Fill Out a Valid Nj Ttd Template

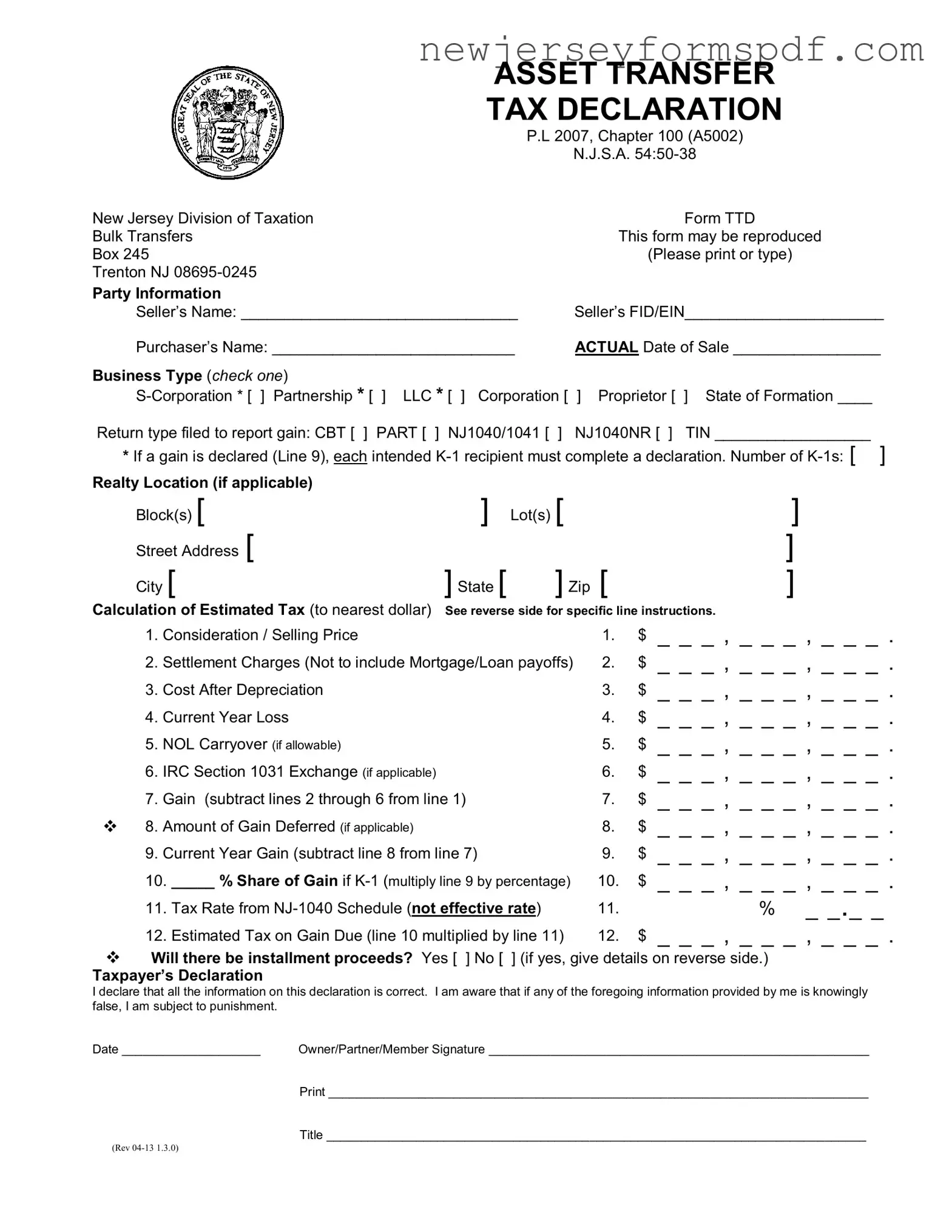

In the realm of business transactions within New Jersey, the Asset Transfer Tax Declaration, governed by P.L 2007, Chapter 100 (A5002) under N.J.S.A. 54:50-38, plays a pivotal role in ensuring the compliance of businesses with state tax obligations. This declaration, known formally as the Form TTD and facilitated by the New Jersey Division of Taxation, is crafted specifically for bulk transfer transactions and mandates meticulous reporting from both the seller and purchaser of business assets. Key components of the form include detailed party information, business type designation, and a nuanced calculation for the estimated tax on gains derived from the asset transfer. Significantly, the form delineates a comprehensive procedure for the payment of estimated taxes to be held in escrow at closing, ensuring that the transaction adheres to state tax laws and regulations. Moreover, it contains provisions for declaring the gain on the sale, the tax rate applicable, and the method for calculating taxes due, with considerations for installment proceeds and deferred gains. Importantly, the form also serves as a declaration by the taxpayer, attesting to the accuracy of the information provided under penalty of punishment for falsification. This pivotal document underscores the state's commitment to tax compliance and the integrity of business transactions, positioning itself as a cornerstone in the administrative process for the transfer of business assets in New Jersey.

Sample - Nj Ttd Form

|

ASSET TRANSFER |

||

|

TAX DECLARATION |

||

|

P.L 2007, Chapter 100 (A5002) |

||

|

|

N.J.S.A. |

|

New Jersey Division of Taxation |

|

|

Form TTD |

Bulk Transfers |

|

This form may be reproduced |

|

Box 245 |

|

(Please print or type) |

|

Trenton NJ |

|

|

|

Party Information |

|

|

|

