Fill Out a Valid Nj W3 Template

Every year, businesses operating within New Jersey or dealing with unregistered unincorporated contractors in the state have an important tax obligation to fulfill through the New Jersey Department of the Treasury, Division of Taxation. The crux of this obligation is captured in the Annual Reconciliation of Gross Income Tax Withheld From Unregistered Unincorporated Contractors, designated as Schedule NJ-W-3-UNC. This form serves a pivotal role in ensuring that taxes withheld from payments made to these contractors within the year are accurately reported. Importantly, it distinguishes between New Jersey employers and those outside the state, outlining distinct requirements for each regarding the reporting of withholding payments alongside the regular Monthly or Quarterly returns. Furthermore, it mandates the inclusion of copies of Form 1099-MISC, which detail the payments made to unregistered unincorporated contractors, emphasizing the New Jersey Gross Income Tax withheld. The Schedule NJ-W-3-UNC, accompanied by the 1099 forms, is to be submitted by a specific deadline, reinforcing the importance of timely compliance with state tax regulations. This form not only facilitates the reconciliation of gross income tax withheld but also serves to underscore the transparency and accountability expected of businesses in their dealings with unregistered contractors, ensuring that all parties fulfill their tax obligations accordingly.

Sample - Nj W3 Form

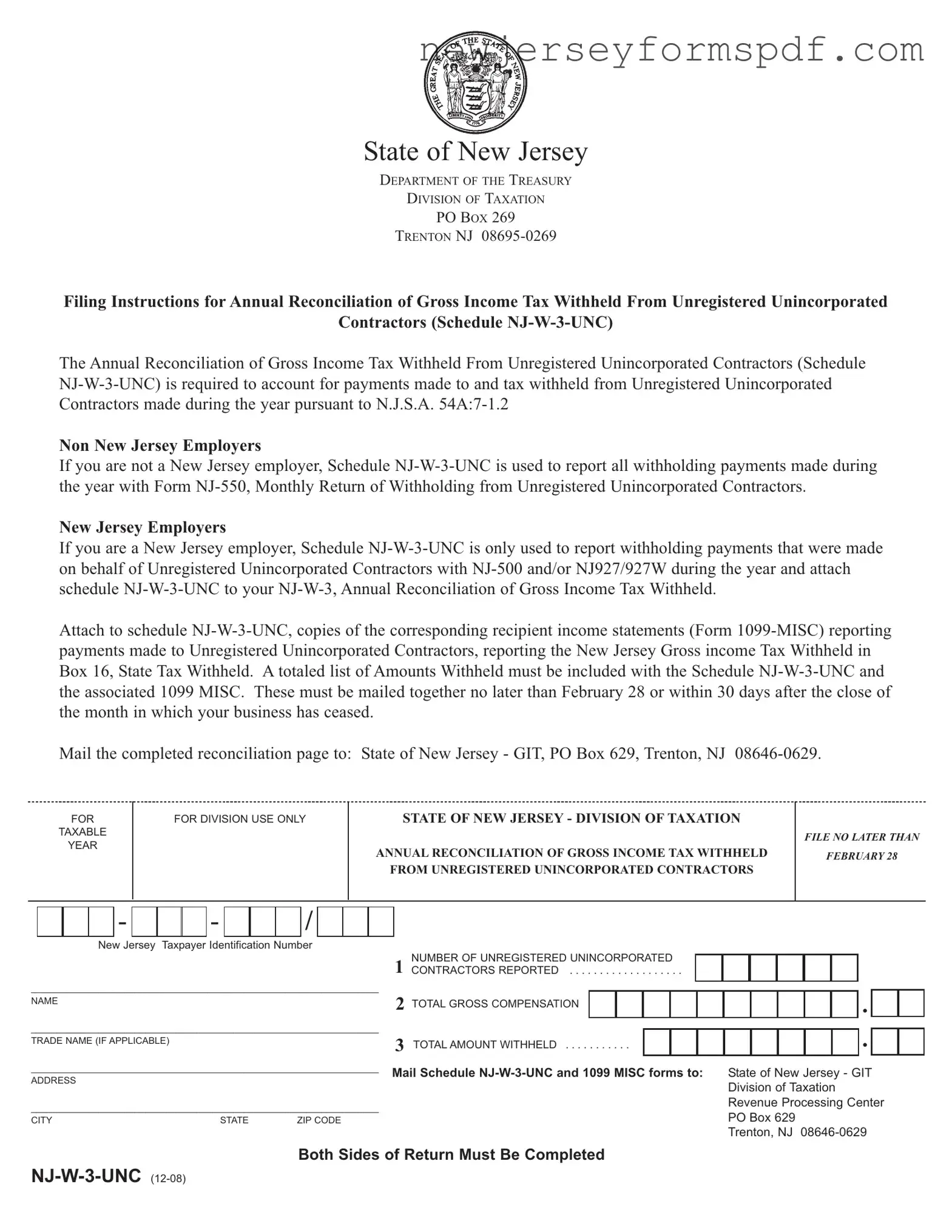

State of New Jersey

DEPARTMENT OF THE TREASURY

DIVISION OF TAXATION

PO BOX 269

TRENTON NJ

Filing Instructions forAnnual Reconciliation of Gross IncomeTaxWithheld From Unregistered Unincorporated

Contractors (Schedule

TheAnnual Reconciliation of Gross Income Tax Withheld From Unregistered Unincorporated Contractors (Schedule

Contractors made during the year pursuant to N.J.S.A.

Non New Jersey Employers

If you are not a New Jersey employer, Schedule

New Jersey Employers

If you are a New Jersey employer, Schedule

Attach to schedule

