date of death. However, returns filed using the Form 706 method have a due date of 9 months plus 30 days after the decedent's death.

How long can the filing extension be for Inheritance and Estate Tax Returns?

Inheritance Tax Return extensions can initially be requested for up to 4 months beyond the original due date, with the possibility of a further 2-month extension, totaling 6 months. Estate Tax Return extensions can be requested for up to 6 months beyond the initial due date. Extensions beyond these periods are only granted under exceptional circumstances as determined by the Director.

Does requesting an extension for filing also extend the time for tax payments?

No, requesting an extension of time to file does not extend the time for making tax payments. Interest starts accruing on any unpaid Inheritance Tax due from 8 months after the decedent's date of death and on any unpaid Estate Tax from 9 months after the decedent's date of death, based on the applicable laws.

Will the estate receive delinquent notices if an extension is granted?

Yes, even with an extension, the estate may still receive computer-generated delinquent notices. An extension only delays the filing deadline; it does not impact notices related to unpaid taxes or other compliance reminders from the state.

What information is needed to complete Form IT-EXT?

The following information is required on the NJ Estate Form IT-EXT:

- Decedent's name and Social Security Number

- Date of death and county of residence

- Name, Social Security Number, address, and daytime phone number of the executor, administrator, or heir-at-law

- Mailing address for correspondence

- Whether an extension is requested for the Inheritance or Estate Tax Return, including the number of months requested

How is the NJ Estate Form IT-EXT submitted?

The completed form should be mailed to the State of New Jersey, Division of Taxation, Individual Tax Audit Branch - Inheritance & Estate Tax at the provided PO Box in Trenton, NJ. It is important to ensure that the form is fully completed and signed under the penalties of perjury, attesting to the accuracy of the information provided.

Will I receive confirmation of the extension request?

Requests for extensions do not receive a reply unless the request is denied. The form has sections for use by the Division of Taxation to indicate whether the extension has been approved or not, including any reasons for denial or other comments. It is recommended to keep a copy of the submitted form and any related correspondence for your records.

Common mistakes

Filling out the New Jersey Estate Form, also known as the IT-EXT form for the Division of Taxation - Inheritance and Estate Tax Application for Extension of Time to File A Return, requires careful attention to detail. Mistakes can lead to delays or issues with the processing of the application. Here are some common mistakes people make:

- Incorrect or Incomplete Decedent Information: The form requires detailed information about the decedent, including their full name, Social Security Number, and date of death. Leaving out any part of this information, or entering incorrect data, can lead to processing delays. It is crucial to double-check these details for accuracy.

- Failure to Indicate the Type of Tax Return Extension: The form allows for the request of an extension for either the Inheritance Tax Return or the Estate Tax Return, or both. Applicants sometimes overlook or fail to clearly indicate the specific extension or extensions they are requesting. It is imperative to mark the appropriate box to avoid confusion and ensure the request is processed correctly.

- Not Understanding the Extension Periods: There are different extension periods for Inheritance Tax Returns and Estate Tax Returns. An extension for the Inheritance Tax Return can initially be requested for up to 4 months, with the possibility of a further 2-month extension. For the Estate Tax Return, an extension can be requested for up to 6 months. Misunderstanding these periods can result in requesting an inappropriate extension length, potentially leading to penalties for late filing.

- Omitting Signature and Date: The form requires certification from the Executor, Administrator, Heir-at-Law, or Estate Representative that the information provided is true and correct, under penalties of perjury. Sometimes, individuals forget to sign and date the form. This oversight can invalidate the request for an extension, as an unsigned form is not considered legally submitted.

To avoid these and other potential mistakes, it is advised to read the form instructions carefully, verify all provided information for accuracy, and ensure that all required sections are completed fully and correctly. Doing so will help in the seamless processing of the extension request.