Seller’s Name: ________________________________ |

Seller’s FID/EIN_______________________ |

||

Purchaser’s Name: ____________________________ |

ACTUAL Date of Sale _________________ |

||

Business Type (check one) |

|

|

|

] LLC * [ ] Corporation [ |

] Proprietor [ |

] State of Formation ____ |

|

Return type filed to report gain: CBT [ ] |

PART [ ] NJ1040/1041 [ ] |

NJ1040NR [ ] |

TIN __________________ |

* If a gain is declared (Line 9), each intended

Realty Location (if applicable) |

|

|

|

|

|

|

Block(s) [ |

] |

Lot(s) [ |

|

|

] |

|

Street Address [ |

|

|

|

|

] |

|

City [ |

] State [ |

] Zip [ |

|

] |

||

Calculation of Estimated Tax (to nearest dollar) |

See reverse side for specific line instructions. |

|||||

1. |

Consideration / Selling Price |

|

|

1. |

$ |

_ _ _ , _ _ _ , _ _ _ . |

2. |

Settlement Charges (Not to include Mortgage/Loan payoffs) |

2. |

$ |

_ _ _ , _ _ _ , _ _ _ . |

||

3. |

Cost After Depreciation |

|

|

3. |

$ |

_ _ _ , _ _ _ , _ _ _ . |

4. |

Current Year Loss |

|

|

4. |

$ |

_ _ _ , _ _ _ , _ _ _ . |

5. |

NOL Carryover (if allowable) |

|

|

5. |

$ |

_ _ _ , _ _ _ , _ _ _ . |

6. |

IRC Section 1031 Exchange (if applicable) |

|

|

6. |

$ |

_ _ _ , _ _ _ , _ _ _ . |

7. |

Gain (subtract lines 2 through 6 from line 1) |

|

7. |

$ |

_ _ _ , _ _ _ , _ _ _ . |

|

8. Amount of Gain Deferred (if applicable) |

|

|

8. |

$ |

_ _ _ , _ _ _ , _ _ _ . |

|

9. |

Current Year Gain (subtract line 8 from line 7) |

|

9. |

$ |

_ _ _ , _ _ _ , _ _ _ . |

|

10. _____ % Share of Gain if |

10. |

$ |

_ _ _ , _ _ _ , _ _ _ . |

|||

11. Tax Rate from |

11. |

|

% _ _._ _ |

|||

12. Estimated Tax on Gain Due (line 10 multiplied by line 11) |

12. |

$ |

_ _ _ , _ _ _ , _ _ _ . |

|||

Will there be installment proceeds? Yes [ ] No [ ] (if yes, give details on reverse side.)

