Fill Out a Valid Nj W4 Template

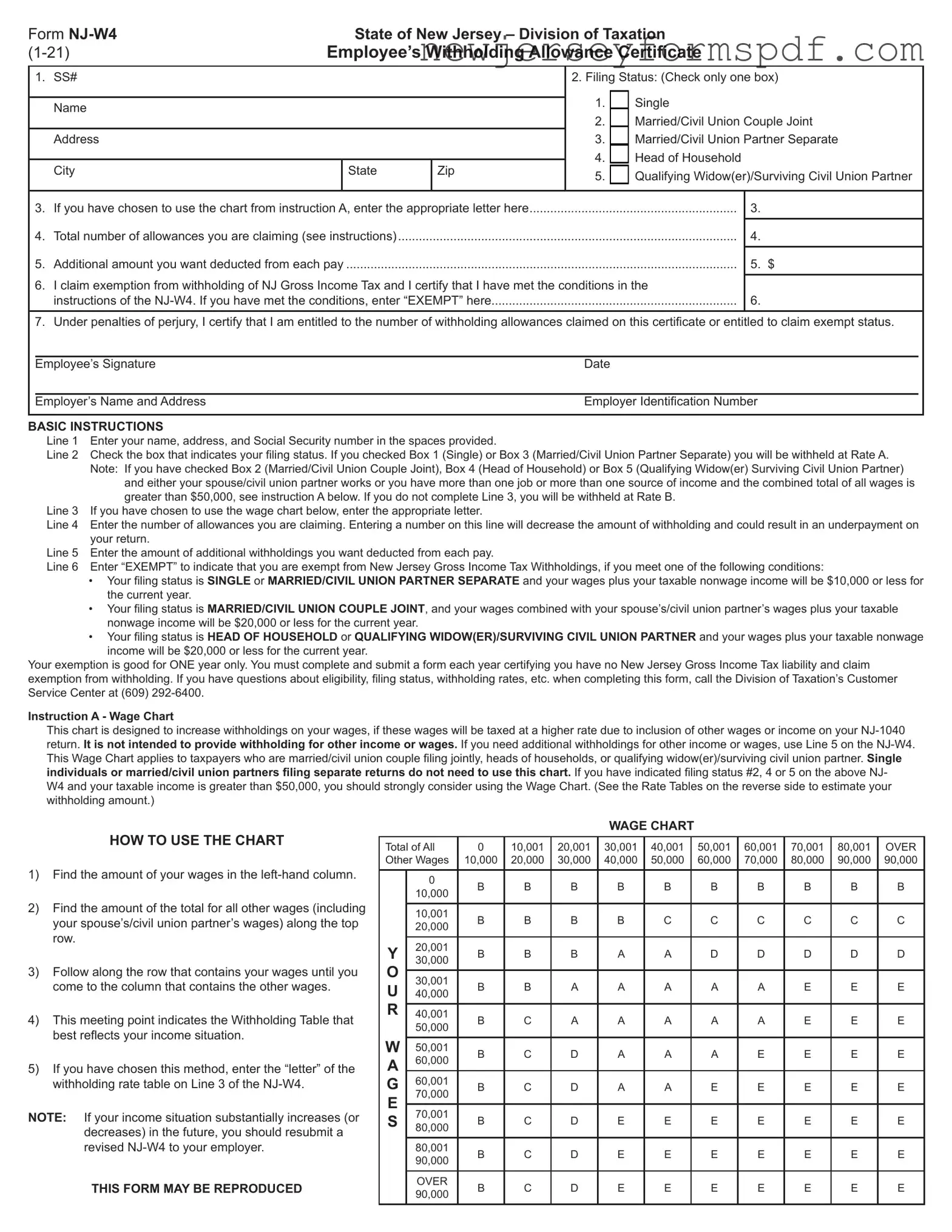

The NJ W4 form, formally known as the Employee's Withholding Allowance Certificate, plays a pivotal role for both employees and employers within the State of New Jersey. This document, issued by the State of New Jersey Division of Taxation, serves the purpose of indicating how much state income tax should be withheld from an employee's paycheck. It has multiple sections, including personal information, filing status, number of allowances, and any additional amount the employee wishes to have withheld. Importantly, the form includes options for employees to adjust withholding rates based on their personal income and filing status, which can significantly impact their take-home pay and annual tax liabilities. Additionally, certain individuals may claim exemption from withholdings if they meet specific conditions outlined in the form. The form itself requires careful consideration of one's income, tax status, and any potential tax liabilities or refunds. It also features a unique wage chart and accompanying rate tables designed to aid in accurate withholding for individuals with higher combined incomes or multiple jobs. Updating the NJ W4 form as personal financial situations change can ensure employees are not under or over-withheld, steering clear of unexpected tax bills or penalties.

