Fill Out a Valid St 7 New Jersey Template

In the realm of agricultural and horticultural operations, navigating the landscape of tax exemptions in New Jersey involves understanding and utilizing various forms, one of which is the Farmer’s Exemption Certificate (ST-7). This form serves as a critical tool for eligible businesses, enabling them to make tax-exempt purchases of tangible personal property or services directly used in the production, handling, and preservation of agricultural or horticultural commodities. Recognized by the State of New Jersey Division of Taxation, this certificate outlines stringent criteria for its use, including specific types of commodities produced, and the tangible personal property or service purchased. Eligible purchasers are determined based on their involvement in farming enterprises, as defined by the Sales and Use Tax Act, N.J.S.A. 54:32B-8.16, excluding those primarily engaged in boarding or training horses or selling commodities produced by others. Furthermore, the ST-7 form distinguishes between single purchase and blanket certificates, emphasizes the requirement for good faith in transactions, and outlines conditions under which nonregistered purchasers may qualify. Compliance with these regulations, including proper completion and timely submission of the exemption certificate, is essential for both purchasers and sellers to navigate the complexities of tax-exempt agricultural purchases in New Jersey effectively.

Sample - St 7 New Jersey Form

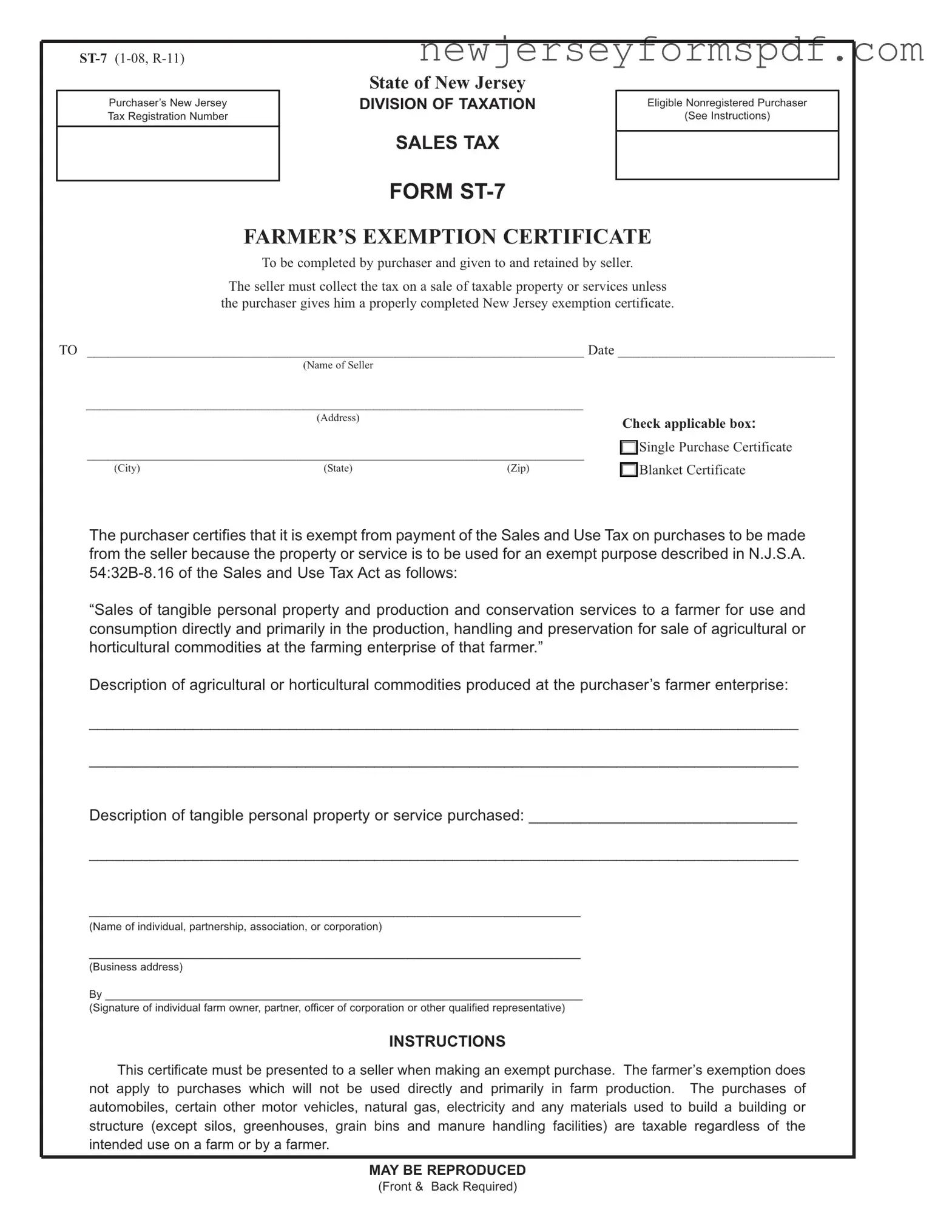

Purchaser’s New Jersey Tax Registration Number

State of New Jersey

DIVISION OF TAXATION

SALES TAX

FORM

Eligible Nonregistered Purchaser

(See Instructions)

FARMER’S EXEMPTION CERTIFICATE

To be completed by purchaser and given to and retained by seller.

The seller must collect the tax on a sale of taxable property or services unless the purchaser gives him a properly completed New Jersey exemption certificate.

TO _______________________________________________________________________ Date _______________________________

(Name of Seller

_______________________________________________________________________

|

(Address) |

|

Check applicable box: |

|

|

|

|

||

_______________________________________________________________________ |

|

Single Purchase Certificate |

||

|

||||

|

|

|||

(City) |

(State) |

(Zip) |

|

Blanket Certificate |

ThepurchasercertifiesthatitisexemptfrompaymentoftheSalesandUseTaxonpurchasestobemade from the seller because the property or service is to be used for an exempt purpose described in N.J.S.A.

“Sales of tangible personal property and production and conservation services to a farmer for use and consumption directly and primarily in the production, handling and preservation for sale of agricultural or horticultural commodities at the farming enterprise of that farmer.”

Description of agricultural or horticultural commodities produced at the purchaser’s farmer enterprise:

__________________________________________________________________________________

__________________________________________________________________________________

Description of tangible personal property or service purchased: _______________________________

__________________________________________________________________________________

_______________________________________________________________________

(Name of individual, partnership, association, or corporation)

_______________________________________________________________________

(Business address)

By _____________________________________________________________________

(Signature of individual farm owner, partner, officer of corporation or other qualified representative)

INSTRUCTIONS

This certificate must be presented to a seller when making an exempt purchase. The farmer’s exemption does not apply to purchases which will not be used directly and primarily in farm production. The purchases of automobiles, certain other motor vehicles, natural gas, electricity and any materials used to build a building or structure (except silos, greenhouses, grain bins and manure handling facilities) are taxable regardless of the intended use on a farm or by a farmer.

MAYBE REPRODUCED

(Front & Back Required)

INSTRUCTIONS FOR USE OFFARMER’S EXEMPTION CERTIFICATE

1.

NOTE: For sales and use tax purposes, a “farming enterprise” does not include an enterprise that is primarily engaged in boarding or training horses or in selling agricultural or horticultural products produced by others.

The farmer’s exemption applies only to sales of tangible personal property or services which will be used directly and primarily in agricultural or horticultural production. It does not apply to sales of: motor vehicles, natural gas, electricity, or property to be used to construct a building or structure (with the exception of silos, greenhouses, grain bins, or manure handling facilities).

NOTE: Whenpurchasingatruckortrucktractorwithagrossvehicleweightratingofmorethan18,000poundswhichisregisteredwith the New Jersey Division of Motor Vehicles as a farm vehicle or a commercial

2.Good Faith- To act in good faith means to act in accordance with standards of honesty. In general, registered sellers who accept exemption certificates in good faith are relieved of liability for the collection and payment of sales tax on the transaction covered by the exemption certificate.

In order for good faith to be established, the following conditions must be met:

(a)Certificate must contain no statement or entry which the seller knows is false or misleading;

(b)Certificate must be an official form or a proper and substantive reproduction, including electronic;

(c)Certificate must be filled out completely;

(d)Certificate must be dated and include the purchaser’s New Jersey tax identification number or, for a purchaser that is not registered in New Jersey, the Federal employer identification number or

(e)Certificate or required data must be provided within 90 days of the sale.