Taxpayer’s Declaration

I declare that all the information on this declaration is correct. I am aware that if any of the foregoing information provided by me is knowingly false, I am subject to punishment.

Date ____________________ |

Owner/Partner/Member Signature _______________________________________________________ |

|

Print ______________________________________________________________________________ |

|

Title ______________________________________________________________________________ |

(REV |

|

N.J.S.A.

Procedure

The estimated tax on the gain portion of the escrow to be held at closing is initially calculated by multiplying the gross consideration by the tax rate of the taxpayer.

Upon completion of this declaration, submission to and review by the Division, the estimated tax on the gain portion of the escrow may be reduced appropriately.

Upon closing of the transaction, the escrow will be held by the transferee’s attorney and the estimated tax on the gain portion of the escrow will be demanded by the Division to be applied to the appropriate tax type and year. A confirmation of receipt and the application of the estimated tax payment will be sent to the transferor’s attorney.

The taxpayer files their year end business tax return, claims credit for the payment and pays any additional tax due. They may request a refund or credit if an overpayment exists.

Specific Line Instructions for Estimated Tax Calculation

Special Note: Lines 1 through 9 establish gain. Line 10 assigns share.

Line 1: Total sale price or consideration of all assets currently being transferred.

Line 2: Total amount of settlement charges to transferor associated with this transaction.

Line 3: If fully depreciated enter zero.

Line 8: Calculate amount deferred based on installment or short term notes.

Line 9: For NJ1065 filers: If any member/partner is not an individual or if the number of nonresident member/partners exceeds five (5) stop here and attach the most current membership directory. The Division will calculate and communicate the estimated tax for resident filers and/or withholding amount for nonresident filers.

Line 11: Individual tax rates may be found in the most current

Line 12:

•

•

This is the declared amount that the Division will demand from escrow to be applied to the taxpayer’s account(s).

Details of Installment proceeds:

_______________________________________________________________________

_______________________________________________________________________

_______________________________________________________________________

___________________________________________________________________

Document Specifications

| Fact Name | Description |

|---|---|

| Form Title | Asset Transfer Tax Declaration |

| Legislation | P.L 2007, Chapter 100 (A5002) N.J.S.A. 54:50-38 |

| Governing Body | New Jersey Division of Taxation |

| Form Code | TTD |

| Type of Form | Bulk Transfers |

| Usage | Used for declaring asset transfers and calculating the estimated tax on gained portion of escrow to be held at closing. |

| Important Section | The taxpayer's declaration section where the seller declares the correctness of the information and acknowledges the consequences of providing false information. |

| Procedure Highlight | The estimated tax on the gain from the asset transfer is calculated, and upon completion and review by the Division, the estimated tax may be adjusted accordingly. |

| Special Notes | Instructions for calculating estimated tax on the gain, including provision for installment proceeds and the demand from escrow upon meeting certain criteria. |

Detailed Steps for Using Nj Ttd

Filling out the NJ TTD form is a crucial step in the process of transferring business assets in New Jersey, ensuring that the estimated tax on the gain from the sale is calculated and paid. This form requires detailed information about both the seller and the purchaser, the nature of the business, and the financial specifics of the transaction. Careful attention to detail and accuracy in completing the form will facilitate smooth processing by the New Jersey Division of Taxation and help prevent any potential delays or issues. Following the instructions provided below will guide you through each step of filling out the form correctly.

- Start by entering the Seller’s Name and Federal ID Number (FID/EIN) in the designated sections.

- Next, fill in the Purchaser’s Name.

- Specify the ACTUAL Date of Sale.

- Select the type of business from the given options (S-Corporation, Partnership, LLC, Corporation, Proprietor) and mark the appropriate box.

