Fill Out a Valid Nj L 9 Template

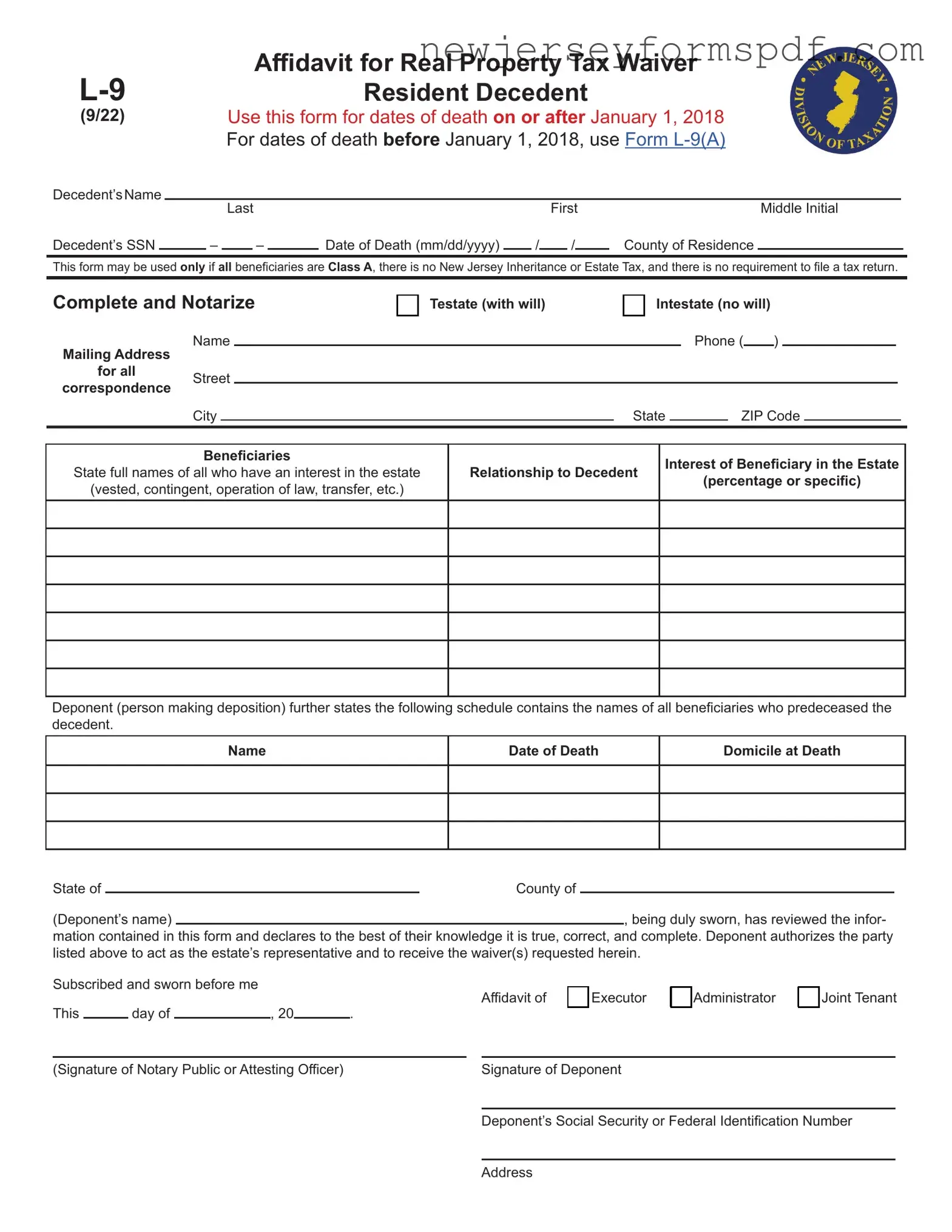

Inheriting property and settling the affairs of a loved one in New Jersey can present an intricate process, especially when it concerns dealing with the decedent's real estate and tax matters. The NJ L-9 Form, officially titled "Affidavit for Real Property Tax Waiver: Resident Decedent," serves as a crucial document in these circumstances, provided the death occurred on or after January 1, 2018. Designed for the executor, administrator, or joint tenant of the property to complete, the form's primary use is to request a waiver for real property taxes. It's eligible for use only if the estate benefits Class A beneficiaries, which include a spouse or civil union partner, children (and their descendants), parents, stepchildren, and domestic partners registered on or after July 10, 2004. However, its applicability is restricted under certain conditions, such as when property is jointly owned with a surviving spouse or if assets valued over $500 are passed outside these Class A beneficiaries. Additionally, the form mandates the submission of supporting documents, including the decedent's will, a copy of the property deed, and death certificate, emphasizing its role not as a tax waiver itself but as an affidavit to facilitate the waiver process. Filing it requires direct submission to the New Jersey Division of Taxation, specifically the Inheritance and Estate Tax Branch. This form underscores the importance of correctly navigating New Jersey's inheritance and estate tax requirements to ensure the smooth transition of property ownership while also fulfilling legal obligations.

Sample - Nj L 9 Form

(9/22)

Decedent’sName

Decedent’s SSN

Affidavit for Real Property Tax Waiver

Resident Decedent

Use this form for dates of death on or after January 1, 2018

For dates of death before January 1, 2018, use Form