Sample - Nj W4 Form

Form |

|

State of New Jersey – Division of Taxation |

||||||||

Employee’s Withholding Allowance Certificate |

||||||||||

1. |

SS# |

|

|

|

2. Filing Status: (Check only one box) |

|||||

|

|

|

|

|

|

1. |

|

Single |

||

|

|

|

|

|

|

|

||||

|

|

Name |

|

|

|

|

||||

|

|

|

|

|

2. |

|

Married/Civil Union Couple Joint |

|||

|

|

|

|

|

|

|

||||

|

|

Address |

|

|

|

3. |

|

Married/Civil Union Partner Separate |

||

|

|

|

|

|

|

4. |

|

Head of Household |

||

|

|

City |

|

State |

Zip |

5. |

|

Qualifying Widow(er)/Surviving Civil Union Partner |

||

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

3. |

If you have chosen to use the chart from instruction A, enter the appropriate letter here |

|

|

3. |

|

|||||

|

|

|

|

|

|

|

|

|

||

4. |

Total number of allowances you are claiming (see instructions) |

|

|

|

|

4. |

|

|||

|

|

|

|

|

|

|

|

|

||

5. |

Additional amount you want deducted from each pay |

|

|

|

|

5. $ |

|

|||

6. |

I claim exemption from withholding of NJ Gross Income Tax and I certify that I have met the conditions in the |

|

|

|||||||

|

|

|||||||||

|

|

instructions of the |

|

|

6. |

|

||||

|

|

|

|

|

|

|

||||

7. |

Under penalties of perjury, I certify that I am entitled to the number of withholding allowances claimed on this certificate or entitled to claim exempt status. |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

Employee’s Signature |

|

|

|

Date |

|

|

|

||

|

|

|

|

|

|

|

|

|

||

|

Employer’s Name and Address |

|

|

|

Employer Identification Number |

|||||

|

|

|

|

|

|

|

|

|

|

|

BASIC INSTRUCTIONS

Line 1 Enter your name, address, and Social Security number in the spaces provided.

Line 2 Check the box that indicates your filing status. If you checked Box 1 (Single) or Box 3 (Married/Civil Union Partner Separate) you will be withheld at Rate A. Note: If you have checked Box 2 (Married/Civil Union Couple Joint), Box 4 (Head of Household) or Box 5 (Qualifying Widow(er) Surviving Civil Union Partner)

and either your spouse/civil union partner works or you have more than one job or more than one source of income and the combined total of all wages is greater than $50,000, see instruction A below. If you do not complete Line 3, you will be withheld at Rate B.

Line 3 If you have chosen to use the wage chart below, enter the appropriate letter.

Line 4 Enter the number of allowances you are claiming. Entering a number on this line will decrease the amount of withholding and could result in an underpayment on your return.

Line 5 Enter the amount of additional withholdings you want deducted from each pay.

Line 6 Enter “EXEMPT” to indicate that you are exempt from New Jersey Gross Income Tax Withholdings, if you meet one of the following conditions:

•Your filing status is SINGLE or MARRIED/CIVIL UNION PARTNER SEPARATE and your wages plus your taxable nonwage income will be $10,000 or less for the current year.

•Your filing status is MARRIED/CIVIL UNION COUPLE JOINT, and your wages combined with your spouse’s/civil union partner’s wages plus your taxable nonwage income will be $20,000 or less for the current year.

•Your filing status is HEAD OF HOUSEHOLD or QUALIFYING WIDOW(ER)/SURVIVING CIVIL UNION PARTNER and your wages plus your taxable nonwage income will be $20,000 or less for the current year.

Your exemption is good for ONE year only. You must complete and submit a form each year certifying you have no New Jersey Gross Income Tax liability and claim exemption from withholding. If you have questions about eligibility, filing status, withholding rates, etc. when completing this form, call the Division of Taxation’s Customer

Service Center at (609)

Instruction A - Wage Chart

This chart is designed to increase withholdings on your wages, if these wages will be taxed at a higher rate due to inclusion of other wages or income on your

This Wage Chart applies to taxpayers who are married/civil union couple filing jointly, heads of households, or qualifying widow(er)/surviving civil union partner. Single individuals or married/civil union partners filing separate returns do not need to use this chart. If you have indicated filing status #2, 4 or 5 on the above NJ- W4 and your taxable income is greater than $50,000, you should strongly consider using the Wage Chart. (See the Rate Tables on the reverse side to estimate your

withholding amount.)

HOW TO USE THE CHART

1)Find the amount of your wages in the

2)Find the amount of the total for all other wages (including your spouse’s/civil union partner’s wages) along the top row.

3)Follow along the row that contains your wages until you come to the column that contains the other wages.

4)This meeting point indicates the Withholding Table that best reflects your income situation.

5)If you have chosen this method, enter the “letter” of the withholding rate table on Line 3 of the

NOTE: If your income situation substantially increases (or decreases) in the future, you should resubmit a revised