The seller may, therefore, accept this certificate in good faith as a basis for exempting sales to the signatory purchaser and is relieved of liability even if it is determined that the purchaser improperly claimed the exemption.

3.Blanket Certificates - Aseller may permit a purchaser to file a blanket Farmer’s Exemption Certificate to cover future purchases of similar items of tangible personal property. However, each subsequent sales slip or purchase invoice based on such blanket certificate must be clearly marked with the purchaser’s name, address, and identification number.

4.Eligible Nonregistered Purchaser - If the purchaser is not required to be registered with the New Jersey Division ofTaxation and does not have a New Jersey Tax Registration Number, the purchaser is required to place either his Federal Identification Number or, if a sole proprietor, the last three digits of his Social Security Number in the box at the top, right corner of the form marked “Eligible NonregisteredPurchaser.” Note: AnyNewJerseyfarmerwhoisnotasoleproprietor,orwhosellsanygoodsorservicessubjecttosales tax, or who is an employer, must be registered with the New Jersey Division of Taxation and therefore cannot be an “eligible nonregistered purchaser”.

5.

6.Retention of Certificates - Certificates must be retained by the seller for a period of not less than four years from the date of the sale covered by the certificate.

REPRODUCTION OFFARMER’S EXEMPTION CERTIFICATES:

Private reproduction of both sides of these certificates may be made without the prior permission of the Division of Taxation

FOR MORE INFORMATION:

Call the Customer Service Center (609)

Document Specifications

| Fact Number | Fact Detail |

|---|---|

| 1 | The ST-7 form is a Farmer’s Exemption Certificate used in the State of New Jersey. |

| 2 | It is governed by the New Jersey Sales and Use Tax Act, specifically N.J.S.A. 54:32B-8.16. |

| 3 | This form allows eligible farming enterprises to purchase goods and services exempt from sales tax for use directly and primarily in agricultural and horticultural production. |

| 4 | The exemption does not apply to vehicles (except certain heavy-duty trucks), natural gas, electricity, or materials for constructing buildings (other than silos, greenhouses, grain bins, and manure handling facilities). |

| 5 | To qualify, purchasers must complete the form in good faith, ensuring all provided information is accurate and complete. |

| 6 | Blanket certificates may be issued for ongoing purchases that meet the exemption criteria, but must include clear identification for each transaction. |

| 7 | The seller must retain the exemption certificate for at least four years following the sale. |

Detailed Steps for Using St 7 New Jersey

Filling out the ST-7 New Jersey Farmer's Exemption Certificate is a crucial step for eligible farmers who wish to claim exemption from sales and use tax for certain purchases. This process involves providing detailed information to substantiate the exemption claim. It is designed to ensure that only qualified purchases made by farming enterprises that directly and primarily engage in agricultural or horticultural production enjoy the tax relief. The steps below are crafted to guide you through filling out the form correctly to ensure that your claim is processed efficiently and effectively.

- Enter the seller's name, address (including city, state, and zip code), and the date of the transaction at the top of the form.

- Choose between a Single Purchase Certificate and a Blanket Certificate by checking the appropriate box. A Single Purchase Certificate applies to a one-time transaction, while a Blanket Certificate covers all future purchases of similar items from the seller.

- Under the section marked "The purchaser certifies that it is exempt from payment of the Sales and Use Tax on purchases to be made from the seller because," clearly write that the purchase is for "agricultural or horticultural commodities at the farming enterprise of that farmer" as specified in N.J.S.A. 54:32B-8.16.

- Provide a detailed description of the agricultural or horticultural commodities produced at your farming enterprise.

- Describe the tangible personal property or service purchased that qualifies for the exemption.

- Include the name of the individual, partnership, association, or corporation making the purchase.

- Write the business address of the purchaser.

- Sign the certificate. The signature must be that of the individual farm owner, partner, officer of the corporation, or other qualified representative.

- If you don’t have a New Jersey Tax Registration Number because you're not required to be registered with the New Jersey Division of Taxation, place either your Federal Identification Number or, if you’re a sole proprietor, the last three digits of your Social Security Number in the box at the top right corner of the form marked “Eligible Nonregistered Purchaser.”

- Ensure the form is completed in its entirety, with no false or misleading information, and that it is dated with the purchaser’s identification number clearly stated.