|

Last |

|

|

|

|

First |

|

Middle Initial |

|||

– |

|

– |

|

Date of Death (mm/dd/yyyy) |

|

/ |

|

/ |

|

County of Residence |

|

This form may be used only if all beneficiaries are Class A, there is no New Jersey Inheritance or Estate Tax, and there is no requirement to file a tax return.

Complete and Notarize

Name

Mailing Address

for all Street correspondence

City

Testate (with will) |

|

Intestate (no will) |

|

|

|

Phone ( )

State |

|

ZIP Code |

Beneficiaries |

|

Interest of Beneficiary in the Estate |

|

State full names of all who have an interest in the estate |

Relationship to Decedent |

||

(percentage or specific) |

|||

(vested, contingent, operation of law, transfer, etc.) |

|

||

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Deponent (person making deposition) further states the following schedule contains the names of all beneficiaries who predeceased the decedent.

|

|

Name |

|

Date of Death |

|

Domicile at Death |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

State of |

|

|

|

County of |

|

|

|

|

(Deponent’s name) |

|

|

|

|

, being duly sworn, has reviewed the infor- |

|

||

mation contained in this form and declares to the best of their knowledge it is true, correct, and complete. Deponent authorizes the party listed above to act as the estate’s representative and to receive the waiver(s) requested herein.

Subscribed and sworn before me |

|

|

. |

|

Affidavit of |

|

Executor |

|

Administrator |

|

Joint Tenant |

||||

|

|

|

|

|

|

|

|

|

|

||||||

This |

|

day of |

|

, 20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

(Signature of Notary Public or Attesting Officer) |

|

|

Signature of Deponent |

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Deponent’s Social Security or Federal Identification Number |