THIS FORM MAY BE REPRODUCED

WAGE CHART

Total of All |

0 |

10,001 |

20,001 |

30,001 |

40,001 |

50,001 |

60,001 |

70,001 |

80,001 |

OVER |

||

Other Wages |

10,000 |

20,000 |

30,000 |

40,000 |

50,000 |

60,000 |

70,000 |

80,000 |

90,000 |

90,000 |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

0 |

B |

B |

B |

B |

B |

B |

B |

B |

B |

B |

|

|

10,000 |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10,001 |

B |

B |

B |

B |

C |

C |

C |

C |

C |

C |

|

|

20,000 |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Y |

20,001 |

B |

B |

B |

A |

A |

D |

D |

D |

D |

D |

|

O |

30,000 |

|

|

|

|

|

|

|

|

|

|

|

30,001 |

B |

B |

A |

A |

A |

A |

A |

E |

E |

E |

||

U |

40,000 |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|||

R |

|

|

|

|

|

|

|

|

|

|

|

|

40,001 |

B |

C |

A |

A |

A |

A |

A |

E |

E |

E |

||

|

50,000 |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

||

W |

|

|

|

|

|

|

|

|

|

|

|

|

50,001 |

B |

C |

D |

A |

A |

A |

E |

E |

E |

E |

||

A |

60,000 |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|||

G |

60,001 |

B |

C |

D |

A |

A |

E |

E |

E |

E |

E |

|

E |

70,000 |

|

|

|

|

|

|

|

|

|

|

|

80,00070,001 |

B |

|

|

|

|

|

|

|

|

|

||

S |

C |

D |

E |

E |

E |

E |

E |

E |

E |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

80,001 |

B |

C |

D |

E |

E |

E |

E |

E |

E |

E |

|

|

90,000 |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

OVER |

B |

C |

D |

E |

E |

E |

E |

E |

E |

E |

|

|

90,000 |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

RATE TABLES FOR WAGE CHART

The rate tables listed below correspond to the letters in the Wage Chart on the front page. Use these to estimate the amount of withholding that will occur if you choose to use the wage chart. Compare this to your estimated income tax liability for your New Jersey Income Tax return to see if this is the correct amount of withholding that you should have.

RATE “A”

WEEKLY PAYROLL PERIOD (Allowance $19.20) |

|

|

|

ANNUAL PAYROLL PERIOD (Allowance $1,000) |

|

|

|

|

|||||||||||

If the amount of taxable |

|

|

The amount of income tax to be |

If the amount of taxable |

|

The amount of income tax to be |

|||||||||||||

wages is: |

|

|

|

withheld is: |

|

|

wages is: |

|

|

|

withheld is: |

|

|

||||||

|

Over |

But Not Over |

|

|

|

Of Excess Over |

|

Over |

But Not Over |

|

|

|

|

Of Excess Over |

|||||

$ |

0 |

$ |

385 |

|

|

|

1.5% |

$ |

0 |

$ |

0 |

$ |

20,000 |

|

|

|

1.5% |

$ |

0 |

$ |

385 |

$ |

673 |

$ |

5.77 |

+ |

2.0% |

$ |

385 |

$ |

20,000 |

$ |

35,000 |

$ |

300.00 |

+ |

2.0% |

$ |

20,000 |

$ |

673 |

$ |

769 |

$ |

11.54 |

+ |

3.9% |

$ |

673 |

$ |

35,000 |

$ |

40,000 |

$ |

600.00 |

+ |

3.9% |

$ |

35,000 |

$ |

769 |

$ |

1,442 |

$ |

15.29 |

+ |

6.1% |

$ |

769 |

$ |

40,000 |

$ |

75,000 |

$ |

795.00 |

+ |

6.1% |

$ |

40,000 |

$ |

1,442 |

$ |

9,615 |

$ |

56.35 |

+ |

7.0% |

$ |

1,442 |

$ |

75,000 |

$ |

500,000 |

$ |

2,930.00 |

+ |

7.0% |

$ |

75,000 |

$ |

9,615 |

$ |

19,231 |

$ |

628.46 |

+ |

9.9% |

$ |

9,615 |

$ |

500,000 |

$ |

1,000,000 |

$ |

32,680.00 |

+ |

9.9% |

$ |

500,000 |

$ |

19,231 |

|

|

$ |

1,580.38 |

+ |

11.8% |

$ |

19,231 |

$ |

1,000,000 |

|

over |

$ |

82,180.00 |

+ |

11.8% |

$ |

1,000,000 |

RATE “B”

WEEKLY PAYROLL PERIOD (Allowance $19.20) |

|

|

|

ANNUAL PAYROLL PERIOD (Allowance $1,000) |

|

|

|

|

|||||||||||

If the amount of taxable |

|

|

The amount of income tax to be |

If the amount of taxable |

|

The amount of income tax to be |

|||||||||||||

wages is: |

|

|

|

withheld is: |

|

|

wages is: |

|

|

|

withheld is: |

|

|

||||||

|

Over |

But Not Over |

|

|

|

Of Excess Over |

|

Over |

But Not Over |

|

|

|

|

Of Excess Over |

|||||

$ |

0 |

$ |

385 |

|

|

|

1.5% |

$ |

0 |

$ |

0 |

$ |

20,000 |

|

|

|

1.5% |

$ |

0 |

$ |

385 |

$ |

962 |

$ |

5.77 |

+ |

2.0% |

$ |

385 |

$ |

20,000 |

$ |

50,000 |

$ |

300.00 |

+ |

2.0% |

$ |

20,000 |

$ |

962 |

$ |

1,346 |

$ |

17.31 |

+ |

2.7% |

$ |

962 |

$ |

50,000 |

$ |

70,000 |

$ |

900.00 |

+ |

2.7% |

$ |

50,000 |

$ |

1,346 |

$ |

1,538 |

$ |

27.69 |

+ |

3.9% |

$ |

1,346 |

$ |

70,000 |

$ |

80,000 |

$ |

1,440.00 |

+ |

3.9% |

$ |

70,000 |

$ |

1,538 |

$ |

2,885 |

$ |

35.19 |

+ |

6.1% |

$ |

1,538 |

$ |

80,000 |

$ |

150,000 |

$ |

1,830.00 |

+ |

6.1% |

$ |

80,000 |

$ |

2,885 |

$ |

9,615 |

$ |

117.31 |

+ |

7.0% |

$ |

2,885 |

$ |

150,000 |

$ |

500,000 |

$ |

6,100.00 |

+ |

7.0% |

$ |

150,000 |

$ |

9,615 |

$ |

19,231 |

$ |

588.46 |

+ |

9.9% |

$ |

9,615 |

$ |

500,000 |

$ |

1,000,000 |

$ |

30,600.00 |

+ |

9.9% |

$ |

500,000 |

$ |

19,231 |

|

|

$ |

1,540.38 |

+ |

11.8% |

$ |

19,231 |

$ |

1,000,000 |

|

|

$ |

80,100.00 |

+ |

11.8% |

$ |

1,000,000 |

RATE “C”