Mail the completed reconciliation page to: State of New Jersey - GIT, PO Box 629, Trenton, NJ

FOR

TAXABLE

YEAR

FOR DIVISION USE ONLY

STATE OFNEWJERSEY- DIVISION OFTAXATION

ANNUALRECONCILIATION OFGROSS INCOMETAXWITHHELD

FROM UNREGISTERED UNINCORPORATED CONTRACTORS

FILENOLATERTHAN

FEBRUARY28

-

-

-

-

/

/

New Jersey Taxpayer Identification Number

NUMBER OF UNREGISTERED UNINCORPORATED

1 CONTRACTORS REPORTED . . . . . . . . . . . . . . . . . . .

___________________________________________________________________ |

2 TOTALGROSS COMPENSATION |

|

|

|

|

|

NAME |

|

|

|

|

|

|

|

|

|

|

|

|

|

___________________________________________________________________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

TRADE NAME (IFAPPLICABLE) |

3 TOTALAMOUNTWITHHELD |

|

|

|

||

|

|

|

|

|||

___________________________________________________________________ Mail Schedule |

||||||

ADDRESS |

|

|

|

|

|

|

___________________________________________________________________ |

|

|

|

|

|

|

CITY |

STATE |

ZIPCODE |

•

•

State of New Jersey - GIT

Division of Taxation

Revenue Processing Center

POBox 629

Trenton, NJ

Both Sides of Return Must Be Completed

Line Item Instructions forAnnual Reconciliation of Gross IncomeTaxWithheld From Unregistered Unincorporated Contractors

(Schedule

Enter your: NJ Taxpayer Identification Number, Taxpayer Name, Tape Name (if applicable), Mailing Name, Mailing StreetAddress, mailing City, State, and Zip Code.

Complete Lines 1,2, 3 as follows:

Line 1: Enter the number of Unregistered Unincorporated Contractors to whom payments were made during the calendar year.

Line 2: Enter the total gross amount paid to Unregistered Unincorporated Contractors during the calendar year.

Line 3: Enter the total amount of withholding made during the calendar year for Unregistered Unincorporated Contractors.

Annual Reconciliation of Gross IncomeTaxWithheld from Unregistered Unincorporated Contractors

Attach copies of form

I hereby certify that this return, to the best of my knowledge and belief, is a true and correct return.