|||||||

Address

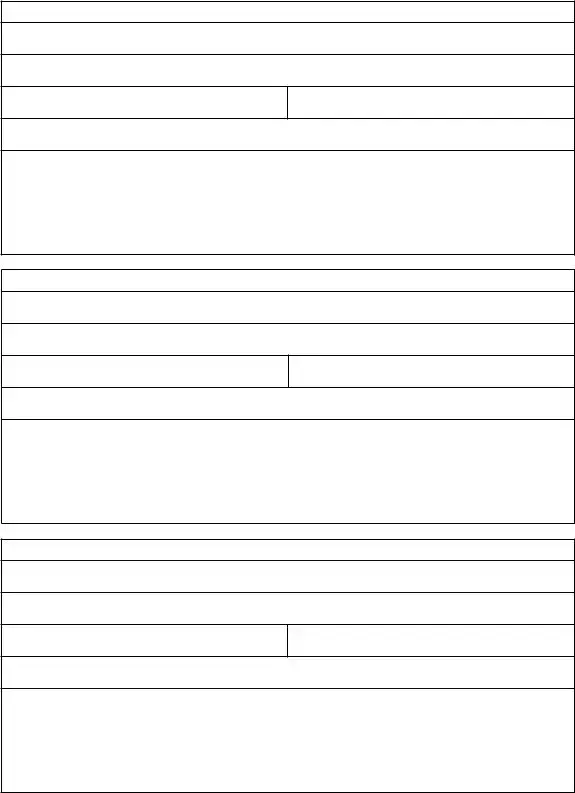

Description of New Jersey Real Estate

County

Street and Number

Lot

Block

Municipality

Owner(s) of Record (if decedent owned a fractional interest, state how held and fractional value thereof):

Description of New Jersey Real Estate

County

Street and Number

Lot

Block

Municipality

Owner(s) of Record (if decedent owned a fractional interest, state how held and fractional value thereof):

Description of New Jersey Real Estate

County

Street and Number

Lot

Block

Municipality

Owner(s) of Record (if decedent owned a fractional interest, state how held and fractional value thereof):

Riders may be attached when necessary

This form will be returned if it is not fully and properly completed and/or it does not have the required attachments.

Include all of the required documentation with this form:

•Copy of the decedent’s will, codicils and related writings, and any trust agreements;

•Copy of the deed for the property listed on the form;

•Copy of executor’s or administrator’s certificate (letters of testamentary or of administration);

•Copy of the decedent’s death certificate.

Form

This form can be completed by:

•The executor;

•Administrator; or

•Joint tenant of the property for which a waiver is requested.

Eligibility

All beneficiaries of this estate must be one of the following Class A beneficiaries:

•Spouse or civil union partner;

•Child (includes legally adopted child), grandchild,

•Parent or grandparent;

•

•Domestic partner (on or after 7/10/04).

You cannot use Form

•The real estate was held as “tenants by the entirety” (jointly by spouse/civil union partner) and the spouse/civil union partner is surviving.

Note: No waiver is needed for this property, and none will be issued;

•Any asset of the decedent valued at $500 or more passes to any beneficiary other than the Class A beneficiaries listed above;

•The relationship of a mutually acknowledged child is claimed to exist;

•There is any New Jersey Inheritance Tax or Estate Tax due.

Note: If a trust agreement either exists or is created by the will, the Division may require a full return should the terms of the trust indicate a possible Inheritance Tax. A waiver would not then be issued from this form.

Required Documents

•Copy of the decedent’s will, codicils and related writings, and any trust agreements;

•Copy of the deed for the property listed on the form;

•Copy of executor’s or administrator’s certificate (letters of testamentary or of administration);

•Copy of the decedent’s death certificate.

This form is not a tax waiver. Do not file with the County Clerk. Mail to:

Regular Mail and USPS Express Mail

NJ Division of Taxation

Transfer Inheritance Tax

PO Box 249

Trenton, NJ

Express Mail – Private Carriers (UPS, FedEx) NJ Division of Taxation

Transfer Inheritance Tax PO Box 249

3 John Fitch Way, 6th Floor Trenton, NJ 08611

For more information about the use of Form

Document Specifications

| Fact | Detail |

|---|---|

| Form Designation | Form L-9 is known as the Affidavit for Real Property Tax Waiver for resident decedents, applicable for deaths on or after 1/1/2018. |

| Eligible Applicants | The form can be filled out by the executor, administrator, or joint tenant of the property for which the waiver is requested. |

| Beneficiary Requirements | All beneficiaries must be Class A beneficiaries, which include spouse or civil union partner, child (including legally adopted children), parent, grandparent, step-child, and domestic partner (after 7/10/04). |

| Non-Eligibility Conditions | The form cannot be used if the real estate was held as “tenants by the entirety” with a surviving spouse/civil union partner, if any asset over $500 passes to non-Class A beneficiaries, a mutually acknowledged child is claimed, or there is any New Jersey Inheritance or Estate Tax due. |

| Required Documents | Applicants must attach a copy of the decedent’s will, codicils, trust agreements, property deed, executor’s or administrator’s certificate, and the decedent’s death certificate. |