Documents used along the form

When handling an estate in New Jersey, the filing of the NJ Estate form, specifically the IT-EXT form for an extension of time to file the inheritance and estate tax return, is a critical step for executors, administrators, or heirs-at-law. It's important to note that this form is part of a suite of documents that are often prepared and filed in conjunction with managing an estate. Recognizing and understanding these associated documents can streamline the process, ensure compliance with legal requirements, and potentially mitigate the financial liabilities of the estate and its beneficiaries.

- Last Will and Testament: This legal document outlines the decedent's wishes regarding the distribution of their property and the care of any minor children. It names an executor responsible for carrying out these wishes.

- Death Certificate: A certified document issued by the government that officially declares the cause, date, and place of a person's death. It is required for many transactions related to closing out an estate.

- Inventory of Assets: A comprehensive list of the decedent's assets at the time of death, including real estate, stocks, bonds, personal property, and other financial assets. This helps in determining the estate's value for tax and distribution purposes.

- Appraisal Reports: Professional evaluations of valuable items, such as real estate, antiques, and jewelry, to determine their fair market value for equitable distribution and tax calculations.

- Trust Documents: If the decedent had established any trusts, these documents outline the terms, trustees, and beneficiaries of those arrangements. Trusts might have separate tax implications and filing requirements.

- Life Insurance Policies: Documents indicating the beneficiaries of any life insurance proceeds, which may or may not be subject to estate and inheritance taxes, depending on ownership and beneficiary arrangements.

- Debts and Liabilities Record: A record of any outstanding debts or liabilities of the decedent, including mortgages, personal loans, and credit card debts, which must be settled by the estate.

- Tax Returns: Copies of the decedent’s recent federal and state income tax returns to help determine any outstanding tax liabilities and the estate's fiscal requirements.

Each of these documents plays a significant role in the comprehensive and lawful management of an estate. Together, they help ensure that the estate is settled accurately, beneficiaries receive their due inheritances, and all tax obligations are met. Professional guidance from an estate or tax attorney, in conjunction with these documents, can provide clarity and ease during what is often a complex and emotionally difficult time.

Similar forms

The New Jersey Estate Form, specifically designed for requesting an extension of time to file inheritance and estate tax returns, shares similarities with the Federal Estate Tax Extension Form 4768. Both forms are used to request additional time for filing estate-related tax returns post the decedent's death. The federal form 4768 is applied to grant extensions for filing Form 706 and paying any federal estate taxes due, mirroring the state-level purpose of the New Jersey Estate Form in addressing the timing of estate and inheritance tax obligations.

Comparable to a Power of Attorney Form, the New Jersey Estate Form authorizes actions on behalf of another person – in this case, the estate of a deceased individual. While the Power of Attorney grants a broad or limited range of legal powers to act on behalf of another in financial, health, or legal matters, the NJ Estate Form specifically authorizes the executor, administrator, or heir to request an extension for filing necessary tax documents related to the estate, highlighting a more narrowed scope of authorized action.

Similar to a Last Will and Testament, which details the wishes of an individual regarding the distribution of their estate upon death, the New Jersey Estate Form plays a significant role in the estate settlement process. Though the Estate Form's purpose is to request an extension for filing taxes and does not distribute assets, it is integral to the administration of the decedent’s estate, ensuring compliance with tax obligations to avoid penalties.

The NJ Estate Form is akin to the IRS Form 4868, which is an Application for Automatic Extension of Time To File U.S. Individual Income Tax Return. Both forms serve the purpose of requesting additional time to file certain tax returns. However, while Form 4868 applies to individual income taxes, the NJ Estate Form is specific to inheritance and estate tax filings, focusing on the obligations of an estate rather than those of a living individual taxpayer.

It also has parallels with an Executor’s Deed, which is used to transfer property title from the estate to another party. Although the NJ Estate Form doesn’t transfer property, both documents are crucial in the administration of an estate. The Executor’s Deed finalizes the distribution of assets as per the decedent’s will or state law, while the Estate Form ensures the estate's compliance with tax filing deadlines during this process.