- Enter the State of Formation for the business.

- Choose the return type filed to report the gain: CBR, PART, NJ1040/1041, or NJ1040NR and mark the correct box.

- If applicable, indicate the number of K-1s.

- Provide the Realty Location details if relevant, including block(s), lot(s), street address, city, state, and zip code.

- Under the Calculation of Estimated Tax section, fill in the numbers carefully:

- Enter the total Consideration / Selling Price.

- Fill in the Settlement Charges (excluding mortgage/loan payoffs).

- Specify the Cost After Depreciation; enter zero if fully depreciated.

- Note the Current Year Loss.

- Include any NOL Carryover if allowable.

- Indicate the amount for IRC Section 1031 Exchange if applicable.

- Calculate the Gain by subtracting lines 2 through 6 from line 1.

- Enter the Amount of Gain Deferred if applicable.

- Determine the Current Year Gain by subtracting line 8 from line 7.

- Calculate the % Share of Gain if K-1 (multiply line 9 by percentage).

- Find the Tax Rate from NJ-1040 Schedule and enter the percentage.

- Compute the Estimated Tax on Gain Due (line 10 multiplied by line 11).

- Answer whether there will be installment proceeds and provide details on the reverse side if applicable.

- Complete the Taxpayer’s Declaration by entering the date and signing your name along with your title. Print your name clearly.

Upon completion and submission of the NJ TTD form to the Division of Taxation, it will be reviewed, and the amount of estimated tax to be held in escrow at closing may be adjusted accordingly. The appropriate action will take place at the closing of the transaction where the escrow will be managed according to the Division’s direction. Following these steps ensures that the process moves forward smoothly. A confirmation will be sent once the estimated tax payment has been received and applied. Finally, the taxpayer should include this payment in their year-end tax return, where they can claim the payment and settle any remaining tax liability.

Learn More on Nj Ttd

What is the NJ TTD form?

The NJ TTD form, also known as the Asset Transfer Tax Declaration, is a document required by the New Jersey Division of Taxation under P.L 2007, Chapter 100 (A5002). Its main purpose is to declare the estimated tax due on the gain from the transfer of business assets. The form is used in bulk transfer situations to ensure compliance with state tax laws.

Who needs to fill out the NJ TTD form?

Any party involved in the bulk transfer of business assets in New Jersey, such as sellers or purchasers of a business, needs to complete this form. This includes S-Corporations, Partnerships, LLCs, Corporations, and Proprietors.

What information is required on the form?

The form requires detailed information about the parties involved in the transaction, including:

- Seller’s Name and FID/EIN

- Purchaser’s Name

- Actual Date of Sale

- Type of Business

- State of Formation

- Return type filed to report gain

- Realty Location (if applicable)

- Detailed calculation of the estimated tax on gain

How is the estimated tax calculated on the NJ TTD form?

The estimated tax is calculated by subtracting allowances such as settlement charges, cost after depreciation, current year loss, NOL carryover, and IRC Section 1031 Exchange (if applicable) from the total consideration or selling price. Then, the gain derived is used to determine the estimated tax owed.

Is an installation proceeds section included in the form?

Yes, the form includes a section to detail if there will be installment proceeds from the transfer. If applicable, specifics of these proceeds need to be provided on the reverse side of the form.

What happens after submitting the NJ TTD form?

After submitting the form, the New Jersey Division of Taxation reviews the estimated tax calculation. The estimated tax on the gain portion of the escrow held at closing may be adjusted. The escrow is then applied to the appropriate tax year and type upon closing. A confirmation of the estimated tax payment receipt and application is sent to the transferor’s attorney.

The NJ TTD form should be submitted as specified by the New Jersey Division of Taxation. It can typically be mailed to the provided address on the form, but always verify current submission guidelines with the Division or a tax professional.

What are the consequences of providing false information?

Individuals who knowingly provide false information on the NJ TTD form are subject to punishment, including potential fines and legal consequences. Accurate and truthful information must be declared to avoid such penalties.