Detailed Steps for Using Nj L 9

Upon the passing of an individual, certain steps are necessary to ensure the smooth transition of assets, including real property, to the rightful heirs without complication. Among these steps, the use of the NJ L-9 form, or Affidavit for Real Property Tax Waiver, is crucial for those instances where a New Jersey decedent's estate includes real property, and all beneficiaries are Class A. This form facilitates a waiver process required for the transfer of the decedent's real estate, under specific conditions, without the immediate need for further tax assessments. To navigate this process effectively, specific documentation must be gathered and accurately presented. The information provided must be verified and submitted to the New Jersey Division of Taxation in accordance with the guidelines set forth for estates with decedent's dates of death on or after 1/1/2018.

- Gather all required documents before beginning the form:

- Copy of the decedent’s will, codicils, related writings, and any trust agreements.

- Copy of the deed for the property listed on the form.

- Copy of the Executor’s or Administrator's certificate (letters testamentary or of administration).

- Copy of the decedent's death certificate.

- Fill in the decedent’s name (last, first, MI), Social Security Number, date of death, and county of residence at the top of the form.

- Indicate whether the decedent died testate (with a will) or intestate (without a will).

- Provide the mailing address to which all correspondence related to the form should be sent, including the name and phone number of the contact person.

- List all beneficiaries of the estate, their relationship to the decedent, and their interest in the estate (either as a percentage or specific).

- Include a schedule of any beneficiaries who predeceased the decedent, noting their names, dates of death, and their domicile at death.

- The deponent (the person making the deposition) should review the filled form, ensuring all information provided is true, correct, and complete to the best of their knowledge. The deponent authorizes the named party to act as the estate's representative and to receive the requested waiver(s).

- Have the form subscribed and sworn before a Notary Public or Attesting Officer on the provided space, indicating the day and year.

- The deponent must sign the form and include their Social Security number or Federal Identification number and address.

- Complete the section describing the New Jersey real estate involved, including the county, street and number, lot and block, municipality, and the owner(s) of record. If the decedent owned a fractional interest, state how it was held and the fractional value thereof. If there are multiple properties, ensure each is listed with complete details.

- Ensure that riders are attached if necessary for additional information.

- Review the entire form and attached documents to ensure they are fully and properly completed. This form will be returned if not accurately filled or if required attachments are missing.

- Mail the completed form along with all required documentation to the NJ Division of Taxation Inheritance and Estate Tax Branch at the provided address. Do not file this form with the County Clerk.

It is important to note, this form is integral in the administrative process following a decedent's death, where transfer of real property ownership within New Jersey is concerned. Its accurate completion and submission, paired with the necessary supporting documents, streamline the waiver process, effectively communicating with the New Jersey Division of Taxation to adhere to state tax laws. Obtaining further advice or clarification from the Inheritance and Estate Tax Branch, or consulting their website, is advisable for individuals navigating this process to ensure compliance and the successful transfer of the decedent's real property to their beneficiaries.

Learn More on Nj L 9

What is Form L-9 and who needs to use it?

Form L-9, known as the Affidavit for Real Property Tax Waiver, is a document used in New Jersey for estates where the deceased was a resident and died on or after January 1, 2018. Executors, administrators, or joint tenants of a property can use this form to request a waiver for real property tax. This form is applicable only if all beneficiaries are Class A beneficiaries, there's no New Jersey Inheritance or Estate Tax due, and there's no requirement to file a tax return for the estate.

Who qualifies as Class A beneficiaries?

Class A beneficiaries include the spouse or civil union partner, child (including legally adopted child), grandchild, great-grandchild, parent, grandparent, step-child (but not step-grandchildren), and domestic partner (relationships recognized on or after July 10, 2004).