WEEKLY PAYROLL PERIOD (Allowance $19.20) |

|

|

|

ANNUAL PAYROLL PERIOD (Allowance $1,000) |

|

|

|

|

|||||||||||

If the amount of taxable |

|

|

The amount of income tax to be |

If the amount of taxable |

|

The amount of income tax to be |

|||||||||||||

wages is: |

|

|

|

withheld is: |

|

|

wages is: |

|

|

|

withheld is: |

|

|

||||||

|

Over |

But Not Over |

|

|

|

Of Excess Over |

|

Over |

But Not Over |

|

|

|

|

Of Excess Over |

|||||

$ |

0 |

$ |

385 |

|

|

|

1.5% |

$ |

0 |

$ |

0 |

$ |

20,000 |

|

|

|

1.5% |

$ |

0 |

$ |

385 |

$ |

769 |

$ |

5.77 |

+ |

2.3% |

$ |

385 |

$ |

20,000 |

$ |

40,000 |

$ |

300.00 |

+ |

2.3% |

$ |

20,000 |

$ |

769 |

$ |

962 |

$ |

14.62 |

+ |

2.8% |

$ |

769 |

$ |

40,000 |

$ |

50,000 |

$ |

760.00 |

+ |

2.8% |

$ |

40,000 |

$ |

962 |

$ |

1,154 |

$ |

20.00 |

+ |

3.5% |

$ |

962 |

$ |

50,000 |

$ |

60,000 |

$ |

1,040.00 |

+ |

3.5% |

$ |

50,000 |

$ |

1,154 |

$ |

2,885 |

$ |

26.73 |

+ |

5.6% |

$ |

1,154 |

$ |

60,000 |

$ |

150,000 |

$ |

1,390.00 |

+ |

5.6% |

$ |

60,000 |

$ |

2,885 |

$ |

9,615 |

$ |

123.65 |

+ |

6.6% |

$ |

2,885 |

$ |

150,000 |

$ |

500,000 |

$ |

6,430.00 |

+ |

6.6% |

$ |

150,000 |

$ |

9,615 |

$ |

19,231 |

$ |

567.88 |

+ |

9.9% |

$ |

9,615 |

$ |

500,000 |

$ |

1,000,000 |

$ |

29,530.00 |

+ |

9.9% |

$ |

500,000 |

$ |

19,231 |

|

|

$ |

1,519.81 |

+ |

11.8% |

$ |

19,231 |

$ |

1,000,000 |

|

|

$ |

79,030.00 |

+ |

11.8% |

$ |

1,000,000 |

RATE “D”

WEEKLY PAYROLL PERIOD (Allowance $19.20) |

|

|

|

ANNUAL PAYROLL PERIOD (Allowance $1,000) |

|

|

|

|

|||||||||||

If the amount of taxable |

|

|

The amount of income tax to be |

If the amount of taxable |

|

The amount of income tax to be |

|||||||||||||

wages is: |

|

|

|

withheld is: |

|

|

wages is: |

|

|

|

withheld is: |

|

|

||||||

|

Over |

But Not Over |

|

|

|

Of Excess Over |

|

Over |

But Not Over |

|

|

|

|

Of Excess Over |

|||||

$ |

0 |

$ |

385 |

|

|

|

1.5% |

$ |

0 |

$ |

0 |

$ |

20,000 |

|

|

|

1.5% |

$ |

0 |

$ |

385 |

$ |

769 |

$ |

5.77 |

+ |

2.7% |

$ |

385 |

$ |

20,000 |

$ |

40,000 |

$ |

300.00 |

+ |

2.7% |

$ |

20,000 |

$ |

769 |

$ |

962 |

$ |

16.15 |

+ |

3.4% |

$ |

769 |

$ |

40,000 |

$ |

50,000 |

$ |

840.00 |

+ |

3.4% |

$ |

40,000 |

$ |

962 |

$ |

1,154 |

$ |

22.69 |

+ |

4.3% |

$ |

962 |

$ |

50,000 |

$ |

60,000 |

$ |

1,180.00 |

+ |

4.3% |

$ |

50,000 |

$ |

1,154 |

$ |

2,885 |

$ |

30.96 |

+ |

5.6% |

$ |

1,154 |

$ |

60,000 |

$ |

150,000 |

$ |

1,610.00 |

+ |

5.6% |

$ |

60,000 |

$ |

2,885 |

$ |

9,615 |

$ |

127.88 |

+ |

6.5% |

$ |

2,885 |

$ |

150,000 |

$ |

500,000 |

$ |

6,650.00 |

+ |

6.5% |

$ |

150,000 |

$ |

9,615 |

$ |

19,231 |

$ |

565.38 |

+ |

9.9% |

$ |

9,615 |

$ |

500,000 |

$ |

1,000,000 |

$ |

29,400.00 |

+ |

9.9% |

$ |

500,000 |

$ |

19,231 |

|

|

$ |

1,517.31 |

+ |

11.8% |

$ |

19,231 |

$ |

1,000,000 |

|

|

$ |

78,900.00 |

+ |

11.8% |

$ |

1,000,000 |

RATE “E”