After completing and signing the ST-7 form, it must be presented to the seller at the time of purchase. Sellers are required to retain this certificate for at least four years from the date of the sale. It’s essential to understand that the seller must collect tax on any sale of taxable property or services unless you provide them with a properly completed exemption certificate. Additionally, remember that this exemption does not apply to all purchases, such as motor vehicles, natural gas, electricity, and materials used to build structures (with some exceptions). Careful adherence to the instructions and correctly filling out the form will facilitate a smoother process in claiming your tax exemption.

Learn More on St 7 New Jersey

What is the ST-7 Form in New Jersey?

The ST-7 Form, also known as the Farmer's Exemption Certificate, is a document that allows farmers in New Jersey to make tax-exempt purchases of tangible personal property or services that are directly and primarily used in the production, handling, and preservation for sale of agricultural or horticultural commodities. This form should be completed by the purchaser and presented to the seller at the time of purchase.

Who is eligible to use the ST-7 Form?

Eligibility to use the ST-7 Form is restricted to businesses that are considered “farming enterprises” under N.J.S.A. 54:32B-8.16 of the Sales and Use Tax Act. This includes enterprises using land to raise agricultural or horticultural commodities for sale, such as dairy products, poultry, feed crops, fruit, vegetables, livestock, fur animals, timber, ornamental plants, bees, and apiary products. However, enterprises primarily engaged in boarding or training horses, or in selling agricultural or horticultural products produced by others, are not eligible.

What are the conditions for a purchase to be exempt under this certificate?

- The purchase must be for tangible personal property or services used directly and primarily in agricultural or horticultural production.

- Items such as motor vehicles, natural gas, electricity, or property used to construct buildings (except for certain structures like silos and greenhouses) are not exempt.

- The purchaser must provide the certificate in good faith, meaning all information must be accurate and complete.

Can the ST-7 Form be used for a one-time purchase?

Yes, the ST-7 Form can be used as a Single Purchase Certificate for a one-time tax-exempt purchase, or it can serve as a Blanket Certificate for multiple future purchases of similar items from the same seller, provided each purchase meets the exemption criteria.

What information must be included on the ST-7 Form?

The form must be filled out completely and include:

- The name and address of the seller

- The date of the certificate

- A description of the agricultural or horticultural commodities produced

- A description of the tangible personal property or services purchased

- The name, business address, and signature of the farm owner or representative

- The purchaser’s New Jersey tax identification number, or, for nonregistered purchasers, the Federal employer identification number or the last three digits of their Social Security Number

What are the responsibilities of the seller when accepting the ST-7 Form?

Sellers must ensure the certificate is fully completed and presented in good faith. They should keep the certificate for at least four years from the date of the sale. Accepting an ST-7 Form in good faith relieves the seller from the liability of collecting and remitting sales tax on the exempt purchases made by the purchaser.

Where can I find more information or assistance regarding the ST-7 Form?

For more details or assistance, you can contact the New Jersey Division of Taxation directly by calling their Customer Service Center at (609) 292-6400, sending an email to nj.taxation@treas.state.nj.us, or writing to the New Jersey Division of Taxation, Information and Publications Branch, PO Box 281, Trenton, NJ 08695-0281.

Common mistakes

Filling out the ST-7 New Jersey form correctly is essential for ensuring that purchases made by farming enterprises are properly exempt from sales and use tax. However, individuals often make mistakes during this process. Here are six common errors:

Not including the New Jersey Tax Registration Number or, for non-registered purchasers, the appropriate identification number (Federal Identification Number or Social Security Number) at the top of the form. This oversight can invalidate the exemption being claimed.

Selecting the incorrect certificate type between Single Purchase Certificate and Blanket Certificate. It's crucial to understand the difference: a Single Purchase Certificate applies to one transaction, while a Blanket Certificate covers multiple future purchases of similar items.

Failing to provide a detailed description of the agricultural or horticultural commodities produced at the purchaser's farm enterprise, as well as a clear description of the tangible personal property or service purchased. Vague descriptions can lead to the rejection of the exemption claim.

Omitting the signature of the individual farm owner, partner, officer of the corporation, or other qualified representative at the end of the form. A signature is necessary to certify the exemption claim.