When should you not use Form L-9?

The form should not be used under several conditions, including when the real estate was held as "tenants by the entirety" and the spouse/civil union partner is surviving; if any asset of the decedent valued at $500 or more passes to non-Class A beneficiaries; a mutually acknowledged child relationship is claimed; or if there's any New Jersey Inheritance Tax or Estate Tax due on the estate.

What documents are required to submit along with Form L-9?

- Copy of the decedent's will, codicils, related writings, and any trust agreements.

- Copy of the Deed for the property listed on the form.

- Copy of Executor's or Administrator's certificate (letters of testamentary or of administration).

- Copy of the decedent's death certificate.

How and where do you file Form L-9?

Do not file Form L-9 with the County Clerk. Instead, mail the completed form and required documents to the NJ Division of Taxation Inheritance and Estate Tax Branch at the address provided on the form. The form must be fully and properly completed with all required attachments included.

Can this form be obtained and reproduced online?

Yes, the Form L-9 can be obtained from the New Jersey Division of Taxation website and may be reproduced in its entirety. Ensure that the latest version of the form is used for processing.

What should you do if you have questions about using Form L-9?

If any questions arise regarding the use of Form L-9, it's recommended to call the Inheritance and Estate Tax Branch of the NJ Division of Taxation at their provided contact number or visit their website for detailed information and guidance.

Common mistakes

Filling out the NJ L-9 Form, an Affidavit for Real Property Tax Waiver, is a critical step for those handling the estate of a person who has passed away in New Jersey. This form is specifically for situations where the decedent was a resident of New Jersey, died on or after January 1, 2018, and the estate's real property is to be transferred without the need for an Inheritance Tax Waiver from the State. For a smooth process, it's essential to avoid common mistakes. Here are six frequently encountered errors:

Not verifying eligibility first: Before filling out the form, it's crucial to ensure all beneficiaries fall into the Class A category, as defined by the State of New Jersey. This includes spouse, child (including legally adopted children), grandchild, parent, step-child (but not step-grandchildren), and domestic partner (after July 10, 2004). If the property is to pass to anyone outside these categories, this form is not applicable.

Overlooking the completeness of required documents: The form requires several attachments, including a copy of the decedent’s will (if applicable), the deed of the property, executor’s or administrator’s certificate, and the decedent’s death certificate. Not attaching every required document can lead to the rejection of the form.

Inaccurate property descriptions: When describing New Jersey real estate on the form, precision is key. This includes the correct county, street address, lot and block, and municipality. If the decedent owned only a fractional interest in the property, this should be clearly stated along with the fraction's numerical value.

Failure to fully list all beneficiaries: The form asks for detailed information about all beneficiaries, including their full names, relationship to the decedent, and their interest in the estate. Omitting a beneficiary or not correctly detailing their interest can cause issues.

Sending the form to the wrong address: Despite thorough completion, mailing the form to an incorrect address will result in delays. It should be sent to the NJ Division of Taxation, Inheritance and Estate Tax Branch, at the address provided on the form, not to the County Clerk.

Not acknowledging the trust agreement clause: If a trust agreement exists or was created by the will, and its terms might indicate a possible Inheritance Tax, a full return may be required instead of this form. Not addressing this when applicable can lead to the necessity of additional paperwork or even penalties.

Completing the NJ L-9 Form accurately and ensuring all requirements are met can significantly streamline the process of managing and distributing the estate's assets. Families and estate representatives are encouraged to approach this task with attention to detail and, when needed, seek professional guidance.

Documents used along the form

When dealing with estate matters, particularly in New Jersey, there are several documents and forms that often accompany the Form L-9 – Affidavit for Real Property Tax Waiver. This form is crucial for the decedent's estate, especially for exempting certain real property from the New Jersey Inheritance Tax under specified conditions. However, navigating through the entire process comprehensively usually involves more than this single form. Let's take a brief look at some of these additional forms and documents, which play a vital role in the whole procedure.