WEEKLY PAYROLL PERIOD (Allowance $19.20) |

|

|

|

ANNUAL PAYROLL PERIOD (Allowance $1,000) |

|

|

|

|

|||||||||||

If the amount of taxable |

|

|

The amount of income tax to be |

If the amount of taxable |

|

The amount of income tax to be |

|||||||||||||

wages is: |

|

|

|

withheld is: |

|

|

wages is: |

|

|

|

withheld is: |

|

|

||||||

|

Over |

But Not Over |

|

|

|

Of Excess Over |

|

Over |

But Not Over |

|

|

|

|

Of Excess Over |

|||||

$ |

0 |

$ |

385 |

|

|

|

1.5% |

$ |

0 |

$ |

0 |

$ |

20,000 |

|

|

|

1.5% |

$ |

0 |

$ |

385 |

$ |

673 |

$ |

5.77 |

+ |

2.0% |

$ |

385 |

$ |

20,000 |

$ |

35,000 |

$ |

300.00 |

+ |

2.0% |

$ |

20,000 |

$ |

673 |

$ |

1,923 |

$ |

11.54 |

+ |

5.8% |

$ |

673 |

$ |

35,000 |

$ |

100,000 |

$ |

600.00 |

+ |

5.8% |

$ |

35,000 |

$ |

1,923 |

$ |

9,615 |

$ |

84.04 |

+ |

6.5% |

$ |

1,923 |

$ |

100,000 |

$ |

500,000 |

$ |

4,370.00 |

+ |

6.5% |

$ |

100,000 |

$ |

9,615 |

$ |

19,231 |

$ |

584.04 |

+ |

9.9% |

$ |

9,615 |

$ |

500,000 |

$ |

1,000,000 |

$ |

30,370.00 |

+ |

9.9% |

$ |

500,000 |

$ |

19,231 |

|

|

$ |

1,535.96 |

+ |

11.8% |

$ |

19,231 |

$ |

1,000,000 |

|

|

$ |

79,870.00 |

+ |

11.8% |

$ |

1,000,000 |

Document Specifications

| Fact Name | Fact Detail |

|---|---|

| Form Designation | NJ-W4 Form - Employee's Withholding Allowance Certificate |

| Form Issuer | State of New Jersey – Division of Taxation |

| State Specificity | Specific to New Jersey residents for state tax purposes |

| Filing Status Options | Single, Married/Civil Union Couple Joint, Married/Civil Union Partner Separate, Head of Household, Qualifying Widow(er)/Surviving Civil Union Partner |

| Exemption Criteria | Single or Married/Civil Union Partner Separate with $10,000 or less in taxable income; Married/Civil Union Couple Joint or Head of Household/Qualifying Widow(er)/Surviving Civil Union Partner with $20,000 or less in taxable income |

| Allowance Claim | Employees can claim withholding allowances to reduce the amount of state tax withheld. |

| Additional Withholding Request | Allows for additional amount to be deducted from each pay. |

| Annual Resubmission Requirement for Exemptions | Exempt status must be claimed annually. |

| Wage Chart Utility | Helps in determining increased withholdings when combined total of all wages exceeds $50,000. |

| Governing Law(s) | New Jersey Gross Income Tax Act |

Detailed Steps for Using Nj W4

The process of completing the NJ W4 form is a straightforward one, designed to ensure that the correct amount of New Jersey Gross Income Tax is withheld from an employee's earnings. Following the steps outlined below will ensure that the form is filled out correctly and in compliance with the state's taxation requirements. It's important to pay close attention to each detail, as this document plays a significant role in the financial responsibilities of working in New Jersey.

- Start by entering your full legal name, home address, city, state, and zip code in the designated fields at the top of the form.

- Select your filing status by checking the appropriate box next to either Single, Married/Civil Union Couple Joint, Married/Civil Union Partner Separate, Head of Household, or Qualifying Widow(er)/Surviving Civil Union Partner.

- If applicable, choose the appropriate letter from the wage chart provided in Instruction A that corresponds to your filing status and income, and enter this letter in Line 3.

- Determine the total number of allowances you're claiming based on your personal and financial situation, then enter this number in Line 4. Remember, more allowances mean less tax will be withheld.

- If you wish to have an additional amount deducted from each paycheck, specify this amount in dollars on Line 5.

- To claim exemption from New Jersey Gross Income Tax withholdings, write “EXEMPT” in Line 6. Ensure you meet the eligibility requirements as stated in the form's instructions before doing so.

- After reviewing the form for accuracy, sign and date it at the bottom to certify under penalties of perjury that the information provided is correct.

- Lastly, write the employer's name and address, and their Employer Identification Number, in the designated spots.

Once the NJ W4 form has been completed and signed, it's important to submit it to the employer's payroll or human resources department as promptly as possible. Timely submission will ensure that withholdings are adjusted in accordance with the new information, helping to avoid any unexpected outcomes when filing the state income tax return. It's recommended to keep a copy of the completed form for personal records.