The Notice of Probate of Will is another document related to the New Jersey Estate Form, as both are steps in the probate process. The Notice of Probate informs interested parties that the will has been admitted to probate, initiating the estate administration process. In contrast, the Estate Form deals with the financial aspect of the process, specifically extending the deadline for filing taxes due from the estate, elucidating the administrative obligations following death.

Likewise, the Affidavit of Surviving Spouse resembles the NJ Estate Form in its function to ease the administrative burdens following a death. While the affidavit is used by the surviving spouse to assert rights to certain assets or benefits, the NJ Estate Form assists in managing the estate's tax-related responsibilities, both facilitating aspects of asset management and transition post-death.

The Trustee’s Deed, similar to the Executor’s Deed, is used for transferring titles of property held in a trust. In parallel, the New Jersey Estate Form is part of the broader administration and legal tasks necessary when handling an estate, focusing specifically on tax filing deadlines. Both are integral in the orderly transfer and management of assets, though the Trustee’s Deed and the NJ Estate Form cater to different elements of these proceedings.

Comparable to the Change of Beneficiary Form commonly used in insurance and retirement accounts, the New Jersey Estate Form plays a significant part in the administrative aftermath of an individual's death. While the Change of Beneficiary Form facilitates the transfer of benefits following the policyholder's or account holder's demise, the NJ Estate Form addresses the timely filing of taxes, underscoring the procedural necessities that follow a death.

Similarly, the Application for Federal Employment Identification Number (EIN) can be likened to the NJ Estate Form. After an individual’s death, obtaining an EIN is often necessary for the estate or trust, allowing it to conduct financial transactions. The NJ Estate Form, while aimed at securing more time to fulfill tax obligations, coincides with the moment in estate management when such identifiers are crucial for legal and financial proceedings.

Dos and Don'ts

Completing the New Jersey Estate Form (IT-EXT) accurately is crucial for securing an extension of time to file the necessary inheritance and estate tax returns. Here are key guidelines on what you should and shouldn't do during this process:

Do:

Review the application carefully before you begin to ensure you understand all requirements.

Include the decedent’s full name, social security number, and the date of death exactly as they appear in other official documents.

Clearly state whether the decedent died testate (with a will) or intestate (without a will).

Provide accurate contact information for the executor, administrator, or heir-at-law, including a daytime phone number and mailing address for correspondence.

Request the specific number of extension months needed for both the Inheritance and Estate Tax returns, keeping in mind the maximum extension periods allowed.

Sign the certification section to affirm that the information provided is true and correct to the best of your knowledge and belief.

Don't:

Leave any section of the form blank. Incomplete forms can result in processing delays or denial of the extension request.

Forget that an extension to file does not extend the time to pay any taxes due. Interest will accrue on unpaid taxes after the original due dates.

Overlook the need to state whether the estate is using the inheritance tax return extension, estate tax return extension, or both on the same form.

Miss the certification at the bottom of the form, as failing to sign can invalidate your request.

Assume that an extension will stop delinquent notices. The estate may still receive notices even if an extension is granted.

Send the form to the wrong address. It must be mailed to the State of New Jersey, Division of Taxation, Individual Tax Audit Branch - Inheritance & Estate Tax at the specified PO Box in Trenton, NJ.

Following these guidelines diligently will enhance the success of your extension application and help avoid common pitfalls that can delay processing or lead to penalties.

Misconceptions

When dealing with the New Jersey Estate form, specifically the IT-EXT form used for applying for an extension of time to file an Inheritance and Estate Tax return, there are several misconceptions that can complicate the process for executors, administrators, heirs, or general inquirers. Understanding these misconceptions is crucial for efficiently navigating estate planning and tax responsibilities in New Jersey.

Misconception 1: Extensions for Filing Automatically Extend the Payment DeadlineOne common misunderstanding is the belief that obtaining an extension to file the Inheritance or Estate Tax return also extends the deadline for any tax payments due. However, the reality is that the extension only applies to the filing of the return itself. Tax payments are due 8 months after the decedent's death for Inheritance Tax and 9 months after for Estate Tax. Interest accrues on any unpaid tax from these dates, regardless of any filing extension.