- Form L-8 – Affidavit for Non-Real Estate Investments: Used alongside Form L-9 for assets that do not include real estate, such as bank accounts and stocks owned by the decedent.

- Form L-9(A) – Affidavit for Real Property Tax Waiver: For estates of individuals who died before 1/1/2018, providing similar information as the L-9 but applicable to earlier deaths.

- Death Certificate: An official document confirming the death, required for virtually all post-death transactions and filings.

- Will and Codicils: The last will and testament, along with any amendments, are critical for determining the distribution of assets.

- Executor’s or Administrator’s Certificate (Letters of Testamentary or of Administration): This document authorizes an individual to act on behalf of the deceased's estate.

- Copy of the Deed for the Property: Essential for establishing ownership of the property listed on the Form L-9.

- New Jersey Inheritance Tax Return (Form IT-R): Required if the estate owes inheritance tax, which Form L-9 seeks to waive for specific real properties.

- New Jersey Estate Tax Return (Form IT-Estate): Required for estates that exceed a certain value threshold, determining the estate tax due to New Jersey.

- Trust Agreements: If the decedent had established any trusts, copies of these agreements must be included to understand the complete distribution and taxation implications.

Understanding each document's role in estate management ensures a smoother process for executors, administrators, or joint tenants handling the affairs of a decedent. Proper completion and submission of these documents, along with the Form L-9 when applicable, are critical steps in settling an estate according to New Jersey's legal framework. This effort helps to ensure that all financial and legal obligations are met, and the rightful beneficiaries receive their due inheritance with the minimum possible tax burden.

Similar forms

The Form L-9 for New Jersey shares similarities with the IRS Form 706, United States Estate (and Generation-Skipping Transfer) Tax Return. Both are used in the context of a decedent's estate, but where Form L-9 is geared towards a waiver for real property tax for New Jersey residents, Form 706 focuses on reporting the value of the entire estate for federal estate tax purposes. Like the L-9, Form 706 requires detailed information about the decedent and their estate, including beneficiaries and their relationships to the decedent, but it also involves calculating tax due on the estate's transfer of wealth.

The New Jersey Inheritance Tax Return is another document with objectives akin to those of Form L-9. It too deals with the aftermath of a person's death, evaluating assets for tax purposes. However, the focus here is on the inheritance tax, levied based on the value of specific assets passed to beneficiaries. Similar to the L-9, which necessitates the identification of Class A beneficiaries to determine eligibility for a tax waiver, the New Jersey Inheritance Tax Return requires detailed listings of all bequeathed assets and their recipients, determining tax based on the beneficiaries' relation to the decedent.

The Affidavit of Surviving Spouse or Domestic Partner in New Jersey is equally intended to assist with the settling of estates, specifically by enabling the transfer of assets to a surviving spouse or partner without the need for a formal probate process. This document closely parallels the L-9 in its attempt to simplify the legal aftermath of death, focusing on facilitating asset transfer to close relatives, albeit through a different mechanism. Where the L-9 grants a tax waiver for real estate, the Affidavit directly supports the transfer of various assets by affirming the surviving spouse or partner's entitlement.

Form L-8, Affidavit for Non-Real Estate Investments: Resident Decedent, is similar to Form L-9 but applies to New Jersey decedent's assets other than real estate. Like L-9, L-8 is designed for use when the decedent leaves behind assets that need to be transferred to beneficiaries; however, it concentrates on investments such as stocks and bonds. Both forms require that all beneficiaries be Class A and that no New Jersey Inheritance or Estate Tax is due, streamlining the process by which assets are passed on without the necessity for full probate or tax proceedings.

The Small Estate Affidavit, used across various jurisdictions, including New Jersey, serves a purpose comparable to that of Form L-9 by allowing for a simpler, faster means of asset transfer from a decedent to their heirs. This affidavit can be utilized when the total value of the estate falls below a certain threshold, indicating that formal probate may be unnecessary. Though it covers a broader spectrum of assets than the real estate-specific L-9, both documents facilitate the bypassing of more cumbersome legal processes for heirs under specific conditions.

