Fill Out a Valid Nj W 3M Template

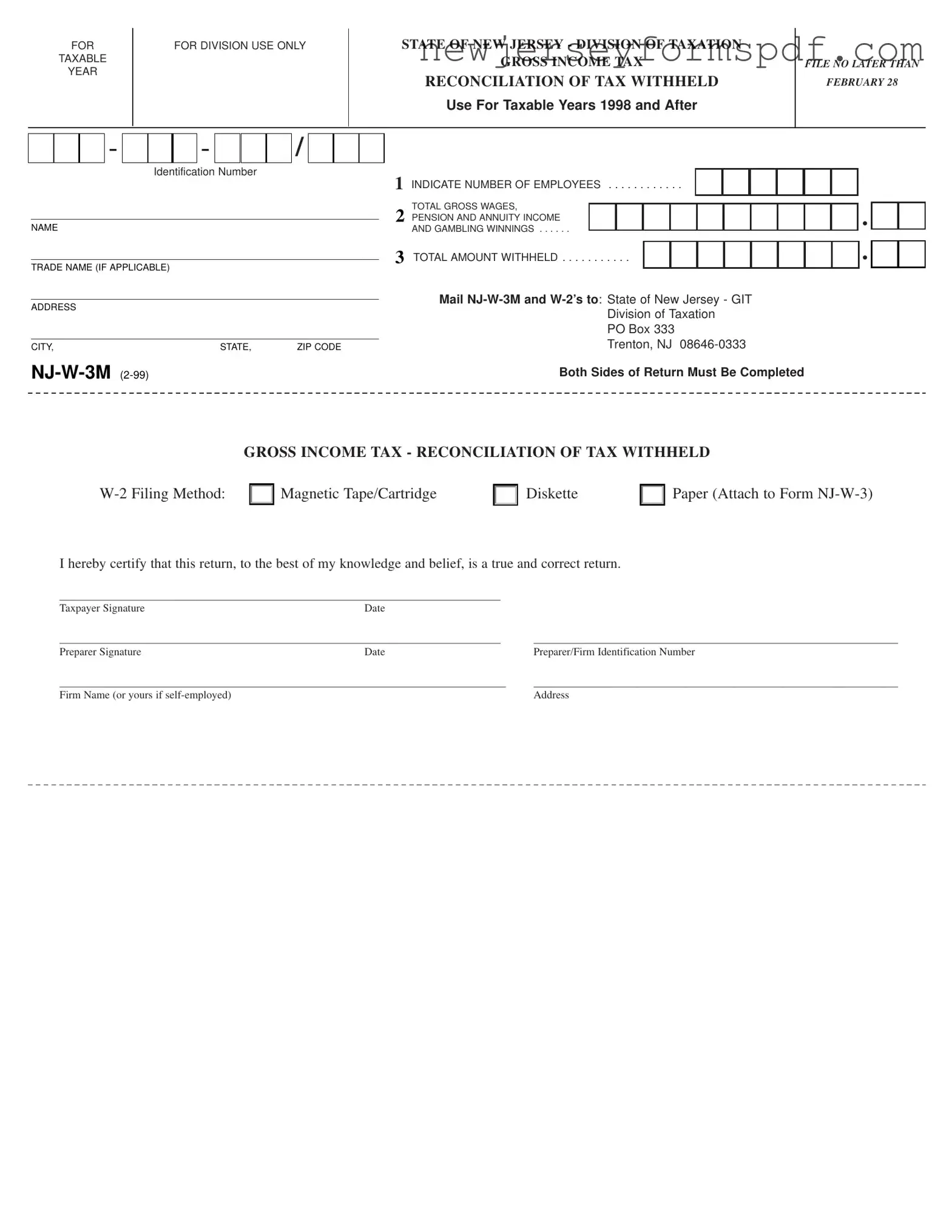

Understanding the intricacies of state tax forms is essential for individuals and business entities that deal with tax withholdings and salary disbursements in New Jersey. The NJ W-3M form, under the purview of the State of New Jersey Division of Taxation, serves a critical role in the process of gross income tax reconciliation for amounts withheld from employees' wages, pension and annuity income, and gambling winnings. Applicable for taxable years 1998 and thereafter, the NJ-W-3M must be filed no later than February 28 of the following year, ensuring that the state has a comprehensive record of the tax withheld by an employer or payer within the previous year. This form requires detailed information including the employer's or entity's name, address, trade name (if applicable), total number of employees, gross wages paid, total pension and annuity income, gambling winnings, and the total amount of tax withheld. Additionally, it outlines the method of W-2 filing—whether by magnetic tape/cartridge, diskette, or paper—and mandates certification by the taxpayer, confirming the accuracy and truthfulness of the submitted information. The completion of this form and its accurate submission, accompanied by W-2 forms for each employee, is not only a legal requirement but also a crucial step in ensuring proper tax practices and compliance with New Jersey state taxation laws.

Sample - Nj W 3M Form

FOR

TAXABLE

YEAR

FOR DIVISION USE ONLY

STATE OF NEW JERSEY - DIVISION OF TAXATION

GROSS INCOME TAX

RECONCILIATION OF TAX WITHHELD

Use For Taxable Years 1998 and After

FILE NO LATER THAN

FEBRUARY 28

- |

|

|

|

- |

|

|

|

/ |

|

|

Identification Number |

|

|

||||

___________________________________________________________________

NAME

___________________________________________________________________

TRADE NAME (IF APPLICABLE)

___________________________________________________________________

ADDRESS

___________________________________________________________________

CITY, |

STATE, |

ZIP CODE |

1 INDICATE NUMBER OF EMPLOYEES . . . . . . . . . . . .

TOTAL GROSS WAGES,

2 PENSION AND ANNUITY INCOME AND GAMBLING WINNINGS . . . . . .

3 TOTAL AMOUNT WITHHELD . . . . . . . . . . .

Mail

Division of Taxation

PO Box 333

Trenton, NJ

Both Sides of Return Must Be Completed

•

•

GROSS INCOME TAX - RECONCILIATION OF TAX WITHHELD

Magnetic Tape/Cartridge |

Diskette |

Paper (Attach to Form |

I hereby certify that this return, to the best of my knowledge and belief, is a true and correct return.

_________________________________________________________________________________ |

|

|