_________________________________________________________________________________ |

|

|

Taxpayer Signature |

Date |

|

_________________________________________________________________________________ |

___________________________________________________________________ |

|

Preparer Signature |

Date |

Preparer/Firm Identification Number |

__________________________________________________________________________________ |

___________________________________________________________________ |

|

Firm Name (or yours, if |

|

Address |

Document Specifications

| Fact Name | Description |

|---|---|

| Purpose of NJ-W-3-UNC | This form is used for the Annual Reconciliation of Gross Income Tax Withheld from Unregistered Unincorporated Contractors. |

| Governing Law | This process is mandated by N.J.S.A. 54A:7-1.2, addressing payments to and tax withholdings from unregistered unincorporated contractors. |

| Deadline for Submission | The completed form, along with the necessary attachments, must be mailed by February 28 or within 30 days after the closure of the business month. |

| Attachment Requirements | Employers must attach copies of the 1099-MISC forms reporting payments to Unregistered Unincorporated Contractors and a totaled list of the amounts withheld. |

| Recipient | The form and attachments should be sent to the State of New Jersey - GIT Division of Taxation Revenue Processing Center, PO Box 629, Trenton, NJ 08646-0629. |

Detailed Steps for Using Nj W3

Filling out the NJ W3 form is a critical process for businesses operating in New Jersey, especially when dealing with unregistered unincorporated contractors. This step is necessary for accurately reporting and reconciling gross income tax withheld from payments made to these contractors during the year. It requires collecting relevant information, ensuring accurate calculations, and submitting the completed form alongside necessary documents by the stipulated deadline. Here's a straightforward guide to help you through the process.

- Start by locating your New Jersey Taxpayer Identification Number. You will need this to accurately identify your business in the records.

- Write down the full legal name of the taxpayer or the business name in the space provided for "Taxpayer Name".

- If applicable, include the trade name of the business in the designated field.

- Enter the complete mailing address of the business, including the street address, city, state, and ZIP code. This ensures any correspondence related to the form can reach you without delays.

- In Line 1, input the total number of unregistered unincorporated contractors you have paid throughout the calendar year. This helps in determining the extent of reporting required.

- Proceed to Line 2, and enter the gross total compensation paid to these contractors within the year. Accuracy here is crucial for correct tax calculation.

- On Line 3, specify the total amount that was withheld from these payments for gross income tax purposes throughout the year.

- Gather all the Form 1099-MISC documents that detail the payments made to unregistered unincorporated contractors. These forms should show the New Jersey Gross Income Tax Withheld in Box 16 for each contractor.

- Compile a totaled list of the amounts withheld, as mentioned in the 1099-MISC forms. This will be included with your NJ-W-3-UNC form for a comprehensive reconciliation.

- Ensure that both the taxpayer signature and date sections at the bottom of the form are duly filled in. If someone prepared the form on behalf of the taxpayer, their signature, preparer/firm identification number, name, and address should also be included.

- Review the entire form and accompanying documents for accuracy. Any mistakes can result in processing delays or incorrect tax reconciliations.

- Finally, mail the completed NJ-W-3-UNC form along with all required 1099-MISC forms and the listed totals of amounts withheld to the State of New Jersey - GIT, Division of Taxation Revenue Processing Center, PO Box 629, Trenton, NJ 08646-0629. Remember, this must be done no later than February 28th or within 30 days following the cessation of your business within the calendar year.

By meticulously following these steps, businesses can ensure compliance with New Jersey’s tax laws regarding payments to unregistered unincorporated contractors. Keeping accurate records and being diligent in the preparation of the NJ W3 form will streamline the process, making it manageable and error-free.

Learn More on Nj W3

What is the NJ-W-3-UNC form?

The NJ-W-3-UNC, or the Annual Reconciliation of Gross Income Tax Withheld From Unregistered Unincorporated Contractors, is a form required by the State of New Jersey for reporting payments made to, and taxes withheld from, unregistered unincorporated contractors within a year. This form helps the Division of Taxation ensure that income taxes withheld from these contractors are properly reported and paid.

Who needs to file the NJ-W-3-UNC form?

There are specific categories of payors who need to file this form:

- Non-New Jersey Employers: Those who are not considered New Jersey employers but have made withholding payments during the year in relation to Unregistered Unincorporated Contractors must use this form in conjunction with Form NJ-550, Monthly Return of Withholding from Unregistered Unincorporated Contractors.

- New Jersey Employers: Those considered as New Jersey employers use this form to report withholding payments only made on behalf of Unregistered Incorporated Contractors, in relation to NJ-500 and/or NJ-927/927W filings.

What documents are required to accompany the NJ-W-3-UNC?

When submitting the NJ-W-3-UNC form, it is essential to include:

- Copies of recipient income statements (Form 1099-MISC) that report payments made to unregistered unincorporated contractors, specifically showing the New Jersey Gross Income Tax Withheld in Box 16, State Tax Withheld.