Misconception 2: Extension Requests Always Get ApprovedAnother misconception is that extension requests are always granted. While it may be common to receive an extension, approval is not automatic. Extensions beyond the initial periods (4 months for Inheritance Tax, 6 months for Estate Tax) are only given under exceptional circumstances as determined by the Director of the New Jersey Division of Taxation. Without sufficient justification, an extension request may be denied.

Misconception 3: Separate Forms Required for Inheritance and Estate Tax ExtensionsMany believe that separate forms need to be submitted to request an extension for filing the Inheritance Tax return and the Estate Tax return. The IT-EXT form simplifies this process by allowing requests for both types of extensions to be made on a single form. This streamlines the application process, saving time and reducing paperwork.

Misconception 4: The Estate Will Not Receive Notices if an Extension is GrantedThere is a misconception that once an extension is granted, the estate will not receive any delinquent notices. Even with an extension, the estate may still receive computer-generated notices if taxes are overdue. It's important to track deadlines and ensure payments are made to avoid these notices, as the extension only covers the filing of the tax return, not the payment of taxes.

Misconception 5: All Extensions are the Same LengthLastly, it's often assumed that all extensions are of the same duration. However, the initial extension period can vary: up to 4 months for the Inheritance Tax return and up to 6 months for the Estate Tax return. Further, any additional extension beyond these initial periods requires explicit approval from the Director, and is only granted in cases of exceptional circumstances.

Understanding these nuances of the IT-EXT form and the process for requesting filing extensions for New Jersey's Inheritance and Estate Tax can significantly ease the administrative burden on those managing an estate. It ensures the proper steps are taken to comply with state tax obligations, avoiding unnecessary complications or penalties.

Key takeaways

Filling out the New Jersey Estate Form, specifically the IT-EXT form, is a critical process for executors, administrators, or heirs tasked with the management of a decedent's financial obligations. Here are ten key takeaways that can help understand and navigate this process more efficiently.

- The form is used to request an extension of time to file either the Inheritance Tax Return or the Estate Tax Return in New Jersey.

- Decedent’s information, including full name, Social Security Number, and date of death, is essential to complete the form appropriately.

- The form distinguishes between cases where the decedent died with a will (testate) or without a will (intestate), which impacts the tax and legal proceedings.

- Identification of the executor, administrator, or heir-at-law, which includes providing their name, Social Security Number, and contact information, is mandatory for the filing process.

- It is critical to specify the type of tax return extension being requested – Inheritance Tax or Estate Tax, as the form caters to both but has distinct deadlines and extension limits.

- The original due date for Inheritance Tax returns is eight months following the decedent's death, with the possibility of requesting an initial extension of up to four months.

- For Inheritance Tax, if circumstances prevent filing within the initial four-month extension, a further extension of two months might be available, maxing extension requests to six months.

- Estate Tax returns have a slightly different timeline, with the original due date being nine months post the decedent’s death, and a possible extension up to six months.

- Payment obligations are not deferred with an extension request; interest accrues on any unpaid tax due from the original payment deadline specified by the law.

- Even with an approved extension, the estate might receive automated delinquent notices, indicating the separation of extension approval from actual payment status and obligations.

- Completing and submitting the form requires a declaration under penalty of perjury confirming the accuracy of the provided information, underscoring the seriousness of the document.

It's important to note that obtaining an extension to file does not alleviate the estate's obligation to eventually fulfill both the filing and the payment requirements. Prompt and accurate completion of the IT-EXT form can prevent unnecessary complications and ensure legal compliance during what is often a challenging time for executors and families.

Popular PDF Documents

How to Get a Police Report Nj - Promotes fairness and non-discrimination in state contracting, aligning with broader social justice goals.

Last Will and Testament Template New Jersey - Facilitate a stress-free management of your estate with this New Jersey Will template, covering everything from debts to bequests.

Nj Annulment Forms Pdf - The form is a crucial step in the legal process, ensuring defendants are properly informed of lawsuits against them.