Taxpayer Signature |

Date |

|

_________________________________________________________________________________ |

___________________________________________________________________ |

|

Preparer Signature |

Date |

Preparer/Firm Identification Number |

__________________________________________________________________________________ |

___________________________________________________________________ |

|

Firm Name (or yours if |

|

Address |

Document Specifications

| Fact Name | Description |

|---|---|

| Purpose | The NJ-W-3M form is used for the Gross Income Tax Reconciliation of Tax Withheld in the state of New Jersey, serving businesses to report total wages paid, pensions, annuities, and gambling winnings from which state tax was withheld. |

| Submission Deadline | Employers must file the NJ-W-3M form by February 28th of the year following the tax year being reported to ensure compliance with state requirements. |

| Governing Law | The NJ-W-3M form is governed by the New Jersey Division of Taxation, under the State of New Jersey's tax laws and regulations. |

| Filing Methods | Filers can submit the NJ-W-3M form and accompanying W-2s using various methods, including magnetic tape/cartridge, diskette, or paper, to cater to different technological capacities among employers. |

Detailed Steps for Using Nj W 3M

Filling out the NJ W-3M form is an essential step for employers in New Jersey to reconcile the gross income tax withheld from their employees' wages. This process ensures that employers report and submit the correct amount of taxes to the New Jersey Division of Taxation, contributing to the smooth functioning of state tax operations. While the form might appear complicated at first glance, following a structured guide can simplify the process. Below are detailed steps to accurately complete the NJ W-3M form, ensuring compliance and timely submission.

- First, locate the section titled "FOR TAXABLE YEAR" at the very top of the form and enter the applicable year for which you're reporting.

- Under "Identification Number," input your employer identification number (EIN) to identify your business to the Division of Taxation.

- Write your full legal name where it says "NAME."

- If your business operates under a different name, provide this "TRADE NAME (IF APPLICABLE)."

- In the "ADDRESS" field, include your business mailing address exactly as it should appear on official correspondence.

- For "CITY, STATE, ZIP CODE," ensure you provide the complete address information, facilitating any necessary contact or documentation delivery.

- Locate the line beginning with "INDICATE NUMBER OF EMPLOYEES" and enter the total number of employees for whom you've withheld taxes.