Finally, the Transfer on Death (TOD) deed, recognized in some states, also shares a conceptual similarity to New Jersey's Form L-9. While not applicable in New Jersey, a TOD deed allows property owners to designate beneficiaries to whom the property will automatically transfer upon their death, bypassing the probate process. Although serving different legal functions, with the TOD focusing on pre-death designation and the L-9 on post-death tax waiver, both instruments streamline the transfer of real property to intended beneficiaries and mitigate potential legal and tax complications.

Dos and Don'ts

When dealing with the complexities of estate management, particularly in New Jersey, the correct handling of Form L-9, the Affididavit for Real Property Tax Waiver, is crucial. This form plays a pivotal role for those who are navigating the aftermath of a loved one's passing, aiming to ensure that real estate matters are handled smoothly and in accordance with state laws. To aid in this process, here are some key guidelines to follow, as well as common pitfalls to avoid.

Do's:

Verify the eligibility of all beneficiaries as Class A before proceeding. Class A beneficiaries include a spouse or civil union partner, children (including legally adopted children), parents, grandparents, stepchildren, and domestic partners (after 7/10/04). This step is paramount to ensure compliance with the eligibility requirements of Form L-9.

Gather all required documents before filling out the form. These include a copy of the decedent's will and any codicils, the deed for the property, the executor's or administrator’s certificate, and the decedent's death certificate. Having these documents at the ready will streamline the process.

Ensure accuracy in reporting the decedent's information, including their Social Security number and date of death. Accuracy in these details is essential for the form's acceptance and processing.

Complete the form in its entirety. This means filling out all sections and not leaving any area blank unless it is specifically mentioned as optional. An incomplete form can cause delays or rejection of the application for a waiver.

Attach any necessary riders if the real estate descriptions exceed the space provided in the form. This ensures that all properties are accounted for and adequately described, a step that cannot be overlooked for the waiver to be granted.

Notarize the form as required. The signature of the executor, administrator, or joint tenant, as well as that of the notary public, validates the form and is a mandatory step in the submission process.

Don'ts:

Do not file this form if the estate contains real estate held as "tenants by the entirety" and the spouse or civil union partner is surviving. No waiver is needed in such situations, and filing this form would be unnecessary.

Avoid using the form if any assets valued at $500 or more are passing to beneficiaries who are not classified as Class A. This condition disqualifies the estate from using Form L-9 for obtaining a tax waiver.

Do not claim a mutually acknowledged child relationship if intending to use this form—as this disqualifies the estate from its eligibility.

Do not file this form with the County Clerk, as it needs to be sent directly to the NJ Division of Taxation Inheritance and Estate Tax Branch. Misdirecting the form can result in processing delays.

Refrain from submitting the form without all the required attachments. Omission of the necessary documents, such as the death certificate or deed, will result in the form being returned.

Avoid making assumptions about the process or the information needed. When in doubt, it's advisable to seek clarification from the Inheritance and Estate Tax Branch or consult their website for additional guidance.

By following these guidelines, individuals can ensure that their submission of the NJ L-9 form is handled efficiently and accurately, facilitating a smoother process during a time that is often challenging for all involved.

Misconceptions

Understanding the NJ L-9 Form, the Affidavit for Real Property Tax Waiver, involves navigating through some common misconceptions. Here are six misconceptions that often arise:

- It’s a Tax Waiver Form: Despite its name, the L-9 isn't a tax waiver but an affidavit used to request a Real Property Tax Waiver from the New Jersey Division of Taxation for the estate of a deceased resident.

- Filing with the County Clerk: Some people mistakenly believe that this form should be filed with the County Clerk. However, the completed form, along with all required documents, should be sent directly to the NJ Division of Taxation, not the County Clerk.