Learn More on Nj W4

What is the NJ W4 form?

The NJ W4 form, officially known as the Employee's Withholding Allowance Certificate, is a document that employees in New Jersey complete to indicate how much state income tax should be withheld from their paychecks. This form helps ensure that the right amount of tax is withheld, based on your income, filing status, and other factors.

Who needs to fill out the NJ W4 form?

Any employee in the state of New Jersey who earns income that is subject to state income tax should complete the NJ W4 form. This includes both new hires and current employees who want to update their withholding allowances or marital status.

How do I determine my filing status on the NJ W4 form?

Your filing status on the NJ W4 form corresponds to your personal situation and how you expect to file your taxes. Options include Single, Married/Civil Union Couple Joint, Married/Civil Union Partner Separate, Head of Household, or Qualifying Widow(er)/Surviving Civil Union Partner. Choose the status that best describes your anticipated tax filing situation for the year.

Can I claim exempt status on my NJ W4?

Yes, you can claim exempt status on your NJ W4 if you meet certain conditions, such as expecting to have no New Jersey Gross Income Tax liability for the year because your income falls below certain thresholds. These thresholds vary based on your filing status. Remember, claiming exempt status means no state tax will be withheld from your pay.

How many allowances should I claim?

The number of allowances you claim on the NJ W4 form determines how much state income tax is withheld from your paycheck. The more allowances you claim, the less tax is withheld. Consider your personal and financial circumstances, including dependents and other income, to decide the appropriate number of allowances. The instructions on the form can help guide you in making this decision.

What if my income changes or I want to adjust my withholding?

If your income changes significantly or if you want to adjust the amount of state tax withheld from your paycheck for any reason, you should submit a new NJ W4 form to your employer with updated information. This can help ensure that you're not under- or overwithheld come tax time.

What is the Wage Chart and how do I use it?

The Wage Chart included with the NJ W4 instructions is designed for employees whose income, combined with that of a spouse or from multiple jobs, exceeds $50,000. It helps to adjust your withholdings more accurately to avoid underpayment of taxes. You use the chart to find your combined wage amount and identify the corresponding withholding rate table letter to enter on your NJ W4.

How can additional withholdings be specified on the NJ W4?

If you need to have additional tax withheld from each paycheck, you can specify this amount on line 5 of the NJ W4 form. This might be necessary if you have other income that's not subject to withholding, owe additional taxes, or are looking to get a bigger refund when you file your state income tax return.

What happens if I don't submit a NJ W4 form?

If you don't submit a completed NJ W4 form to your employer, state tax will be withheld from your pay at a default rate, which might not accurately reflect your actual tax liability. This could result in owing more state income tax when you file your return.

Where can I get help if I have questions about completing the NJ W4?

If you have questions about how to complete the NJ W4 form or are unsure about your tax liability, you can contact the New Jersey Division of Taxation's Customer Service Center at (609) 292-6400. They can provide guidance based on your specific situation.

Common mistakes

Filling out the New Jersey W-4 (NJ-W4) form is a necessary step for employees to indicate their tax withholdings preferences. However, mistakes can occur in this process, leading to incorrect withholdings from your paycheck. Here are ten common mistakes to avoid:

- Incorrect Social Security Number: It's crucial to double-check the SSN is entered correctly to ensure proper tax records and to avoid issues with your tax return.

- Misunderstanding Filing Status options: Selecting the wrong filing status, such as Single when you might qualify for Head of Household, can affect your withholding rate.

- Not using the wage chart properly: When your combined income is over $50,000, failing to use or incorrectly applying the wage chart instructions can lead to inaccurate withholdings.

- Claiming the wrong number of allowances: Each allowance reduces the amount of money withheld from your paycheck. Incorrectly calculating your allowances can result in owing taxes or receiving a large refund.

- Overlooking additional income: If you have additional income that's not subject to withholding, failing to account for it on Line 5 can lead to underpayment of taxes.

- Claiming exemption without meeting conditions: Exempt status requires meeting specific income thresholds. Claiming this status without meeting the criteria can result in tax liability.

- Incorrectly adjusting for multiple jobs or working spouses: Not adjusting your withholding when you or your spouse has multiple jobs can lead to underpaying taxes.

- Forgetting to re-submit the form when financial situations change: Any major financial changes, such as a change in income or marital status, necessitate submitting a new NJ-W4.

- Neglecting to consider non-wage income: If you have taxable non-wage income, failing to adjust your withholdings to cover the tax liability on this income can lead to a tax bill.

- Providing outdated information: Not updating personal information such as your address could lead to delays or loss of important tax documentation.

It's important to fill out the NJ-W4 form carefully and accurately to ensure the correct amount of tax is withheld, avoiding unpleasant surprises during tax season. Knowing and avoiding these common mistakes can help safeguard against potential issues.

Documents used along the form

When starting a new job in New Jersey, the Form NJ-W4 is one of the primary documents you'll encounter. This form is essential for determining the amount of New Jersey state income tax that will be withheld from your paycheck. However, beyond the NJ-W4, there are several other forms and documents frequently used to ensure accurate and compliant handling of employees' financial and tax details. Understanding these forms will help you navigate through the onboarding process smoothly and ensure that your employer withholds the correct amount of tax from your paycheck.