- Next to "TOTAL GROSS WAGES, PENSION AND ANNUITY INCOME AND GAMBLING WINNINGS," report the combined total of these amounts.

- In the section labeled "TOTAL AMOUNT WITHHELD," write down the total tax amount withheld from your employees' earnings.

- Review the address provided under "Mail NJ-W-3M and W-2’s to:" and prepare an envelope directed to this location: State of New Jersey - GIT Division of Taxation, PO Box 333, Trenton, NJ 08646-0333.

- Select your "W-2 Filing Method" by indicating whether you'll use Magnetic Tape/Cartridge, Diskette, or Paper. Attach your W-2 forms if you choose the Paper method.

- Sign and date the form where it says "Taxpayer Signature" and "Date," certifying the accuracy and truthfulness of the information provided.

- If you're working with a preparer, have them complete the "Preparer Signature," "Date," "Preparer/Firm Identification Number," "Firm Name," and "Address" sections.

After completing the form, double-check all information for accuracy to avoid potential errors or delays. Once you're confident that everything is correct, mail the NJ-W-3M form alongside the required W-2 forms to the provided address. Remember, the deadline for submission is February 28 of the following year. Timely and accurate filing helps ensure that your business remains in good standing and that your employees' tax obligations are properly accounted for.

Learn More on Nj W 3M

What is the NJ-W-3M form?

The NJ-W-3M form, known as the Gross Income Tax Reconciliation of Tax Withheld, is a document required by the State of New Jersey Division of Taxation. It's used to summarize the total gross wages, pension and annuity income, and gambling winnings from which tax was withheld by an employer or business, and to reconcile these amounts with the total tax withheld for the year. This form is necessary for taxable years 1998 and onward.

Who needs to file the NJ-W-3M form?

This form must be filed by any employer or business that withheld New Jersey income tax from employees, pensioners, or on gambling winnings. It’s an essential part of annual tax filing requirements for entities that have withheld taxes on behalf of others.

When is the NJ-W-3M form due?

The NJ-W-3M form is due annually by February 28th for the previous tax year. Timely submission is crucial to avoid penalties and interest for late filing.

What are the filing methods for the NJ-W-3M?

The NJ-W-3M form can be filed using several methods. These include:

- Magnetic Tape/Cartridge

- Diskette

- Paper

Note that if you're using paper filing, the W-2 forms must be attached to the Form NJ-W-3.

Where should the NJ-W-3M form be sent?

The completed NJ-W-3M form, along with any required W-2 forms if applicable, should be mailed to:

State of New Jersey - GIT

Division of Taxation

PO Box 333

Trenton, NJ 08646-0333

How do you ensure the NJ-W-3M form is correctly completed?

To make sure your NJ-W-3M form is correctly filled out:

- Double-check the Identification Number and the accuracy of the name, trade name (if applicable), address, city, state, and zip code provided.

- Accurately report the number of employees, total gross wages, pension and annuity income, and gambling winnings.

- Verify the total amount of tax withheld to ensure it matches with your records.

- Ensure both sides of the return are completed as required.

- Sign and date the form, including the preparer's signature, date, and firm identification number if prepared by someone other than the taxpayer.

Are there any penalties for filing the NJ-W-3M late?

Yes, there are penalties for filing the NJ-W-3M form late. The State of New Jersey may impose late filing penalties, interest on the unpaid tax due, and other penalties for failure to file or pay taxes on time. Therefore, it's important to ensure timely filing and payment to avoid these penalties.

Common mistakes

Filling out the NJ W-3M form, which is crucial for the Gross Income Tax Reconciliation of Tax Withheld in New Jersey, often presents challenges. People occasionally make mistakes due, in part, to the form's specific requirements and deadlines. Here are some of the common errors encountered:

- Missing the Deadline: The form must be filed no later than February 28th following the taxable year. A surprising number of people overlook this critical deadline, leading to unnecessary penalties or interest charges.

- Incorrect Identification Number: Each form must include a correct Identification Number. Errors in this section can lead to processing delays or misidentification.

- Failure to Indicate the Number of Employees: On the form, there's a specific requirement to state the number of employees. Misreporting or forgetting to fill this out can cause discrepancies and potential audits.