- A totaled list of all amounts withheld must also be included with the Schedule NJ-W-3-UNC.

What is the filing deadline for the NJ-W-3-UNC form?

The completed NJ-W-3-UNC form and all required accompanying documents must be submitted no later than February 28th of the following year. If the business ceases operations, the documents must be filed within 30 days following the close of the business month.

Where should the NJ-W-3-UNC form be mailed?

The completed NJ-W-3-UNC form, along with the corresponding 1099-MISC forms and the totaled listing of amounts withheld, should be mailed to:

State of New Jersey - GIT, Division of Taxation, Revenue Processing Center, PO Box 629, Trenton, NJ 08646-0629.

Common mistakes

Filling out the NJ W-3 form, which deals specifically with the Annual Reconciliation of Gross Income Tax Withheld from Unregistered Unincorporated Contractors, requires attention to detail and an understanding of tax regulations. However, people commonly make several mistakes during this process. Recognizing and avoiding these errors can save a lot of time and prevent the hassle of dealing with the Department of Treasury's corrections.

Not including the New Jersey Taxpayer Identification Number: This is a crucial piece of information that identifies the business. Failing to provide this can result in the form being rejected or delayed in processing.

Incorrectly reporting the total gross compensation paid to unregistered unincorporated contractors: It's important to accurately calculate and report the total amount paid. Overlooking or misreporting can lead to discrepancies and potential penalties.

Omitting or misreporting the total amount withheld: The total amount of withholding made during the calendar year for Unregistered Unincorporated Contractors needs to be accurately reported. Errors here could affect your reconciliations and tax liabilities.

Forgetting to attach copies of Form 1099-MISC: Along with schedule NJ-W-3-UNC, copies of the corresponding recipient income statements must be attached. These documents are vital for verifying the payments made and the New Jersey Gross Income Tax Withheld.

Missing the deadline for submission: The deadline for mailing the completed reconciliation page and accompanying documents is no later than February 28 or within 30 days after the business has ceased operations for the year. Late submissions can incur penalties and interest.

In addition to these points,

Ensure all required signatures are present. Both the taxpayer and the preparer (if applicable) need to sign the form to validate the information provided. Unsigned forms can be subject to rejection or delay.

Double-check the mailing address before sending your documents. Mailing them to the incorrect address can lead to delays or the loss of sensitive financial information.

Keep thorough records. Maintaining detailed records of payments made to unregistered unincorporated contractors and taxes withheld will make completing this form easier and more accurate.

By taking care to avoid these common mistakes, you can streamline the process of completing your NJ W-3 form and ensure that your business remains in good standing with the New Jersey Department of Treasury.

Documents used along the form

When working with New Jersey's Schedule NJ-W-3-UNC for the Annual Reconciliation of Gross Income Tax Withheld from Unregistered Unincorporated Contractors, it's important to be familiar with several other forms and documents that may be needed alongside this schedule. These documents are essential for a comprehensive approach to handling tax withholdings and filings for contractors in New Jersey.

- Form NJ-550: This is a Monthly Return of Withholding from Unregistered Unincorporated Contractors. For those not considered as New Jersey employers, this form is used to report all withholding payments made during the year.

- Form NJ-500: Employers use this form for making Quarterly Wage and Tax Reports. It's a part of the process for reporting withholding payments for Unregistered Unincorporated Contractors if you're a New Jersey employer.

- Form NJ-927/927W: This is a Quarterly Wage and Tax Report for New Jersey employers, which is also used in conjunction with Schedule NJ-W-3-UNC to report withholdings from Unregistered Unincorporated Contractors.

- Form 1099-MISC: Copies of this form must be attached to Schedule NJ-W-3-UNC. It reports the payments made to Unregistered Unincorporated Contractors and the New Jersey Gross Income Tax Withheld, specifically in Box 16 for State Tax Withheld.

- NJ-W-3: The Annual Reconciliation of Gross Income Tax Withheld form is necessary for New Jersey employers to summarize the total income taxes withheld from employees and contractors over the year. Schedule NJ-W-3-UNC is attached to this form when required.