- Form I-9, Employment Eligibility Verification: This form is required by the U.S. government to document that each new employee (both citizens and noncitizens) is authorized to work in the United States. The I-9 form requires employees to present documents proving their identity and employment authorization.

- Form W-2, Wage and Tax Statement: Although not used at the start of employment, the W-2 form is crucial for employees. It reports an employee's annual wages and the amount of taxes withheld from their paycheck. Employers must send out the W-2 form to employees by January 31st each year.

- Form W-9, Request for Taxpayer Identification Number and Certification: Self-employed individuals or contractors in New Jersey may be asked to complete a W-9 form. This form is used by businesses to gather information from vendors or independent contractors, like their Taxpayer Identification Number (TIN), to report income paid to them and withheld taxes to the IRS.

- Direct Deposit Authorization Form: Many employers offer direct deposit for paychecks, which requires employees to fill out a direct deposit authorization form. This form provides the employer with the necessary information to deposit funds directly into the employees’ bank accounts, including account numbers and bank routing numbers.

Together, these forms play a critical role in the employee onboarding process, tax calculations, and financial transactions between employers and employees. While the Form NJ-W4 deals specifically with state income tax withholding, each of the other documents serves its unique purpose, from verifying work eligibility to ensuring you receive your paycheck in the most convenient way possible. Having a good understanding of these forms and providing accurate, up-to-date information will help streamline your employment setup and maintain compliance with state and federal regulations.

Similar forms

The Form W-4, known as the Employee’s Withholding Certificate, at a federal level shares similarities with the NJ-W4 since both aim to inform employers about the correct amount of tax to withhold from employees' paychecks. Just like its New Jersey counterpart, the Form W-4 requires employees to input personal information, such as filing status and number of dependents, which directly influences the calculation of withholding tax amounts. This process ensures that employees neither overpay nor underpay their tax obligations throughout the year.

The Form IT-2104, used in New York, is almost a twin to the NJ-W4, given that both are state-specific versions of the federal Form W-4, tailored to collect employee withholding information. Each form reflects its respective state's tax rates and regulations, helping employers withhold the correct state income tax. Employees in both states are prompted to provide similar information regarding their filing status, allowances, and additional withholdings, aimed at reaching an accurate tax deduction.

The California DE 4 Form plays a role similar to the NJ-W4 for California employees. This form helps calculate state payroll withholdings based on personal allowances and additional income. It reflects California’s unique tax schedules and credits, paralleling NJ-W4's purpose of customizing withholdings to fit New Jersey's tax code. Participants provide similar details about their income and personal situation to ensure their employer withholds an appropriate amount of state tax.

The Form A-4 is used by employees in Alabama and shares its purpose with the NJ-W4. Both forms serve to inform the employer about the employee's withholding preferences for state income tax. By indicating filing status, exemptions, and any additional amounts to be withheld, employees guide their employers in retaining the correct proportion of taxes, adjusting for the differing tax structures and regulations between Alabama and New Jersey.

Georgia’s Form G-4 offers a similar mechanism for tax withholding within its jurisdiction, akin to the NJ-W4. Employees in Georgia use Form G-4 to communicate their withholding needs based on their personal financial situation, similar to how NJ-W4 operates in New Jersey. Both documents effectively serve as tools for ensuring that the right amount of state income tax is withheld, reflecting each state's specific tax codes and rates.

Form MO W-4, utilized in Missouri, aligns with the NJ-W4 by providing a means for employees to signal their withholding requirements to employers, specific to Missouri’s tax provisions. It, too, requires information on the employee’s filing status and allowances, aiming to match withholding levels to the individual's estimated tax liability, paralleling the function and intent of the NJ-W4, albeit under Missouri's distinct tax parameters.

In Illinois, the Form IL-W-4 serves an identical purpose to the NJ-W4, guiding employers in withholding the correct amount of state income tax from employees' wages. Both forms ask for similar types of details from the employee, including filing status and number of allowances claimed, to tailor the withholding amount accurately to the employee’s tax liabilities, given the respective state tax laws.

Form VA-4 is designed for Virginia employees to indicate their state tax withholding preferences, drawing parallels to the NJ-W4. Through the VA-4, Virginians declare their personal allowances and additional withholding amounts, guiding employers on how much state income tax to deduct from their paychecks. This system ensures that employees’ tax withholdings are closely aligned with their actual tax liabilities according to Virginia’s tax statutes, mirroring the NJ-W4’s function in New Jersey.

Colorado’s Form DR 0004 shares the same goal as the NJ-W4: to communicate an employee's withholding choices to the employer within the context of the Colorado tax code. Employees indicate their preferred number of allowances and any extra withholding per pay period, ensuring that the withheld amounts reflect their anticipated state tax obligations, similar to how the NJ-W4 operates for New Jersey residents.

Oregon’s Form OR-W-4 plays a comparable role to the NJ-W4 by allowing employees to specify their withholding preferences for state taxes, tailored to Oregon’s tax regulations. The form collects details on the employee's financial situation and desired withholding level, ensuring the appropriate amount of tax is deducted from each paycheck. This mirrors the process and purpose of the NJ-W4, with adjustments to accommodate Oregon's different tax structure and rates.

Dos and Don'ts

Completing the NJ W4 form accurately is essential for ensuring the correct amount of New Jersey Gross Income Tax is withheld from your paycheck. Here is a guide to help you navigate the do's and don'ts when filling out this form:

- Do review your personal information for accuracy, including your Social Security Number (SS#) and address. Errors here can lead to processing delays or incorrect withholding.