- Omitting Total Gross Wages, Pension, Annuity Income, and Gambling Winnings: Some filers skip or inaccurately report these amounts, which are essential for accurate tax withholding reconciliation.

- Incorrectly Calculated Total Amount Withheld: Miscalculations in this field can result from simple math errors or misunderstanding what constitutes withholdable income, leading to reporting inaccuracies.

- Improper Filing Method Indicated: The form allows for different filing methods, including Magnetic Tape/Cartridge, Diskette, and Paper. Choosing the incorrect method for submission can lead to the form being returned or not processed.

- Leaving the Certification Section Incomplete: The form requires a taxpayer signature to certify that the return is true and correct. Missing signatures are a common oversight that renders the form incomplete.

- Forgetting to Attach W-2 Forms: The NJ W-3M must be mailed along with W-2 forms. Failing to include these can lead to processing delays and potential penalties.

To avoid these pitfalls, individuals should take their time when filling out the form, double-check their work, and ensure all supporting documents are attached. Attention to detail and adherence to deadlines are key factors in successfully submitting the NJ W-3M form.

Documents used along the form

When managing payroll and taxes in New Jersey, several forms and documents commonly accompany the NJ-W-3M (Gross Income Tax Reconciliation of Tax Withheld) form. This comprehensive list provides insights into the forms often used alongside the NJ-W-3M to ensure compliance and facilitate accurate tax reporting for businesses.

- W-2 Forms (Wage and Tax Statement): These forms report an employee's annual wages and the amount of taxes withheld from their paycheck. They are crucial for employees to file their personal income taxes.

- W-4 Forms (Employee's Withholding Certificate): Used by employees to determine the amount of federal income tax to withhold from their wages. This form helps employers calculate and withhold the correct federal income tax from employees' paychecks.

- NJ-W-4 Forms: Similar to the Federal W-4, this form is specific to the state of New Jersey and helps determine the amount of New Jersey state income tax to withhold from employees' wages.

- 941 Forms (Employer's Quarterly Federal Tax Return): These forms report to the IRS the amount of federal income tax, Social Security tax, and Medicare tax withheld from employees' paychecks by the employer.

- NJ-927 Forms: This is a quarterly report form used in New Jersey for reporting state income tax, unemployment insurance, and disability insurance withheld by employers.

- 1099 Forms (Miscellaneous Income): Often used by employers and businesses to report payments made to independent contractors, rents, royalties, and other forms of non-employee compensation.

- Unemployment Wage Report Forms: These are required for reporting total wages paid to employees, which helps in determining unemployment insurance contributions in New York.

- NJ-WT (Payment Voucher for Gross Income Tax Withheld): This voucher is used by employers to make payments of withheld taxes to the New Jersey Division of Taxation.

- Annual Report Forms: Businesses often need to file an annual report with the state of New Jersey, providing updated information on the entity’s structure and operations.

Each of these documents plays a vital role in ensuring the accurate and timely reporting and payment of taxes both to the state of New Jersey and to the federal government. Using them correctly alongside the NJ-W-3M form can help businesses avoid penalties and ensure compliance with tax regulations.

Similar forms

The Federal Form W-3, "Transmittal of Wage and Tax Statements," bears similarity to the NJ W-3M, serving as a summary or reconciliation form that employers must file with the Social Security Administration (SSA) along with all W-2 forms for their employees. Both forms compile information on wages paid and taxes withheld from employees, although the W-3 is for federal reporting, whereas the NJ W-3M focuses on New Jersey state tax obligations. This distinction highlights how payroll reporting requirements must be met at both the federal and state levels, with each form playing a crucial role in the process.

Another relevant document is Form 940, "Employer's Annual Federal Unemployment (FUTA) Tax Return." Form 940 parallels the NJ W-3M in that it is an annual filing employers must complete, but it focuses on unemployment taxes rather than income taxes. While the NJ W-3M reconciles income taxes withheld from employees’ wages for New Jersey, Form 940 reconciles federal unemployment tax responsibilities. Each document ensures employers meet their respective tax reporting requirements for different types of taxes.