Can the estimated tax payment be adjusted or refunded?

Yes, the taxpayer may file a year-end business tax return, claiming credit for the payment. If an overpayment exists, a refund or credit may be requested. Any additional tax due must also be paid at this time.

Where can I find the specific line instructions for the form?

Specific line instructions for estimated tax calculation are provided on the reverse side of the NJ TTD form. These instructions detail how to calculate the gain and the estimated tax payment correctly.

Common mistakes

When filling out the New Jersey Asset Transfer Tax Declaration, commonly known as the Form TTD, people often encounter pitfalls. Avoiding these mistakes is crucial for a smooth transaction process. Here are the top five errors to watch out for:

Incorrectly reporting the selling price or consideration: The total sale price or consideration for all assets being transferred must be accurately reported in Line 1. Overestimating or underestimating this figure can lead to incorrect tax estimations.

Omitting or inaccurately listing settlement charges: Line 2 requires the total amount of settlement charges associated with the transaction, excluding mortgage or loan payoffs. Failing to include these charges or listing them inaccurately can affect the calculation of the estimated tax.

Improper calculation of deferred gain: If applicable, the amount of gain deferred through installment or short-term notes must be calculated and reported on Line 8. Misinterpretation of this calculation can lead to incorrect tax obligations.

Not attaching necessary additional documentation: For NJ1065 filers, if any member or partner is not an individual or if the number of nonresident members or partners exceeds five, the process requires attaching the most current membership directory. Failure to include required documentation could delay processing.

Misunderstanding the tax rate and estimated tax due: Line 11 requires the tax rate from the NJ-1040 Schedule to be applied, which varies for corporations and individuals. Line 12 then calculates the estimated tax on gain due. Misinterpreting these instructions can lead to an incorrect tax payment.

Avoiding these errors requires careful reading of the form instructions and attention to detail. Ensuring the accurate completion of each line and including all necessary documentation will facilitate a smoother transaction and compliance with New Jersey tax obligations.

Documents used along the form

In the process of business transactions, especially those involving the transfer of assets, the NJ TTD form plays a crucial role by ensuring compliance with tax laws related to asset transfers. This document, titled the Asset Transfer Tax Declaration, necessitates the completion and submission of various other forms and documents to fully support and document the transaction comprehensively. Understanding these supplementary documents can provide clarity and ease the completion of the transaction process.

- Form A-3128: This is an Affidavit of Consideration for Use by Seller. It documents the amount of consideration involved in the real estate transaction, a requirement by New Jersey counties to record deeds.

- Form GIT/REP-1: Non-Resident Seller's Tax Declaration form is used when a non-resident of New Jersey sells or transfers real estate located in New Jersey, to declare tax withholdings related to the gain on the sale.

- Form GIT/REP-3: This Seller's Residency Certification/Exemption, essential for residents of New Jersey proving their residency status to exempt themselves from withholding tax at the time of a real estate sale.

- Form CBT-100: Corporation Business Tax Return for businesses operating as corporations, crucial for reporting the income, gains, losses, and taxable distribution of the corporate entity to the state of New Jersey.

- Form NJ-1065: Partnership Return, necessary when the seller is a partnership. This form reports the income, deductions, gains, and losses from the operation of a partnership.

- Form WR-30: Employer Report of Wages Paid. While not directly related to the sale of assets, if the business has employees, this form reports wage and tax information for each employee to the state.

- Form UC-2: Report Covering Employees Subject to Unemployment Insurance. Businesses must report their payroll and calculate unemployment insurance contributions for employees, an important aspect of business operations to be squared away during a transfer of ownership.

Completing and submitting these forms along with the NJ TTD form ensures that the transfer of assets is properly documented and in compliance with all applicable laws and regulations. The intersection of these documents with the transaction process emphasizes the importance of meticulous documentation and adherence to state requirements, ultimately facilitating a smooth transition and preventing legal and financial complications down the line.