- Eligibility Is Limited: There’s a misconception that the form is only for spouses or direct descendants. In truth, any Class A beneficiary, which includes spouses, civil union partners, children (including legally adopted children), grandchildren, parents, grandparents, step-children (but not step-grandchildren), and domestic partners (after 7/10/04), can use this form.

- Applicability for All Estates: Another common misunderstanding is that the L-9 form is applicable for all estates in New Jersey. It's specifically for estates where the deceased was a resident, all beneficiaries are Class A, there's no New Jersey Inheritance or Estate Tax due, and a tax return is not required.

- No Documentation Required: Contrary to what some believe, just filling out the form isn't enough. Required documents include a copy of the decedent’s will, codicils and related writings, any trust agreements, the deed for the property, the Executor’s or Administrator’s certificate, and the decedent’s death certificate.

- Use for Tenants by the Entirety: There's a false belief that this form is needed when real estate is held as “tenants by the entirety” (jointly by spouse/civil union partner) and the spouse or civil union partner is surviving. Actually, in such cases, no waiver is needed, and thus, the form would not be applicable.

Clarifications on these misconceptions can help in the proper completion and submission of the NJ L-9 form, ensuring that the request for a Real Property Tax Waiver is processed efficiently and accurately.

Key takeaways

Filling out and using the Form L-9 in New Jersey, known as the Affidavit for Real Property Tax Waiver, involves specific guidelines and criteria that must be carefully followed to ensure its successful submission and processing. Here are key takeaways to help understand and navigate this process effectively:

- Eligibility is strictly defined: The form is designed exclusively for estates where the decedent's date of death is on or after January 1, 2018, and all beneficiaries are identified as Class A beneficiaries. These include spouses or civil union partners, children (including legally adopted children), grandchildren, great-grandchildren, parents, grandparents, step-children (but not step-grandchildren), and domestic partners after July 10, 2004.

- Certain conditions disqualify the use of the form: The L-9 cannot be used if the real estate was held as “tenants by the entirety” with a surviving spouse or civil union partner, if any asset over $500 passes to non-Class A beneficiaries, if a mutually acknowledged child's relationship is claimed, or if any New Jersey Inheritance Tax or Estate Tax is due.

- Specific documents are required for submission: Along with the completed AFFIDAVIT, copies of the decedent's will, any codicils and related writings, deed for the listed property, and executor’s or administrator’s certificate are needed. Additionally, a copy of the decedent’s death certificate must be attached.

- This form is not a tax waiver itself and should not be filed with the County Clerk. Instead, it must be mailed directly to the New Jersey Division of Taxation, Inheritance and Estate Tax Branch.

- The role of the deponent is critical: The person completing the form, whether an executor, administrator, or joint tenant, must swear to the information's accuracy and completeness. This affidavit must be notarized to be valid.

- Clarity on real estate interests is essential: When listing New Jersey real estate holdings on the form, one must clearly describe each property, indicating how the decedent owned it (e.g., sole owner or as a fractional owner) and the fractional value thereof if applicable.

- Non-compliance or missing documents lead to rejection: The state will return forms that are incomplete or lack the required documentation. Ensuring all the necessary paperwork accompanies the L-9 form is crucial for its processing.

- Seeking guidance is encouraged: For questions or clarification, contacting the Inheritance and Estate Tax Branch of the New Jersey Division of Taxation or visiting their website is advised. This can help avoid common mistakes and ensure the process is handled correctly.

- Finally, reproducing this form in its entirety for personal records and reference is permissible, providing a way to maintain accurate and thorough estate files.

Understanding these key aspects of the Form L-9 can greatly assist in the efficient handling of an estate's real property tax matters in New Jersey, ensuring that all legal and procedural requirements are met.

Popular PDF Documents

Nj Reg - Available online, the NJ-REG form can be easily accessed and submitted electronically for convenience.

New Jersey Filing Requirements - Complete and accurate participant directories must be maintained for both those electing and those not eligible for the composite return.

Perc Website - Formal submission route for New Jersey public sector workers or unions aiming to adjust their representation or bargaining status.