Form 941, "Employer's Quarterly Federal Tax Return," shares a purpose with the NJ W-3M, albeit on a federal level and on a quarterly basis. Form 941 is used by employers to report income taxes, social security tax, or Medicare tax withheld from employees' paychecks. Similarly to the NJ W-3M, which is used annually, Form 941 ensures the IRS is aware of the taxes withheld and paid on behalf of the employees, showing the regulatory parallels between state and federal tax obligations.

The W-2 form is an essential document closely associated with the NJ W-3M, providing detailed information on an employee's income, taxes withheld, and other deductions for the year. While the W-2 is prepared for each individual employee, the NJ W-3M serves as a collective summary of all W-2 forms issued by an employer within New Jersey. Basically, the W-2s provide the employee-specific information that fills the summary reported in the NJ-W3M, directly feeding into the reconciliation process required by the state.

State specific versions of the W-3 form, like the California Form DE-9C, "Quarterly Contribution Return and Report of Wages," perform a similar role to the NJ W-3M but cater to different state requirements. These forms serve as a reconciliation of wages and taxes paid within their respective states, showing how each state has its mechanisms for ensuring employers report and pay their tax dues properly. Though they vary in frequency and specific details required, the overarching goal mirrors that of the NJ W-3M.

The 1096 form, "Annual Summary and Transmittal of U.S. Information Returns," is akin to the NJ W-3M in its role as a summary document. While the 1096 is used to transmit Form 1099s and other types of information returns to the IRS, the NJ W-3M is specifically for reconciling gross income taxes withheld. Both serve as the final step in the reporting process, providing a comprehensive overview of the information being reported to the government.

Form 945, "Annual Return of Withheld Federal Income Tax," is designed for reporting federal income tax withheld from non-payroll items. It aligns with the NJ W-3M’s objective of tax reconciliation, but Form 945 encompasses areas like gambling winnings, pensions, and backup withholding on interest and dividends. This demonstrates how both forms cater to similar needs—ensuring taxes withheld are properly reported—albeit in different contexts.

The Schedule H form, associated with household employment taxes, shares a reconciliation function with the NJ W-3M. Schedule H is used by taxpayers to report taxes from household employees on their federal income tax returns. Like the NJ W-3M, it provides a summary of taxes due based on wages paid, highlighting the requirement across various employment types to accurately report and pay employment taxes.

The New York NYS-45, "Quarterly Combined Withholding, Wage Reporting, and Unemployment Insurance Return," is another parallel, catering to New York employers. It combines reporting for state income tax withholding, wage reporting, and unemployment insurance into one form, similarly to how the NJ W-3M handles income tax for New Jersey. This illustrates the variation in state reporting requirements, with each state streamlining its processes within a single or multiple forms.

Lastly, the Federal Form 1099 series, particularly Form 1099-MISC, reflects the broader concept of tax reporting captured by the NJ W-3M. Form 1099-MISC is used to report various types of income outside wages, salaries, and tips. While different in detail and purpose, both forms play crucial roles in the broader tax reporting and payment ecosystem, ensuring individuals and entities report income accurately to state and federal tax authorities.

Dos and Don'ts

Filling out the NJ W-3M form, which is crucial for the reconciliation of tax withheld in New Jersey, requires a careful approach to ensure accuracy and compliance with state tax laws. Here are some tips to help guide you through the process.

Do:- Verify all information before submission: Ensure that every detail, including the Identification Number, names, addresses, and the total amounts reported, is accurate. Incorrect information can lead to processing delays or errors in tax reconciliation.

- Include all required attachments: Make sure to attach all W-2 forms as required. These forms are essential for completing the NJ-W-3M process, as they provide detailed information about employees' wages and taxes withheld.

- Sign and date the form: The form is not considered valid until it is signed by the taxpayer and, if applicable, the preparer. This acts as a certification that the information provided is true and correct to the best of your knowledge.

- Meet the submission deadline: Submitting the form by the due date, February 28, is crucial to avoid any penalties or interest for late filing. Timely submission ensures compliance with state tax requirements.

- Forget to report all required income types: It's important to report total gross wages, pension and annuity income, and gambling winnings. Each category is vital for accurate tax reconciliation and should not be overlooked.

- Use the wrong filing method: Choose the correct W-2 filing method (Magnetic Tape/Cartridge, Diskette, or Paper) that suits your submission. Using the wrong method can result in processing errors or delays.