Misunderstanding the scope of the farmer’s exemption by attempting to apply it to prohibited items such as motor vehicles, natural gas, electricity, and materials used to construct a building or structure (excluding certain specified farm-related structures).

Providing incomplete or incorrect information regarding the purchaser's eligibility as a Nonregistered Purchaser. Specifically, some purchasers might fail to include their last three digits of their Social Security Number (for sole proprietors) or their Federal Identification Number.

Avoiding these mistakes ensures that the exemption certificate is properly completed and accepted, facilitating the tax-exempt purchase of eligible items.

Documents used along the form

When leveraging the ST-7 New Jersey Farmer’s Exemption Certificate, it's often accompanied by other forms and documents to ensure comprehensive compliance and to maximize the benefits of pertinent tax laws and regulations. These companion documents contribute to a more streamlined process for both the purchaser and seller, emphasizing the importance of understanding and utilizing them effectively.

- ST-4 Exempt Use Certificate: This certificate is akin to the ST-7 but is specifically designated for purchases that are exempt from the sales and use tax for reasons other than agricultural production. For instance, when purchasing automobiles or trucks with a certain gross vehicle weight, this form is utilized instead of the ST-7, adhering to N.J.S.A. 54:32B-8.43.

- REG-1E Application for ST-5 Exempt Organization Certificate: Organizations that qualify for tax-exempt purchases due to their nature (such as nonprofits, schools, or religious institutions) must initially complete the REG-1E to obtain an ST-5 Exempt Organization Certificate, which subsequently allows tax-free purchases.

- NJ-REG Business Registration Application: This application is crucial for any business, including farming enterprises, intending to operate within New Jersey. It's a prerequisite for obtaining a New Jersey Tax Registration Number, necessary for completing the ST-7 form. Additionally, it serves to register the enterprise with the Division of Revenue and Enterprise Services for other business-related taxes and filings.

- SS-4 Application for Employer Identification Number (EIN): The SS-4 form is used by entities to apply for an EIN from the IRS. This number is essential not only for tax filing purposes but also for completing the ST-7 form in cases where the purchaser is an eligible nonregistered purchaser without a New Jersey Tax Registration Number but can provide their Federal EIN instead.

Together, these forms create a foundational framework for agricultural enterprises and other eligible organizations to navigate New Jersey's tax exemption processes effectively. Ensuring accurate and timely submission of these documents, in conjunction with the ST-7 Farmer’s Exemption Certificate, is imperative for the fulfillment of tax obligations and the availing of benefits under the state's tax code.

Similar forms

The ST-4 Exempt Use Certificate is comparable to the ST-7 New Jersey form, focusing on exempt purchases but tailored for different scenarios. Where the ST-7 targets agricultural pursuits, the ST-4 is broader, catering to goods or services used within a company for a non-taxable purpose. Both forms require purchasers to certify the eligibility of their tax-exempt status, but the ST-4 is often employed for manufacturing or industrial operations, legitimizing tax-free transactions for equipment or supplies integral to production or operations.

Another similar form is the Resale Certificate, also known as Form ST-3 in New Jersey. This document is utilized by businesses purchasing goods intended for resale rather than personal use. Like the ST-7, it aids in avoiding the immediate payment of sales tax at the point of purchase. The key commonality lies in their function to prevent tax payment on taxable sales, provided these sales are exempt under specific conditions outlined by state law.

The Streamlined Sales and Use Tax Agreement Certificate of Exemption is a multi-purpose form that, akin to the ST-7 form, is designed to streamline the exemption process for eligible purchasers on a multi-state level. This form is particularly useful for businesses operating in multiple states, allowing them to comply with the varying tax exemption requirements within the Streamlined Sales and Use Tax Agreement member states. Both certificates serve to certify that a purchase is intended for an exempt purpose, thereby negating the sales tax typically collected by the seller.

The Uniform Sales & Use Tax Exemption/Resale Certificate - Multijurisdiction form serves a similar purpose to the ST-7, intended for use by businesses making purchases that will either be resold or used in a manner that qualifies for a tax exemption. Like the ST-7, this form facilitates tax-exempt purchases across various jurisdictions, thereby simplifying the process for companies that operate in multiple states or that purchase goods for resale or production that qualify for tax exemptions.