- Form W-9: Although not directly linked to the withholding process, Form W-9, Request for Taxpayer Identification Number and Certification, is often collected from contractors, including Unregistered Unincorporated Contractors, to accurately report payments via 1099 forms and comply with tax withholding requirements.

Gathering and accurately completing these forms and documents is crucial for adhering to New Jersey's tax laws and regulation concerning the compensation and tax withholdings for unregistered unincorporated contractors. Ensuring you have all the necessary paperwork prepared will streamline your annual reconciliation process and keep you compliant with state tax obligations.

Similar forms

The Federal Form W-3, "Transmittal of Wage and Tax Statements," is quite similar to the New Jersey Schedule NJ-W-3-UNC. Both of these forms play an important role in summarizing information that has been reported on other forms. Specifically, the Federal Form W-3 is used to accompany Form W-2, "Wage and Tax Statement," when these are sent to the Social Security Administration. It summarizes the total earnings, Social Security wages, Medicare wages, and withholding for all employees for the year. Similarly, NJ-W-3-UNC serves as a summary for payments made to, and taxes withheld from, unregistered unincorporated contractors, providing an annual overview much like the Federal W-3 does, but with a focus on unregistered contractors within New Jersey.

The 1099-MISC form, "Miscellaneous Income," shares similarities with the NJ-W-3-UNC in content focus. These forms are centered around reporting payments made to individuals or entities that are not direct employees of a company. While the 1099-MISC form is used to report payments such as rents, royalties, or fees paid to non-employees, the NJ-W-3-UNC specifically focuses on income tax withheld from payments made to unregistered unincorporated contractors within New Jersey. Both forms are crucial for the accurate reporting of non-employee compensation and ensuring appropriate tax withholding and payments to tax authorities.

Form NJ-927/927W, "Employer's Quarterly Report," is another document that shares functional similarities with the Schedule NJ-W-3-UNC. NJ-927/927W is used by employers to report wages paid, and the taxes withheld from those wages, each quarter within New Jersey. While this form is used on a quarterly basis to manage and document ongoing tax obligations, the NJ-W-3-UNC compiles information annually, specifically focusing on the reconciliation of gross income tax withheld from unregistered unincorporated contractors. Both are pivotal in maintaining accurate tax records and ensuring employers fulfill their tax withholding responsibilities within the state.

The Federal Form 940, "Employer's Annual Federal Unemployment (FUTA) Tax Return," like the NJ-W-3-UNC, is used to report annual information to a governmental tax authority. Form 940 details the employer's federal unemployment tax liabilities, providing an annual recap similar to how NJ-W-3-UNC provides a yearly summary of tax withheld for unregistered unincorporated contractors. Though Form 940 focuses on unemployment taxes at the federal level and NJ-W-3-UNC deals with income taxes withheld for a specific group of workers within New Jersey, both serve critical roles in ensuring employers accurately report and pay their respective tax obligations yearly.

Dos and Don'ts

When preparing the Annual Reconciliation of Gross Income Tax Withheld from Unregistered Unincorporated Contractors, Schedule NJ-W-3-UNC, it is important to be diligent and accurate. Here are some essential dos and don’ts to keep in mind:

- Do ensure that you correctly identify whether you are a New Jersey employer or a non-New Jersey employer as this determines how you should fill out the form.

- Do accurately report the number of unregistered unincorporated contractors you paid during the calendar year on Line 1.

- Do enter the total gross amount paid to these contractors in the calendar year on Line 2.

- Do include the total amount of tax withheld for these contractors during the calendar year on Line 3.

- Do attach copies of the 1099-MISC forms reporting payments made to Unregistered Unincorporated Contractors, clearly indicating the New Jersey Gross Income Tax Withheld in Box 16.

- Don't forget to include a totaled list of amounts withheld with the Schedule NJ-W-3-UNC.

- Don't overlook the deadline for mailing the completed Schedule NJ-W-3-UNC and associated 1099-MISC forms, which is no later than February 28 or within 30 days after the closure of the business month.

- Don't send incomplete or inaccurate forms, ensuring that all required fields are correctly filled out and all necessary documentation is attached.

By carefully following these guidelines, you can help ensure that your submission is both compliant and processed in a timely manner. Remember to mail the completed reconciliation and forms to the State of New Jersey - GIT, Division of Taxation Revenue Processing Center, P.O. Box 629, Trenton, NJ 08646-0629.