- Omit any part of the form: Both sides of the NJ-W-3M form must be completed. Skipping sections or failing to fill out parts of the form can lead to incomplete submissions, which may affect the reconciliation process.

- Disregard the certification statement: The certification statement at the bottom of the form is there for a reason. By signing it, you're affirming that everything you've reported is accurate. Ignoring this step undermines the form's validity and your compliance.

Misconceptions

There are several misconceptions surrounding the NJ W-3M form, a crucial document for reporting state income tax withholding in New Jersey. Understanding these inaccuracies is vital for ensuring compliance and accuracy in tax filings.

Only businesses with employees need to file: This is a misconception because the NJ W-3M form must also be filed by businesses paying pension and annuity income, and gambling winnings, not just wages to employees.

It’s optional to file the NJ W-3M form: Filing this form is mandatory for any business that withholds New Jersey state income tax. It's not optional, as failing to file can result in penalties.

The due date is the same every year: While the general deadline is February 28th, exceptions or extensions can occur, such as leap years or when the due date falls on a weekend or holiday, potentially pushing the deadline.

Electronic filing is not allowed: Contrary to this belief, New Jersey accepts electronic filing of the NJ W-3M form. E-filing is not only permitted but is also encouraged for its efficiency and quick processing time.

Only paper forms require accompanying W-2s: Regardless of the filing method, whether paper or electronic, W-2 forms must accompany the NJ W-3M form. This ensures all withholding information matches across documents.

You can file the NJ W-3M form without first issuing W-2s to employees: This is incorrect. W-2s must be distributed to employees before or simultaneously when filing the NJ W-3M to ensure all parties have consistent tax records.

There’s only one way to file: The NJ W-3M form can be submitted through multiple channels, including mail and electronically. The method of filing (Magnetic Tape/Cartridge, Diskette, Paper) should be chosen based on the filer’s convenience and resources.

Addressing these misconceptions head-on is paramount for all businesses operating within New Jersey. Ensuring accurate and timely filings not only aids in compliance but also prevents potential fines or audits from the Division of Taxation.

Key takeaways

When preparing and submitting the NJ W-3M for the State of New Jersey, it's pivotal to keep several key practices and regulations in mind. These insights facilitate compliance with the Division of Taxation requirements and ensure proper reporting of employee withholdings for the Gross Income Tax. Here are eight key takeaways from the NJ W-3M form instructions and usage guidelines:

- Deadline Compliance: The form must be filed no later than February 28th of the following year, to avoid any penalties or complications with the Division of Taxation.

- Identification Information: Accurately fill in the identification number, your name, trade name if applicable, and the complete address including city, state, and zip code to ensure proper processing and identification.

- Reporting Details: It's crucial to indicate the total number of employees, total gross wages, pension and annuity income, and gambling winnings accurately to reconcile tax withheld correctly.

- Submitting the Form: When mailing the NJ-W-3M, include all necessary documents such as W-2 forms, and send them to the GIT Division of Taxation at the specified PO Box in Trenton, NJ.

- Form Completion: Ensure both sides of the return are fully completed to meet the submission requirements of the State of New Jersey.

- Choosing the W-2 Filing Method: Indicate your method of W-2 filing, whether it's via magnetic tape/cartridge, diskette, or paper. Attach the W-2 forms to the NJ-W-3M form if submitting through paper.

- Signature and Certification: The form requires a signature from the taxpayer and, if applicable, the preparer, to certify that the information provided is accurate to the best of their knowledge. Signatures are crucial for the document's validity.

- Preparer Information: If a preparer besides the taxpayer themselves is involved, include the preparer’s signature, date, identification number, and firm name and address. This ensures accountability and traceability of the filed documents.

By adhering to these guidelines, individuals can ensure their NJ W-3M submission is compliant, accurate, and timely, which contributes to a smoother process with the Division of Taxation.

Popular PDF Documents

Nj Tax Forms 2023 - Opting out of e-filing using the NJ-1040-O may be necessary for those without internet access or e-filing capabilities.

Nj Family Court Forms - Supports the pursuit of fairness in medical expenses, offering a mechanism to request financial contributions from the other parent.

Nj Business Names Monmouth County - Remember the significance of each owner's signature on the trade name certificate, as it signifies individual agreement and responsibility.