The Capital Improvement Certificate, often specific to certain states, parallels the ST-7 by offering a tax exemption on services and materials used in direct capital improvement of property. While the ST-7 focuses on agricultural goods and services, the Capital Improvement Certificate applies broadly to construction or renovation projects, exempting purchases from sales tax when materials are directly transformed into an integral, permanent part of a structure.

The Direct Payment Permit is slightly different in purpose but similar in its tax exemption implications. Holders of such permits, including those who might also use an ST-7, are authorized to make tangible personal property or taxable services purchases without paying sales tax to the supplier. The permit holder is responsible for self-assessing and remitting the tax directly to the state, offering a cash flow benefit and ensuring the precise application of exemptions.

The Farmer's Affidavit, while not a formal tax exemption certificate, serves a comparable role to the ST-7 by affirming a buyer's intent to use purchased goods in farming. This document, usually less formal, is often used to substantiate the qualifications for agricultural tax exemptions in direct purchases or even at auction, underscoring the use-based exemption similar to the ST-7’s purpose.

An Exemption Certificate for Government Purchases, such as those used by federal, state, or municipal agencies, shares the ST-7’s feature of bypassing the sales tax on eligible transactions. Government entities use their specific forms to assert tax-free purchase status for goods and services deployed within their governmental functions, paralleling the tax-exempt intent behind the ST-7's agricultural focus.

The Non-Profit Organization Exemption Certificate mirrors the ST-7’s tax exemption premise but is specialized for 501(c)(3) or similar organizations. By certifying their status, non-profits can purchase goods and services without incurring the sales tax, supporting their operational and charitable activities in a manner akin to the agricultural exemptions provided by the ST-7 form.

Lastly, the Use Tax Certificate aligns with the ST-7 in its exemption application, although it specifically addresses use tax liabilities rather than sales tax at the point of purchase. For out-of-state purchases where sales tax wasn’t collected by the seller, the Use Tax Certificate can apply for tax exemptions on goods brought into a state for use, storage, or consumption, paralleling the ST-7’s aim to exempt certain purchases from tax under specific conditions.

Dos and Don'ts

When filling out the ST-7 New Jersey Farmer’s Exemption Certificate, there are specific actions you should take to ensure the process is completed accurately and efficiently. Below are guidelines on what to do and what not to do:

Do:- Verify eligibility: Ensure that the business qualifies as a “farming enterprise” under N.J.S.A. 54:32B-8.16, involved directly in agricultural or horticultural production.

- Use correct identification numbers: Include the purchaser’s New Jersey tax registration number or, if not registered in New Jersey, the appropriate Federal employer identification number or out-of-state registration number. Sole proprietors should use the last three digits of their Social Security Number if not registered.

- Complete all sections: Fill out the certificate completely, including the date and a detailed description of the agricultural or horticultural commodities produced and the tangible personal property or service purchased.

- Choose the correct certificate type: Clearly indicate whether it’s a single purchase certificate or a blanket certificate, based on the purchase's nature and frequency.

- Act in good faith: Provide accurate and honest information. The seller's acceptance of the exemption certificate relies on the veracity of the provided information.

- Keep records: Retain a copy of the certificate for a minimum of four years from the date of the transaction for record-keeping and verification purposes.

- Use the certificate for ineligible items: Do not use this certificate for purchases like motor vehicles, natural gas, electricity, or materials for constructing buildings (with the exception of silos, greenhouses, grain bins, or manure handling facilities) as these are not covered under the farmer’s exemption.

- Leave sections blank: Avoid submitting the form with incomplete information. Incomplete forms may not be accepted and could result in the transaction being considered taxable.

- Offer false information: Do not knowingly provide false or misleading information. This could invalidate the exemption certificate and potentially lead to penalties.

- Overlook the expiry for blanket certificates: When using a blanket certificate for ongoing purchases, do not forget to ensure that each purchase invoice is clearly marked with the necessary purchaser details as specified.

- Ignore certificate updates: Do not fail to update the certificate if there are significant changes to your farming enterprise or if you no longer qualify for the exemption.

- Delay submission: Avoid delays in providing the certificate or required data to the seller. Certificates must be provided within 90 days of the sale to be valid.