Misconceptions

Many people have misconceptions about the NJ W-3 form, specifically the Annual Reconciliation of Gross Income Tax Withheld From Unregistered Unincorporated Contractors (Schedule NJ-W-3-UNC). Let’s clear up some of the most common misunderstandings:

- Misconception #1: Only New Jersey Employers Need to File

It's often thought that only New Jersey employers must file Schedule NJ-W-3-UNC. However, this form must be filed by anyone who has made payments to unregistered unincorporated contractors, regardless of whether they are New Jersey employers or non-New Jersey employers. Non-New Jersey employers use this form in conjunction with Form NJ-550, while New Jersey employers attach it to their NJ-W-3 form.

- Misconception #2: It's Only For Payments Made to Individuals

While Schedule NJ-W-3-UNC does relate to unregistered unincorporated contractors, these can be individuals or entities not recognized as separate legal entities. The key factor is not the structure of the contractor but rather that they are unregistered and unincorporated.

- Misconception #3: Form 1099-MISC Is Not Required

Another common misunderstanding is that the 1099-MISC forms are not necessary when filing Schedule NJ-W-3-UNC. In fact, copies of Form 1099-MISC reporting payments made to unregistered unincorporated contractors and the New Jersey Gross Income Tax Withheld must be attached to the Schedule NJ-W-3-UNC form.

- Misconception #4: Information on Payments and Withholdings Can Be Approximated

Every detail reported on Schedule NJ-W-3-UNC, such as the number of unregistered unincorporated contractors, total gross compensation, and total amount withheld, must be accurately reported. Approximating these numbers or failing to provide exact amounts can lead to discrepancies and potential issues with the New Jersey Division of Taxation.

- Misconception #5: The Deadline Is Flexible

Some might think that the filing deadline for Schedule NJ-W-3-UNC is flexible. However, the form must be mailed no later than February 28th following the taxable year, or within 30 days after the close of the month in which the business ceases. Late submissions can result in penalties.

- Misconception #6: Electronic Filing Is An Option

Despite the increasing shift towards electronic filing for many tax forms, Schedule NJ-W-3-UNC, along with the corresponding 1099-MISC forms, must be mailed to the specified address. Currently, there is no option for electronically filing this specific schedule.

Understanding these key points can help ensure that the process of filing Schedule NJ-W-3-UNC is done correctly, avoiding common pitfalls and misconceptions.

Key takeaways

Understanding the process and requirements for the Annual Reconciliation of Gross Income Tax Withheld from Unregistered Unincorporated Contractors in New Jersey, through Schedule NJ-W-3-UNC, is crucial for compliant financial operations. Here are key takeaways about filling out and using the NJ W3 form:

- The purpose of Schedule NJ-W-3-UNC is to report payments and gross income tax withheld from unregistered unincorporated contractors over the calendar year.

- Non-New Jersey employers are required to use Schedule NJ-W-3-UNC in conjunction with Form NJ-550 for reporting all withholding payments made during the year.

- New Jersey employers use Schedule NJ-W-3-UNC to report withholdings only for unregistered unincorporated contractors, attaching it to their NJ-W-3 when payments were made using NJ-500 and/or NJ927/927W.

- It is mandatory to attach copies of the recipients' income statements (Form 1099-MISC) indicating the payments made to unregistered unincorporated contractors and the New Jersey Gross Income Tax Withheld in Box 16.

- A summarized list of amounts withheld must accompany the Schedule NJ-W-3-UNC and the associated 1099 MISC forms.

- The completed forms and attachments must be mailed by February 28th or within 30 days after the business ceases operations, whichever comes first.

- Submissions should be sent to the State of New Jersey - GIT, PO Box 629, Trenton, NJ 08646-0629.

- Key information required on the form includes the company's New Jersey Taxpayer Identification Number, the number of unregistered unincorporated contractors reported, total gross compensation paid, and the total amount withheld.

- The taxpayer or preparer must certify the accuracy and completeness of the return, signifying that, to the best of their knowledge, the return is correct.

Popular PDF Documents

Renew Ucr - Part of New Jersey's broader effort to track, analyze, and respond to hate crimes and the communities they affect.

Register Dba in Nj - The form requires a detailed description of the business activity that will be conducted under the alternate name in New Jersey.