- Do carefully consider your filing status to ensure it reflects your current legal and tax situation. This will impact your withholding rate.

- Do utilize the wage chart provided in instruction A if your combined household income is over $50,000. This can help prevent under-withholding.

- Do indicate the correct total number of allowances you’re claiming. More allowances mean less tax withheld, but it could also mean you owe more tax at year’s end if not accurate.

- Do specify an additional amount to withhold if you expect to owe more taxes or prefer to have a larger refund at the end of the year.

- Do claim exempt status only if you truly meet the conditions, such as expecting to earn below the taxable threshold for your filing status.

- Don't forget to sign and date the form. An unsigned form is invalid and could result in default withholding rates being applied.

- Don't guess when filling out the form. If you need help, contact the Division of Taxation’s Customer Service Center or a tax professional.

- Don't ignore changes in your personal or financial situation. Update your NJ W4 form as needed to ensure withholdings reflect your current situation.

- Don't overlook the instructions for each line. Following them closely can help you avoid common mistakes that could affect your withholding or result in inaccuracies.

Remember, the goal of completing the NJ W4 form accurately is to align your withholdings with your actual tax liability. By doing so, you avoid unexpected tax bills and penalties at the end of the tax year. Regularly review and adjust your withholdings to keep up with any changes in your financial situation.

Misconceptions

One common misconception is that the NJ-W4 form is identical to the federal W-4 form. While they serve similar purposes in determining the amount of state and federal tax withholding from an employee's paycheck, they are distinct forms with different criteria and must be filled out separately.

Many believe that if you claim exemption from withholding on your federal W-4, it automatically applies to your NJ-W4. This is incorrect. Exemption qualifications differ between state and federal guidelines. New Jersey has its own conditions for exemption, which are explicitly outlined in the NJ-W4 instructions.

Another mistake is thinking all employees must file a new NJ-W4 annually. Unlike the exemption claim, which must be renewed each year, other NJ-W4 selections remain in effect until an employee submits a new form to make changes.

Some individuals misunderstand the multiple income earners/higher income rates instructions, thinkingthey don't apply if they are unmarried. The wage chart and rate tables provided in the NJ-W4 instructions, however, are designed to guide those with higher incomes or multiple earners in a household, regardless of marital status, to adjust their withholdings accurately.

There's a misconception that entering "0" or "1" on the allowances line is always the safest approach to avoid owing taxes. While lower allowances increase withholding and can help prevent owing taxes at year's end, they may unnecessarily reduce your take-home pay. It's important to accurately calculate allowances to reflect your tax situation.

It's wrongly assumed that the additional amount requested on Line 5 is for an unspecified, one-time deduction. This section is actually for specifying an additional amount of money to be withheld from each paycheck, which can help cover expected tax liabilities or specific financial strategies.

Many employees think the NJ-W4 is only concerned with personal tax situations and miss that it also considers spousal income and joint liabilities, particularly in determining the correct withholding rate and when using the wage chart for married/civil union couples filing jointly or separately with substantial combined incomes.

Finally, a significant misunderstanding is that the NJ-W4 form's instructions and rate charts are overly complex and unnecessary. However, these tools are essential for accurately determining the appropriate withholding amount, ensuring employees neither overpay taxes throughout the year nor face large tax bills at year's end.

Key takeaways

Filling out the NJ-W4 form is essential for ensuring that the correct amount of New Jersey Gross Income Tax is withheld from your paychecks. Here are seven key takeaways to help you accurately complete the form:

- Familiarize yourself with the different filing statuses available and select the one that accurately reflects your current situation. This choice affects the withholding rate and is crucial for accurate tax deductions.

- Please pay special attention to Line 3 if your combined total income exceeds $50,000 for certain filing statuses. Using the instruction A wage chart can help adjust your withholdings to better match your tax liability.

- The number of allowances you claim on Line 4 directly influences the amount of tax withheld from your paycheck. Claiming fewer allowances increases the amount withheld, potentially resulting in a larger refund (or smaller amount due) when filing your tax return.

- For those wanting additional tax withheld from each paycheck, Line 5 allows you to specify an extra dollar amount for deduction.

- You can claim exempt status on Line 6 if you meet specific conditions, such as expecting your wages and taxable nonwage income to be below certain thresholds. However, you must re-certify your exemption annually.

- Understanding the importance of accurately completing the form cannot be understated. Misrepresentation on the NJ-W4 can lead to underpayment or overpayment of taxes and potential issues with the New Jersey Division of Taxation.

- If you experience significant life changes, such as a change in income, marital status, or the addition of a dependent, it might be necessary to revise your NJ-W4 form to reflect your new circumstances accurately.

Always ensure your NJ-W4 form is up to date to avoid any surprises during tax season. If you have doubts or questions, considering reaching out to the Division of Taxation's Customer Service Center or consulting with a tax professional can provide guidance tailored to your specific situation.

Popular PDF Documents

Nj Realtors Standard Form of Residential Lease Pdf - Covers initial deposit requirements, including how it should be credited towards rent or security deposit.

Nj Family Court Forms - It stands as a comprehensive guide for navigating the complexities of modifying family law orders in the aftermath of a judgment.

Who Must File Nj Inheritance Tax Return - Instructs on the proper compilation and submission of schedules for assets requiring New Jersey tax waivers.