Misconceptions

When dealing with the New Jersey Farmer’s Exemption Certificate (ST-7), there are several common misconceptions that can lead to confusion for both buyers and sellers. Understanding these misconceptions is crucial for carrying out taxable transactions accurately. Below is a list of eight misconceptions and their clarifications:

- All purchases by a farmer are exempt from sales tax. This is not accurate. The exemption applies specifically to purchases of tangible personal property and certain services that are used directly and primarily in the production, handling, and preservation for sale of agricultural or horticultural commodities.

- The exemption certificate can be used for any type of farming enterprise. The reality is that the exemption applies only to enterprises considered as “farming enterprises” under N.J.S.A. 54:32B-8.16, which excludes operations primarily engaged in boarding or training horses or selling agricultural products produced by others.

- Personal vehicles used on a farm can be purchased tax-free with this certificate. However, the certificate does not exempt purchases of motor vehicles, natural gas, electricity, or materials used for constructing buildings or structures (with limited exceptions like silos or greenhouses).

- Any type of truck purchased for farming use can be exempted using ST-7. This is incorrect. Trucks or truck tractors with a gross vehicle weight rating over certain limits must be purchased using an Exempt Use Certificate (ST-4), not the Farmer’s Exemption Certificate.

- There is no need to provide a New Jersey Tax Registration Number when using the exemption certificate. In truth, the certificate requires the purchaser’s New Jersey tax identification number, Federal employer identification number, or out-of-state registration number for non-registered purchasers in New Jersey.

- Blanket certificates cover all future purchases automatically. While blanket certificates are convenient, each subsequent sale or purchase invoice needs to be clearly marked with the purchaser's name, address, and identification number to be valid.

- Eligibility for using ST-7 is automatic for all farmers. Farmers who sell goods or services subject to sales tax, are employers, or are not sole proprietors need to be registered with the New Jersey Division of Taxation and cannot use the certificate as an "eligible nonregistered purchaser."

- Sellers have no responsibility once the exemption certificate is accepted. Sellers must act in good faith, ensure the certificate is fully completed, and retain the certificate for not less than four years from the date of the sale covered. Improper or incomplete certificates could deem sales taxable, with the burden of proof on the seller.

Understanding these specifics about the New Jersey Farmer’s Exemption Certificate ensures that both purchasers eligible for the exemption and sellers are fully compliant with the state's taxation laws, thereby avoiding potential penalties or misunderstandings related to sales tax exemptions.

Key takeaways

Understanding the ST-7 New Jersey Farmer’s Exemption Certificate is crucial for farming enterprises looking to purchase goods and services tax-free for direct use in agricultural production. Here are key takeaways to guide purchasers and sellers in properly using this form:

- The ST-7 form is specifically designed for businesses identified as “farming enterprises” by the New Jersey Sales and Use Tax Act, covering a wide range of agricultural and horticultural production activities.

- This exemption certificate can be used to purchase tangible personal property and services tax-free, provided these are directly and primarily used in agricultural or horticultural production.

- It is important to note that certain items, including motor vehicles, natural gas, electricity, and materials for constructing buildings (excluding specific structures like silos and greenhouses), are not covered under this exemption.

- For a purchase to qualify, the ST-7 form must be fully completed and presented at the time of purchase, detailing the specifics of the exempt use.

- Good faith acceptance of an exemption certificate by sellers protects them from being liable for the collection and payment of sales tax on transactions deemed exempt, provided specific conditions are met regarding the contents and completion of the certificate.

- Purchasers not required to register with the New Jersey Division of Taxation, and thus without a New Jersey Tax Registration Number, can still use this form by indicating their Federal Identification Number or, for sole proprietors, the last three digits of their Social Security Number.

- Blanket certificates are an option for purchasers anticipating multiple purchases; however, they necessitate clear identification on subsequent sales slips or invoices to maintain the exemption status.

- The responsibility of keeping exemption certificates for a minimum of four years from the date of the relevant sale rests with the seller, ensuring compliance with state tax regulations.

Proper understanding and application of the ST-7 form ensure that eligible farming enterprises benefit from tax exemptions on applicable purchases, thereby supporting agricultural and horticultural productivity in New Jersey.

Popular PDF Documents

What Is a Sales Agreement - The contract specifies the conditions under which the financing is to be secured and the consequences of failure to obtain financing within the stipulated time.

Realtors Nj - Information on any additions, remodels, or major repairs done to the property, ensuring buyers are aware of changes and permits.